Table of Contents

- 1. Introduction

- 2. What is the problem?

- 3. How did grid connections become so difficult?

- 4. Don’t forget the demand side: the impact of losing focus on demand connections

- 5. Solving the problem

- 6. Authors

Introduction

An abandoned former coal plant near the largest city in Wales should be a data centre developer’s dream site. Aberthaw boasts 300 acres of developable land, seaside water for cooling, and nearby wind and solar projects. Most important of all, the site already has the physical infrastructure to enable a 1.5 gigawatt grid connection. The reality of Britain’s grid, however, means that developers may wait for five years to receive power from a site already on the network. This wait can extend up to a decade for sites with no existing infrastructure.

Timely grid connection agreements have become a valuable asset, because of how difficult they are to get and how long they take to secure. All of the grid connection slots for generation projects are locked up until 2035. Meanwhile, energy users like data centres, new housing developments, and industry face years of uncertainty and delay. This shouldn’t be the binding constraint for delivering projects that are essential for growing Britain’s economy.

Our paper seeks to explain what is driving the logjam, and makes the case for measures to improve the speed and certainty of demand-side grid connections.

What is the problem?

Britain’s grid is the physical transportation network that allows electricity to be delivered around the country. Aggregating electricity demand and supply in theory makes the system more reliable and cost-effective. Broadly speaking, grid infrastructure is divided into transmission, which transmits electricity across long distances at high voltage, and distribution, which connects electricity directly to users at low voltage. High voltage transmission reduces the amount of electricity lost between generation and consumption, while low voltage distribution allows electricity to be used safely.

Grid connections can happen on either the transmission or distribution system, depending on the amount of power the generator will produce, or how much the customer needs. In either case, the point of connection will ultimately be a substation. Substations are pieces of infrastructure that allow voltages to be transformed and also contain the equipment to safely accommodate new connections. They range from 400 kilovolt (kV) transmission substations down to much smaller substations at distribution level. In an ideal world, connecting to a substation would be seamless. A company would ask for a grid connection to supply or purchase electricity, and their request would be honoured.

But substations can only accommodate so many connections before they need to be expanded and upgraded. There needs to be physical space for the new connection point, and enough electrical capacity to handle the new power flow, both at the substation itself and through the wider network. This has become a major bottleneck in much of Great Britain.

An increase in demand and supply connection requests has used up space on much of the network. Major transmission projects can take twelve to fourteen years to be delivered. Massive connection queues have built up, which has driven a speculative frenzy for perceived scarce assets.

Long grid connection queues and delays in delivery have real costs. Long queues prevent the grid from responding to new technologies and economic opportunities, from AI to clean energy. Demand-side projects cannot be built in the timeframes suitable for securing contracts, which deters investment or sends it abroad.

Delays beyond the promised connection date incur tangible project expenses such as lease payments and debt facility fees. Investors also price in a higher cost of capital to account for the risk of connections not happening on time, which flows directly into electricity prices.

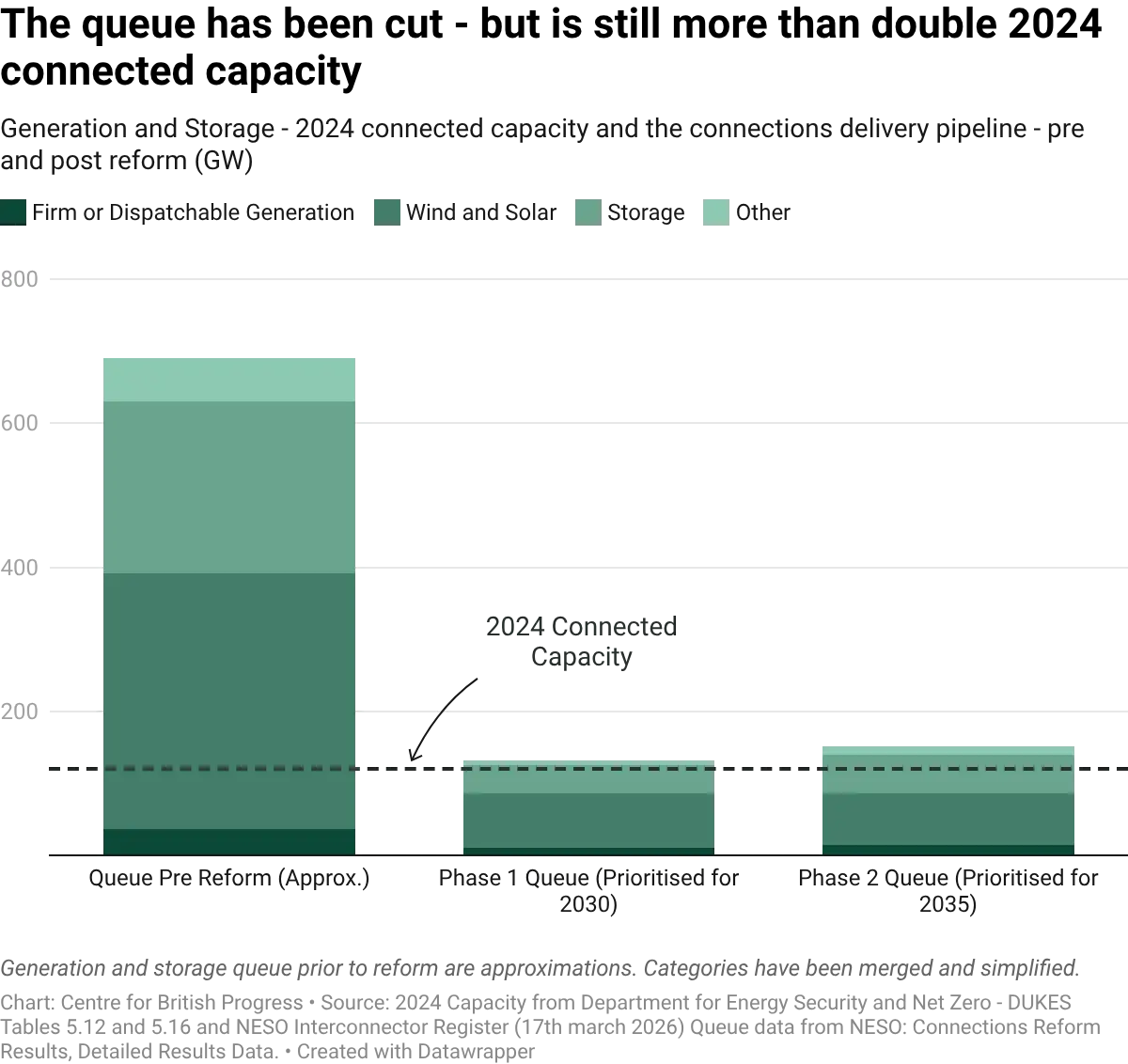

In 2025, the National Energy System Operator (NESO) took radical top-down action, via a set of reforms known as TMO4+. The reforms focussed primarily on the generation and storage side of the queue, trimming project pipelines to align with the Government's Clean Power ambitions.

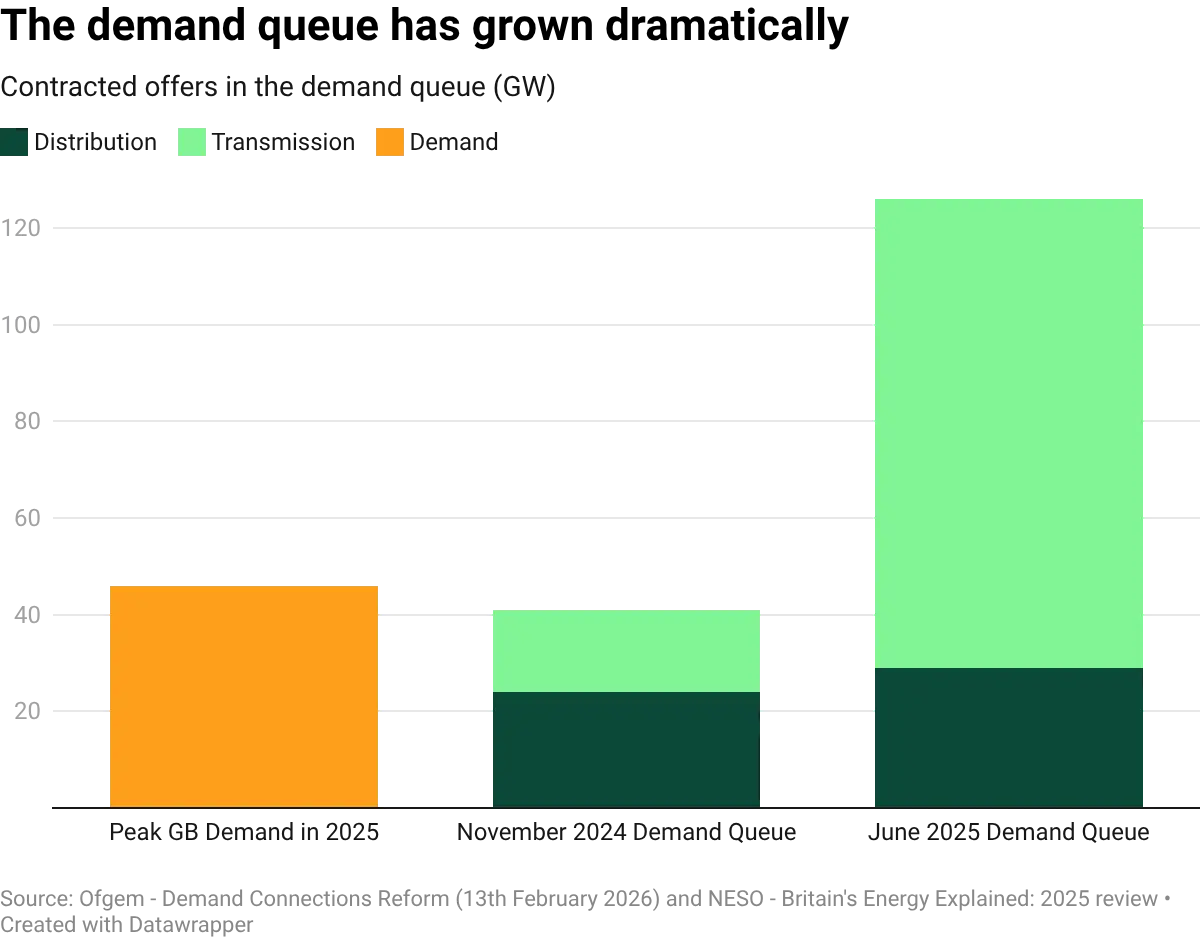

Whilst the TMO4+ reforms were underway, the demand queue more than doubled in the seven months from November 2024, attracting the attention of the National Energy System Operator (NESO) and the energy regulator (Ofgem). Ofgem have consulted on a number of options, including deposits and fees, to reduce the queue of data centre projects to more realistic levels.

Re-ordering the queue can help important projects to be prioritised, but it doesn’t move projects faster through the queue. Our paper focuses on how we can increase the speed of building new connections in Great Britain.

We propose that the Government should:

- Enable direct connections at 400kV for sole-use demand projects

- Extend user self-build distance limits

- Let independent providers build connection spurs downstream of the transmission system

- Improve visibility of the full connection queue

How did grid connections become so difficult?

We identify three major drivers of why the GB queue is particularly lengthy: renewables, speculation, and poor delivery incentives.

1. The rise of renewables increased the number of grid connections but decreased utilisation

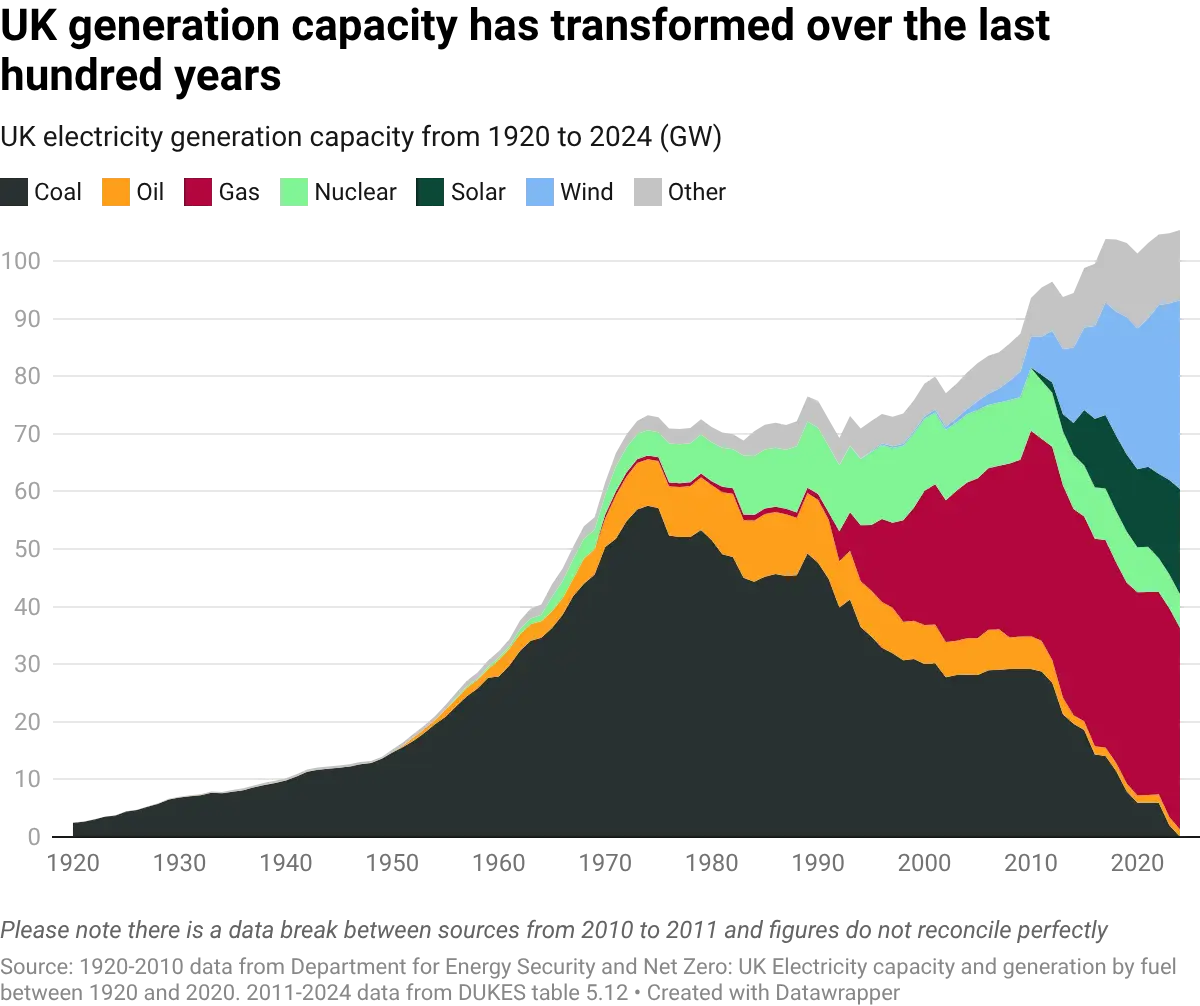

The UK grid was built around a network of large power stations, originally coal and later nuclear power in the ‘70s and ‘80s. Natural gas followed in the ‘90s and early ‘00s, driven by falling gas generation costs, due to advances in gas turbine technology and increased North Sea production. All three generation technologies operated at high capacity factors and tended to connect into the high-voltage transmission network.

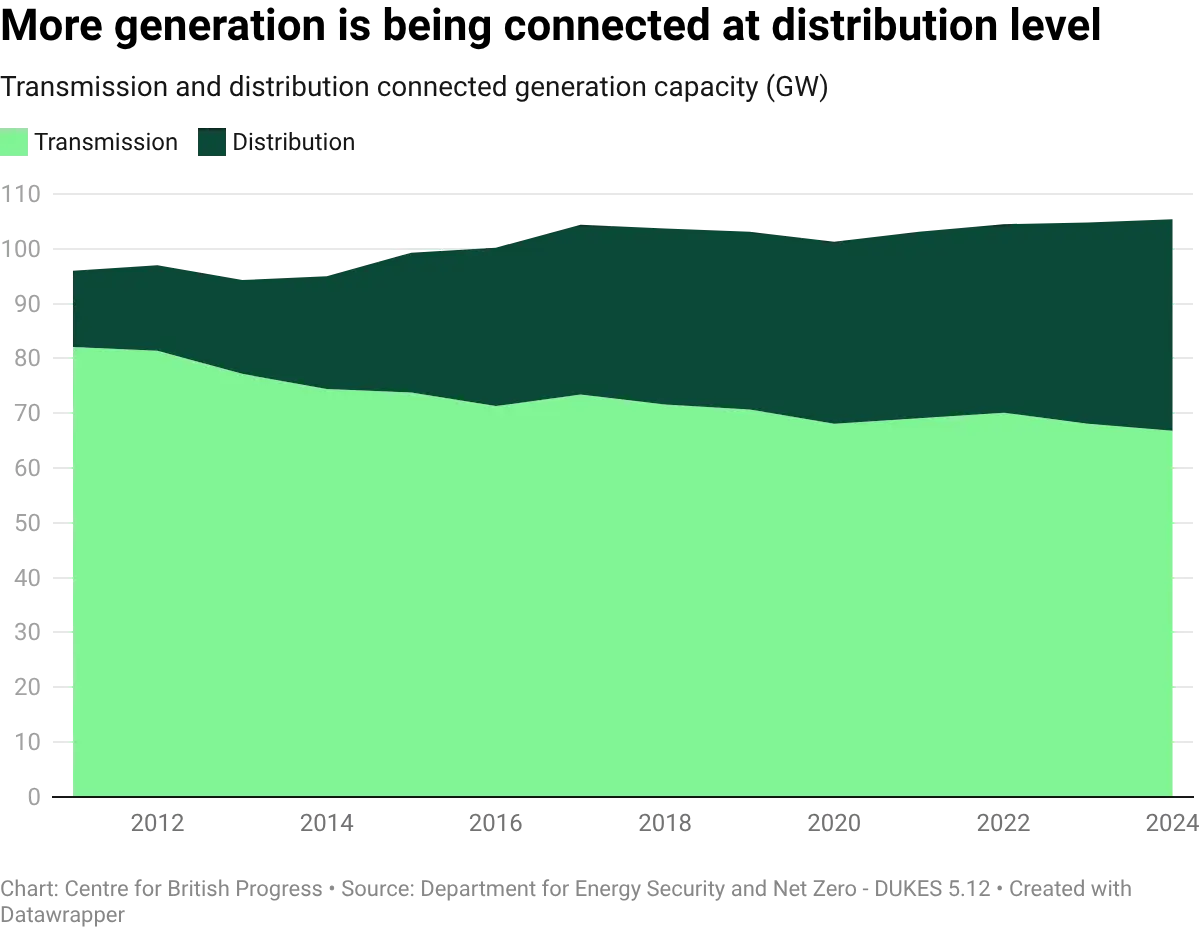

Renewables require much more grid infrastructure than the prior network of large power stations.

Since 2011, the UK has built at least 44 gigawatts of renewable capacity. Renewable sites are smaller than historic baseload sites on average, so more sites and more grid connections are required for each MW of connected generation. They require even more connections per unit of electricity delivered because of lower utilisation (capacity factor) and intermittency (variation in output due to changes in the weather).

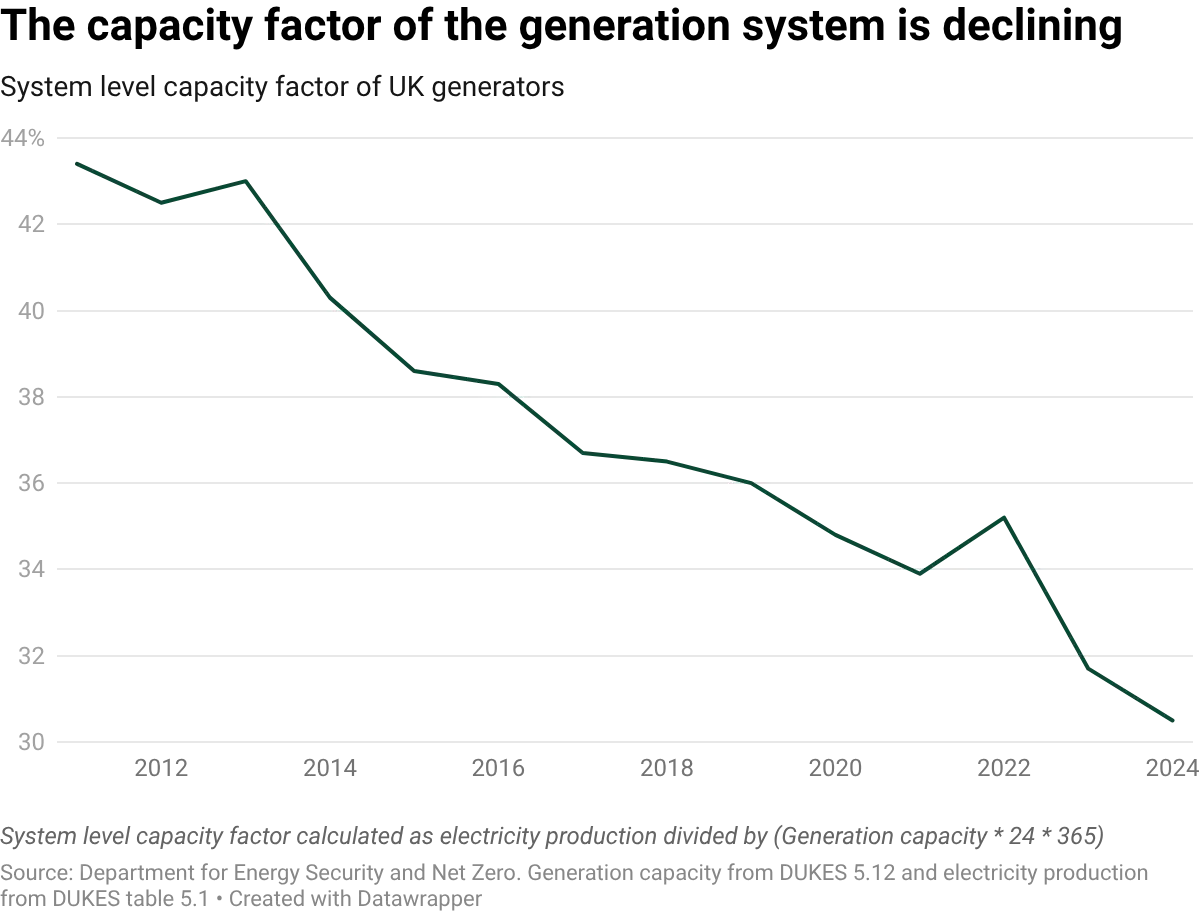

In the year 2000, the UK’s combined cycle gas turbine fleet ran at a 75% load factor. Nuclear and coal ran at 70.5% and 50.8% respectively. In 2024, offshore wind ran at 38.7%, onshore wind at 25.7% and solar photovoltaic at 9.8%. Because wind and solar are intermittent, the UK has to maintain grid connections to gas power stations to ensure that power can be delivered when required. The result is an electricity system with declining utilisation.

Renewable generation sites are often chosen based on proximity to natural resources, rather than where existing grid infrastructure or demand is located. For instance, we have a proliferation of onshore wind in Scotland, where electricity demand is low relative to production and the grid is constrained to deliver energy to population centres further south.

Locating generation close to natural resources has precedent. Coal plants were often sited near coal mines and nuclear power stations near the coast for seawater cooling. But much of our current generation is not only sited far from demand, but is composed of smaller sites that connect at distribution level. This in turn creates large transportation losses if the power has to be stepped up in voltage for transmission further south, and then stepped back down again for end users.

Managing frequency and voltage has also become more difficult with the loss of synchronous generation, requiring new infrastructure to keep the system secure. There are 19 such ‘reactive compensation’ projects in the grid queue for delivery by 2030.

Great Britain is also suffering from an unpleasant hangover from prior grid connection policy.

In May 2009, Ofgem introduced an interim ‘Connect and Manage’ regime. This allowed generators, particularly renewables, to connect to the network before wider transmission reinforcement works had taken place. An ‘interim’ decision in 2009 helped bring forward connections at the time, but ultimately became permanent. The subsequent shortfall in transmission reinforcement has driven up constraint costs, as key network bottlenecks haven’t been upgraded to deal with increased power flows from North to South.

Part of the problem is the slow pace of grid upgrades relative to new generation projects. The 2023 Winser review noted that strategic transmission projects were expected to take 12 to 14 years, whereas wind farms could be built in less than half that time.

The 2024 General Election and the Government’s Clean Power 2030 ambition brought forward the timeline for decarbonising the GB electricity system from 2035 to 2030, dramatically increasing delivery pressures. The National Energy System Operator laid out the requirements in stark terms:

“Network expansion must proceed at more than four times the rate of the last decade, delivering twice as much in half the time”

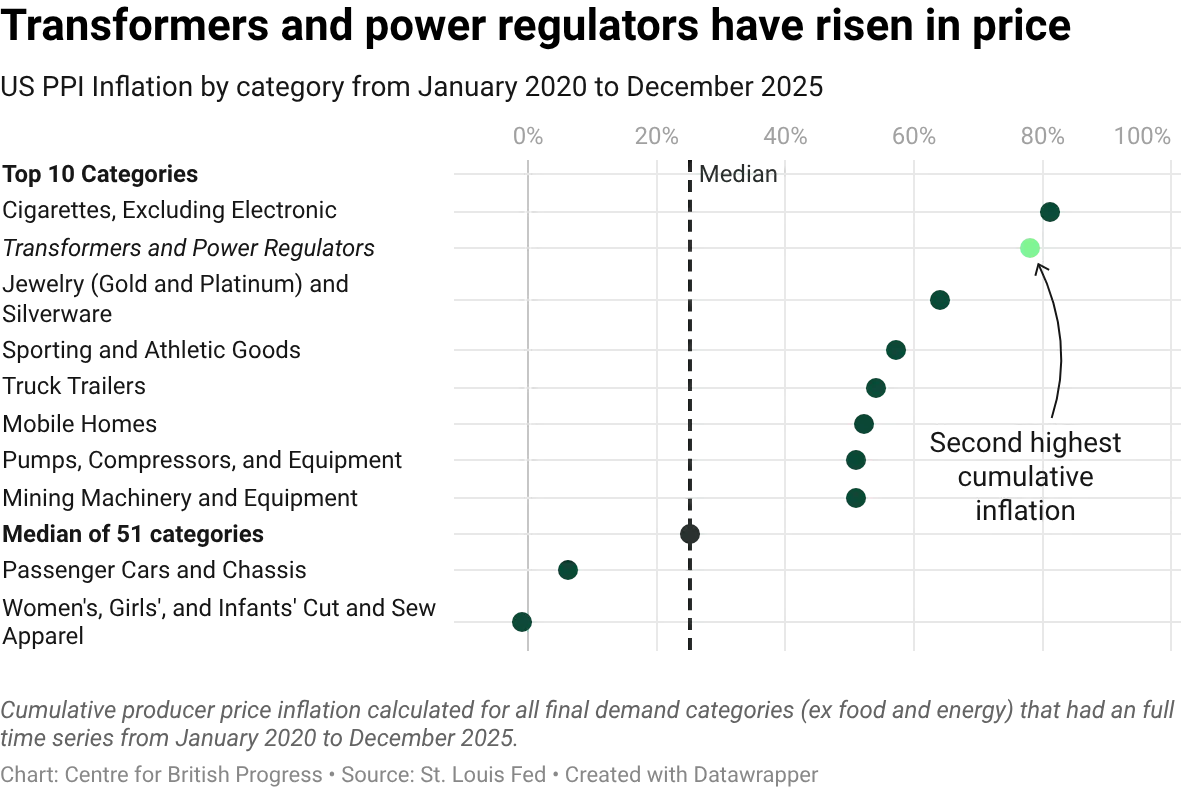

Whilst Great Britain has specific issues, many of the trends are happening in a global context. Countries compete to procure specialist equipment like transformers, which increases prices and lead times for installing new connections.

All of these demand pressures have to be met by a supply side which faces real engineering constraints. New connections and grid upgrades need to be completed without disrupting power flows to users - akin to carrying out repair work on a train line that commuters continue to use to get to work each day.

To allow network upgrades, new connections or maintenance to take place safely, electrical circuits will need to undergo a planned outage. These planned outages or ‘system access’ events require close coordination between NESO, network owners and construction teams to avoid disrupting power flows to end users. Particularly complex projects require outage planning up to six years ahead, and delays have the potential to impact other projects, creating a ripple effect if outage windows are missed. Britain’s planned network upgrades will require nimble project management to allow so many upgrades to happen at once without compromising security of supply.

2. Speculative demand creates a cycle of ever-rising queues, which causes delays and potentially worse network planning

Historically, there have been relatively low entry barriers to securing a grid connection offer. Typically, the process involved thermal studies, voltage studies and some design charges for the grid connection agreement. Low entry barriers are helpful for economic growth as they allow projects to secure a critical grid connection requirement before they start building.

However, if a grid queue grows longer, a connection offer can become a low cost option, triggering a wave of speculative applications and an even longer queue. For example, one prospective developer submitted 240 identical applications, presumably in order to find the earliest connection offer date. Such behaviour is reminiscent of the supermarket queues for toilet paper during the pandemic - perhaps rational on an individual level, but unhelpful for the collective system.

Lengthy connection times also encourage developers to join the queue early ‘just in case’, as connection agreements have become a vital prerequisite for developing a generation project. When the first CfD allocation round opened in 2014, a connection offer was required to participate. Projects without an offer are also much more difficult to finance.

The critical nature of a connection offer can then imbue those agreements with scarcity value, potentially encouraging developers to submit applications in the hope of securing a valuable asset.

Lengthy queues of speculative projects have real costs. Moving through the connection queue requires coordinating back and forth with developers. Building in a reasonable wait time for responses slows down queue progress for projects with more advanced plans.

Network owners are also impacted by speculative demand, as they use the pipeline of connection offers as a signal for where to build new infrastructure. If this queue is unrealistic in scope, networks risk building out stranded assets.

3. Incentives are designed for efficiency, not delivery

The regulatory structures that govern private network owners weren't created with grid expansion in mind. Transmission and distribution networks were privatised in 1990, and the government introduced regulation and price controls to protect consumers from monopolistic behaviour.

Regulated networks are managed under a series of price control periods, typically five years in duration. Ahead of a control period, network companies will submit business plans that detail their investment requirements to meet regulatory objectives. After scrutinising their spending plans, Ofgem publishes ‘final determinations’ that set out the spending allowances and incentives for the control period. Capital expenditure during the control period is added to the network’s asset base, upon which they make an inflation-adjusted rate of return set by the regulator. Alongside the regulated return, operating expenditure and depreciation is recovered through customer revenue each year.

Multi-year price control periods aren’t a nimble way of reacting to a changing electrification environment. Large projects require regulatory sign-off before investment can proceed. This protects bill payers from unnecessary network expansion, but slows down investment. Furthermore, UK electricity consumption is broadly flat versus 35 years ago and networks have understandably been focussed on improving efficiency, rather than building new infrastructure.

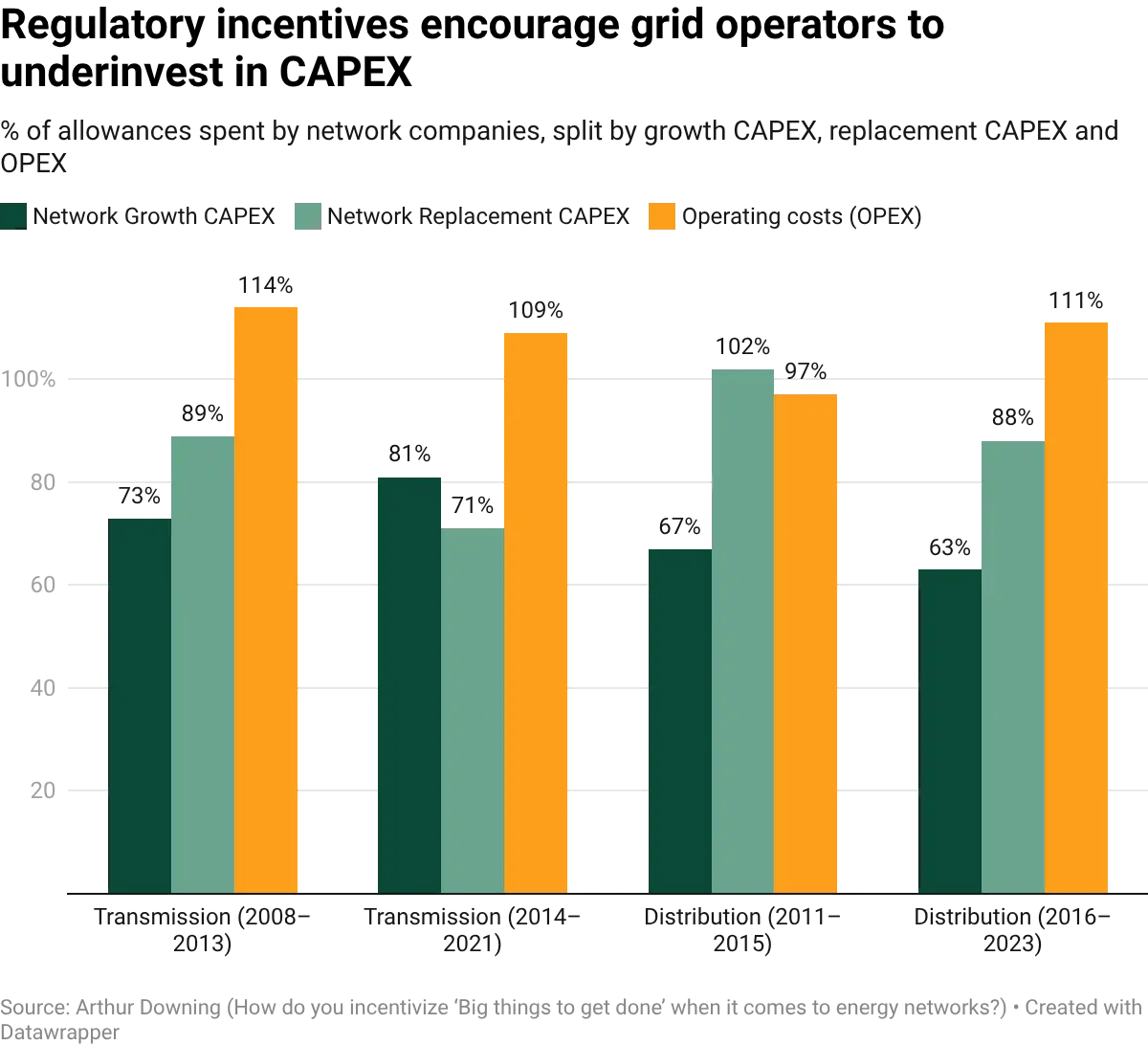

A notable feature of the incentive structure embedded into control periods is the approach to overspend and underspend. Mechanisms such as the ‘totex incentive mechanism’ (TIM) allow networks to keep some of the savings if their spend is below regulatory allowances. A profit maximising actor under this system can enhance returns by proposing that the regulatory allowances are set as high as possible, and then underspending relative to this high bar.

Networks have consistently underspent their regulatory allowances, enhancing their returns via incentive mechanisms but delaying much needed investment. The current system creates and rewards this pattern of behaviour.

More recent data suggests that this pattern of underspend is continuing. Ofgem have expressed concerns over lower than expected maintenance activity in the transmission networks.

“We remain concerned over the lower-than-anticipated levels of asset intervention across all networks, and the potential this has for heightened asset deterioration and the risk of reduced system resilience”

We must find a better way - allowing infrastructure to be built and projects connected, without leaving the public on the hook for stranded assets.

Don’t forget the demand side: the impact of losing focus on demand connections

Decarbonising the electricity system is a core mission for the Government, but we should not sacrifice demand-side connections to meet the Clean Power 2030 target.

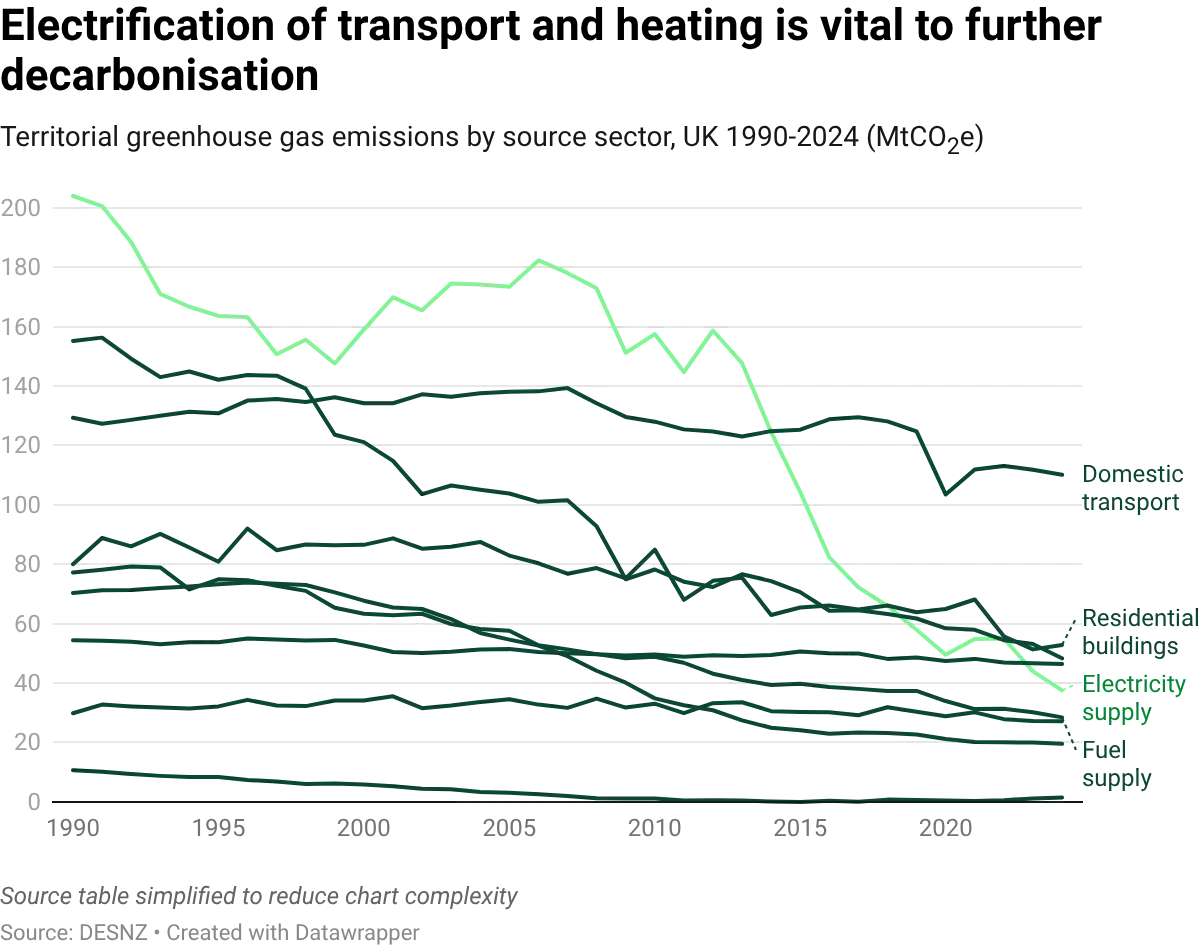

The electricity system was responsible for just 10% of UK territorial emissions in 2024. Longer term decarbonisation will require electrifying sectors such as heating and transport, which, on a combined basis, make up nearly half of our territorial emissions.

Electrification is also vital for Britain’s long term energy security, allowing us to substitute imported fossil fuels with electricity produced domestically - from renewables and nuclear power. In the long run, retail electricity prices will be much more stable than fossil fuels, insulating our economy from price spikes caused by events such as the recent conflict in Iran.

More demand can allow fixed costs in the electricity system to be shared over more megawatt-hours of consumption, reducing unit prices. The UK has been suffering from the opposite dynamic, with final electricity consumption falling by 22% since 2005 and by c. 10% in the last decade.

We estimate that this 10% volume loss has increased electricity prices by around 3% per kWh for end users in 2024, versus a counterfactual of stable volumes. This is because the largely fixed costs of network infrastructure and legacy policy costs (ROCs and FITs) have been spread over a shrinking consumption base.

Adding more demand side users can help reverse this dynamic, especially if consumption grows without increasing peak demand, improving the network’s utilisation. Flexible connection agreements or enabling demand customers to co-locate with generation or storage makes this possible.

The importance of the demand side will only increase as more of the electricity system costs become fixed and the relevance of fuel-based variable costs diminishes.

Solving the problem

Demand customers want grid connections that are:

- Fast: A close match between the connection date desired by the customer (e.g. to align with typical contracting and build timelines) and those offered by the network owner.

- Predictable: Confidence that the offered dates will be honoured so customers can arrange financing and schedule construction.

- Inexpensive: The ability to connect to the system at a reasonable cost.

- Flexible in location: The ability to locate near areas of existing human capital or transportation infrastructure. This may be more important to customers than siting in a location that suits the network operator.

- Prioritised: A methodology to bring forward connection dates if a business has a strong speed or locational preference versus one which is location or wait-time agnostic.

The UK has already invested significant resources into improving the connection process. Before listing our own ideas, we highlight some of the measures which have already been put into place:

- Capacity Releases: In 2022, NESO introduced an amnesty, allowing projects to leave the queue or reduce their capacity at little or no cost. 8.2 GW of projects applied to terminate contracts.

- Increased capacity via modelling changes: Changes to the way that battery storage projects were modelled reduced their grid reinforcement requirements.

- Flexible or “non-firm” connections: Connection agreements allowing the system operator to suspend power flows in extreme circumstances mean projects have been offered earlier connection dates.

- TMO4+ connection reforms: In 2025 connections moved away from a ‘first come first served’ approach towards a system of ’first ready and needed’. The reforms increased entry barriers (requiring planning approval and land rights) for Gate 2 entry, and encouraged stale projects to exit the queue - via project milestones and progression commitment fees.

- Connections 360: NESO have developed a tool to improve visibility of the electricity network - showing where substations have capacity or not. Similar tools have been developed by transmission and distribution owners.

- ET3 Incentives: The next control period for the transmission sector starts in April 2026. It includes financial incentives/penalties to get customers connected.

We suggest four further reforms that could further improve the rate of connection delivery.

1. Save valuable substation space by enabling direct connection at 400kV for sole-use demand projects

Building new transmission level substations is currently expensive and time consuming. It is possible to make much better use of the physical space at existing substations before triggering expansions.

The legal position of a demand project building 275kV/400kV circuits to a transmission level substation is highly uncertain. The 1989 Electricity Act does not clearly define whether immediate connection assets are classified as a transmission system, and thus require a transmission licence.

This legal uncertainty has led to wasting of valuable substation space. Currently, all demand connections are assumed to require a new transformer at the substation site to step voltage down to a distribution level (132kV or below in England and Wales), before electricity can be dispatched to the customer. This takes up scarce space on National Grid land. Instead, the transmission line could be extended at its higher voltage to the customer, and the step down transformer built on the customer’s site instead.

Ofgem have acknowledged the industry confusion, and in November 2025 stated that “These connections are not, in principle, prohibited under the Electricity Act 1989”.

Running a 400 kV cable from a National Grid substation to a privately owned demand project clearly isn’t forming a “transmission system” in any meaningful sense. The immediate fix would be for Ofgem to write a clarification letter to the industry, stating that:

“Running a 400kV/275kV sole-use connection from a National grid substation to a single customer location, to step down voltage for the customer’s own demand/generation does not constitute a “transmission system” for the purposes of the Electricity Act 1989.”

Ofgem have already acknowledged the potential for this clarification letter in their Demand Connections Reform update dated 13th February 2026. In the longer term, the Electricity Act 1989 should be updated to reflect the realities of large demand customers that weren't envisioned at the time of the legislation. The clarification letter will unlock space at transmission level substations much more quickly than legislative change.

2. Extend User Self-Build Distances

The Connection and Use of System Code (CUSC) is the contractual framework that governs the transmission connections process and use of the transmission network. While some network activities must be undertaken by Transmission Owners, others are ‘contestable’ and can be undertaken by the network user instead.

Contestability is restricted to the construction, financing and maintenance of ‘connection assets’, which are defined as the assets solely required to connect an individual user to the transmission system. For instance, the electrical circuits that run between a single industrial electricity user and the nearest transmission substation would be considered connection assets, and could be self-built under a User Self-Build agreement. This creates competition, potentially speeding up connections and reducing costs.

However, the CUSC currently limits the length of these contestable connection assets to 2 kilometres or less. Extending the 2 kilometre limit would give customers more land availability for their projects, improving their chances of securing sites that can gain planning permission.

There is already a code modification process underway (CMP 414) to extend the 2 kilometre limit. Submission of the final modification report is now expected in September 2026. CMP 414 is itself a merger of two earlier modification proposals (CMP 330 and CMP 374). CMP 330 is related to the user self-build extension and was first raised in 2019. Great Britain needs to increase the user self-build limit, not spend another 7 years arguing over it.

The Energy Secretary should make a statement supporting the extension of the user self build limit, and tell the industry to adopt the code modifications as soon as possible. If the industry isn’t able to adopt the appropriate changes, the Government should use powers under the Planning and Infrastructure Act 2025 to amend the codes directly.

3. Halve the time to deliver new transmission substations by allowing independents to build

2004 marked a step change in the competitive environment for grid connections. The first licenses were awarded for Independent Distribution Network Operators (IDNOs) allowing licensed independent providers to deliver last mile connections at distribution level voltages, breaking the monopoly position of regional distribution companies.

Great Britain now has twenty six licensed independents operating at distribution level, revolutionising the periphery of the distribution network. Over 1.5 million customers are served by independents and 70-80% of new connections adopted by IDNOs. There is no equivalent licensing regime available at transmission level.

Independent providers have been trying to move up the voltage scale for years. Eclipse Power Transmission applied for a localised transmission licence in February 2023. There is little evidence of an Ofgem response. Instead, in October 2023, Ofgem issued an open letter suggesting that the benefits of competition from IDNOs in higher voltage connections “may need to be reviewed” and expressed “particular concerns for IDNOs seeking to connect directly to the transmission network”.

The energy regulator’s stance reduces the scope for competition in transmission connections. Their own proposals to increase competition in transmission are also inherently limited. The Competitively Awarded Transmission Owner (CATO) is an attempt to introduce competition in onshore transmission and was first consulted on by Ofgem in 2015. In brief, the CATO system allows new and separable transmission projects to be competitively tendered.

However, the CATO regime fails to introduce competition at the point of project origination, as explained by Adam Bell. The mechanism for selecting new projects is inherently ‘top down’, rather than being initiated by the customer. NESO proposes strategic grid upgrade projects and passes them to Ofgem to confirm their eligibility. It took until December 2024 for Ofgem to consult on the first project to be competitively tendered, part of a new circuit between South West Scotland and North West England. In April 2025, Ofgem were unable to confirm the needs case for the project.

The monopoly on originating new transmission projects could be broken. A demand-side customer could approach an independent provider to find an unconstrained part of the transmission network. The independent could apply for a single point of connection with the relevant Transmission Owner, and then build their own substations and shared-use network downstream of that single connection point.

This offers a much faster way of building out new substation infrastructure. Existing networks have to go through a multitude of regulatory approvals before work can commence and their investment can be added to their regulated asset base. For incumbents, site selection itself becomes a careful tradeoff, looking to satisfy multiple prospective connecting parties. For example, the major and much needed substation expansion at Uxbridge Moor on the Western outskirts of London was first open to public consultation in 2023 and is expected to energise by 2029.

By contrast, an anchor demand customer, providing their own capital, can catalyse a much faster deployment with independents confident of delivering substation builds in around three years. It is important that private capital funds these projects without transferring cost recovery to network customers. Removing the risk of investment being socialised across the wider system reduces the time spent debating site location and requesting regulatory approval.

Adopting this model would also make excellent use of existing transmission infrastructure, allowing a plethora of demand, generation and storage projects to connect downstream of a single point of transmission connection.

We show three ways of making this revolution possible, with the fastest solutions first.

A. Individual licence exemptions

One option is for the Secretary of State to grant licence exemptions to specific transmission projects. There are already project proposals that are pursuing this route to market. Future Point Manchester proposes building its own 400kV substation, allowing 1.4 GW of demand to connect with an anticipated energisation date of 2028. To go ahead, this project would need to be classified as a license exempt private network, which would require sign off from the Secretary of State.

Relying on individual licence exemptions might be a pragmatic near term lever, but it isn't an ideal solution as exemptions are often time limited. This increases legal uncertainty for developers that are looking to deploy hundreds of millions of capital, where returns will be recouped over many years.

B. New class exemption for Growth Zone Transmission Interfaces

Another way to increase competition would be via the creation of a new class exemption under Schedule 5 of The Electricity (Class Exemptions from the Requirement for a Licence) Order 2001.

There is precedent for a change of this nature - in 2024 a new class exemption was added for array transmission, which allows the cables between offshore wind turbines and the offshore substation to be built at transmission level voltages without a licence.

A new class exemption for a Growth Zone Transmission Interface (GZTI) could be created. This would cover privately owned and operated substations that connect directly to the national transmission system at 275/400kV for the purpose of stepping down voltage to serve non-domestic demand and generation within a defined zone. All activities downstream of the transmission interface would remain exempt under Schedules 2-4 (covering generation, distribution and supply).

C. Creating a new licence for Independent Transmission Owners (iTOs)

The long term solution is a licensing regime allowing independents to operate at the periphery of the transmission network. Ofgem’s February 2026 demand connections reform update mentions the “potential development of a dedicated Independent Transmission Owner (iTO) licence” but it is only a “medium term ambition”. This should be a clear priority for Great Britain as it has the potential to dramatically improve connection speeds and allow incumbents to concentrate on their strategic transmission upgrades.

The government should set Ofgem an 18-month target to implement an iTO licence regime. It should allow independent providers to build and adopt limited amounts of transmission level infrastructure that enables the connection of downstream demand, storage and generation projects.

4. Deliver full grid queue visibility and more co-located projects

For all the talk of the grid queue, there is no single place where this queue of projects is transparently documented.

NESO manages the Transmission Entry Capacity Register, which holds details for generation and storage projects connecting at transmission level, as well as larger distribution connected projects. The Embedded Register lists generation and storage projects in Scotland. The Embedded Capacity Register fulfills a similar role at a national level, and is held by the distribution networks.

There is very little visibility of demand side projects that are already connected or seeking connection.

Transmission and distribution networks should make the list of demand side customers holding a connection offer publicly available, so that a national demand capacity register can be published. This could be achieved through a licence condition modification by Ofgem, placing a direct obligation on network companies to publish this information. Projects below a certain size threshold (e.g. 1 MW) and those with national security sensitivities could be excluded from this requirement.

Full visibility of demand side connections could help Britain make better use of its existing network infrastructure, by pairing up demand, storage or generation projects. This enables multiple projects to use a single substation bay or share the cost of new connection assets.

We are already seeing evidence of the existing queue reform process deprioritising co-location. The TMO4+ queue reform process understandably prioritised projects with planning permission, but may have had a selection effect. If getting planning permission from a battery-only site is easier than for a site that combines solar and batteries, then the reformed queue will be biased against co-located projects, in turn wasting scarce substation capacity.

Improving data availability is an easy win for improving Britain’s connection speeds. As well as publishing the demand queue, there are further opportunities to improve grid efficiency. Ultimately, developers want to connect to the network in a timely manner. In an ideal world, they would be provided with the data that allows them to connect in a way that minimises the need for network upgrades. We suggest:

- Adding geospatial data to all connection registers

- Disclosing capacity headroom at each substation - especially at transmission level

- Disclosing which projects are triggering network reinforcements

- Improving visibility of future network outage windows

- Standardising equipment data so developers can run their own power flow studies

Fixing the grid is absolutely essential for Britain’s current and future prosperity.

There are huge gains on the table for countries that can move quickly. Whether investing in AI data centres or green energy projects, global capital responds to regulatory coherence, predictability and speed. Our grid is a public good: it is the bedrock of not just household electricity use, but for our industry and public services too.

The reforms we outline, if adopted swiftly, would represent a significant upgrade in Britain’s capacity to build.

For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]