Table of Contents

- 1. Summary

- 2. The challenge: AI’s growing climate impact

- 3. Britain’s advantage: a greener grid

- 4. A virtuous cycle: How data centres can support cleaner, cheaper power

- 5. Case study: Ynys Môn, Britain’s energy island.

- 6. Conclusion

- 7. Authors

Summary

The coming decades will be defined by our ability to adapt to two great challenges: AI and climate change. To prevent further climate disaster, humanity must reduce greenhouse gas emissions to net zero. We will also have to prepare for AI, harnessing its potential and protecting against its risks.

But are AI and climate action in conflict? We find that, in most countries, the answer is yes. In Britain, however, the answer is probably no.

This is for three reasons:

- Britain has already made great strides towards decarbonising the grid, so a new data centre here produces 70% less emissions each year than one in Saudi Arabia, 43% less than in the US, and 31% less than in Germany.

- Electricity demand from data centres increases the viability of new, green infrastructure. Demand, particularly in locations or at times of high supply, makes the build out of renewable energy required for Clean Power 2030 more achievable and more affordable. Nearly half of the cost of renewable energy comes from building and managing the grid, and data centre demand reduces the share of this that is paid by ordinary households.

- The global and highly mobile nature of investment in data centres means that data centres not built in the UK are likely to be built elsewhere on dirtier grids. This means that building a data centre in the UK can lead to a net reduction in global emissions.

The whole point of decarbonising the grid is to enable Britain to use energy productively, without damaging the climate. Moreover, extra demand on the grid will help make new wind and solar projects more viable, further speeding up our transition.

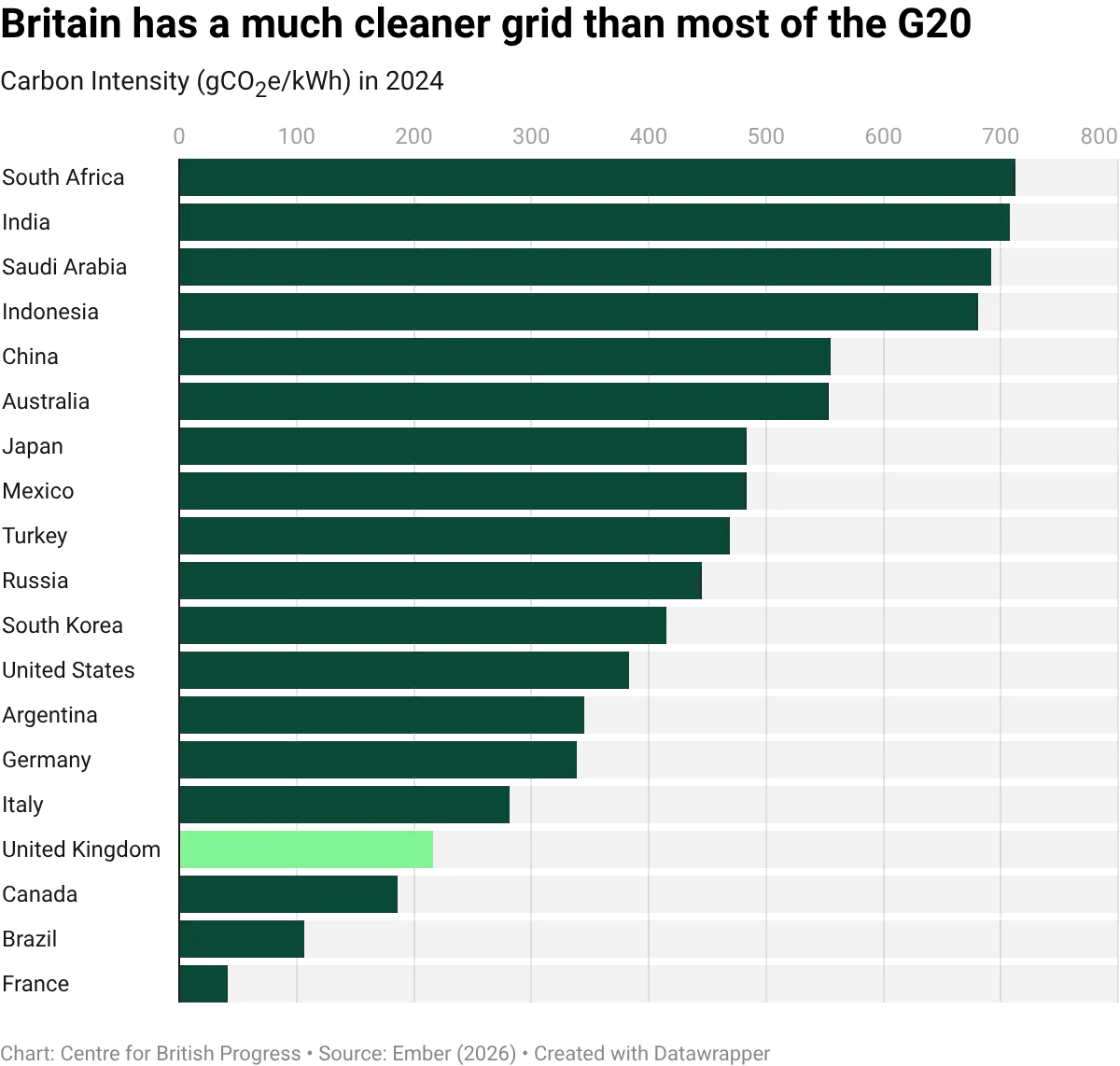

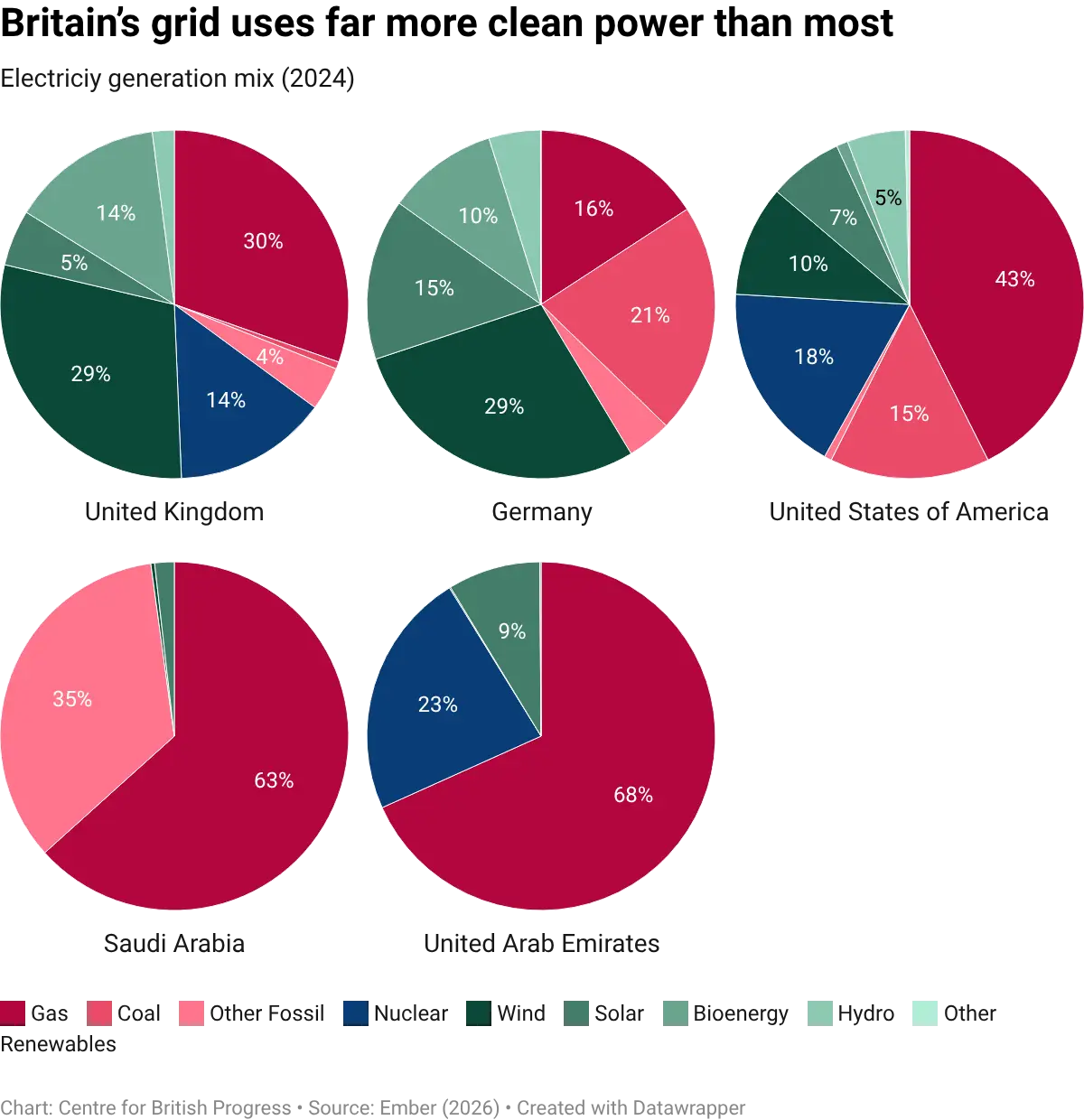

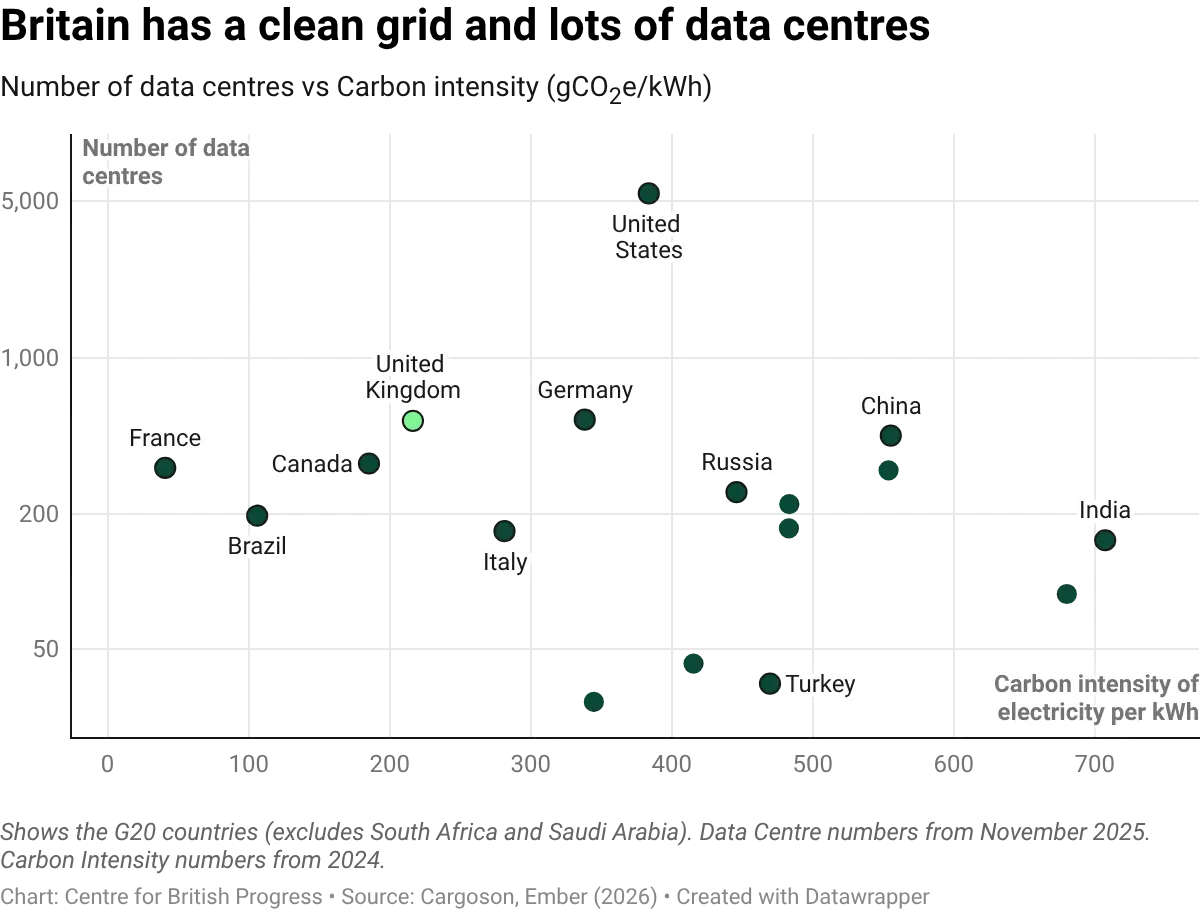

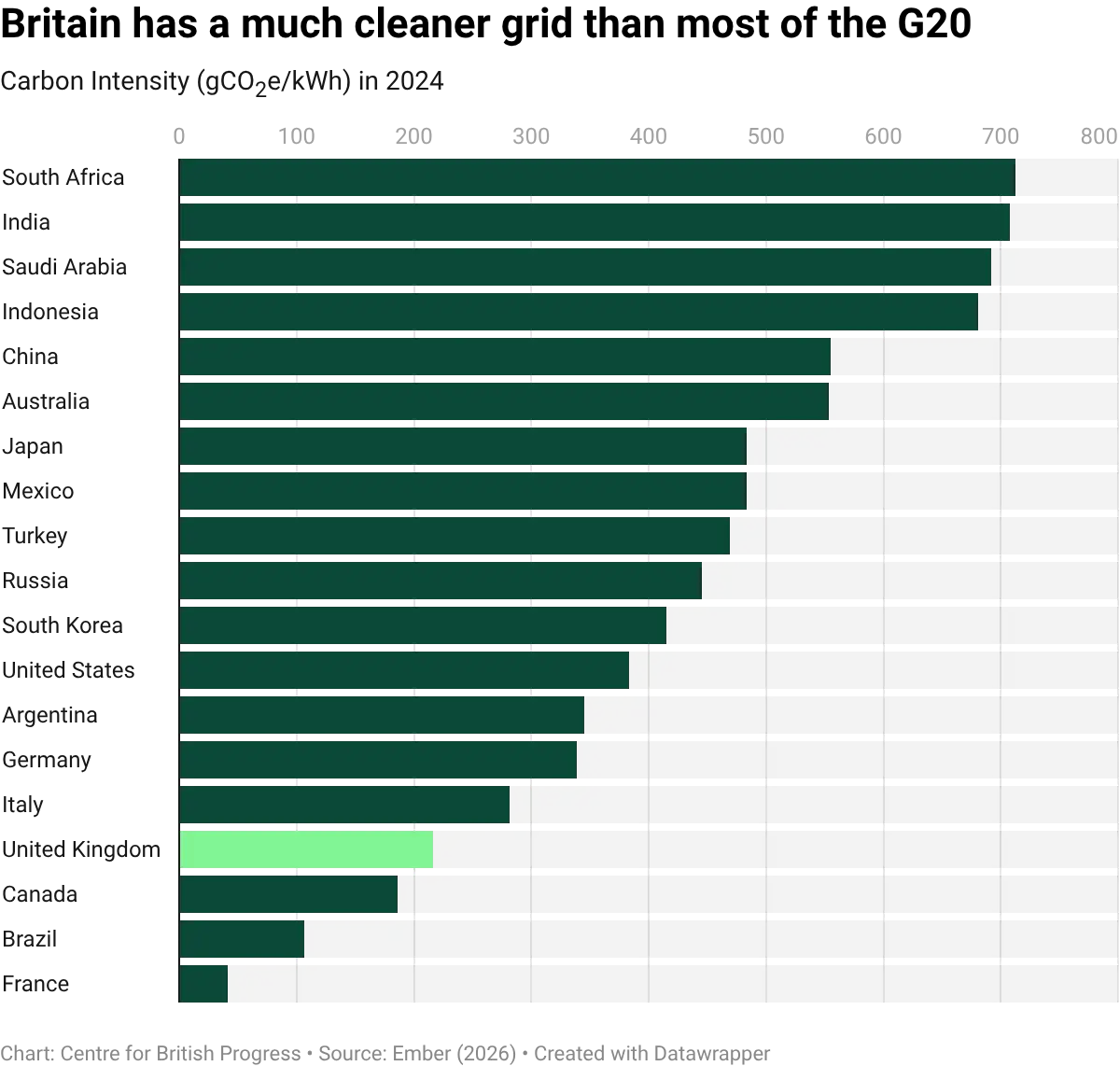

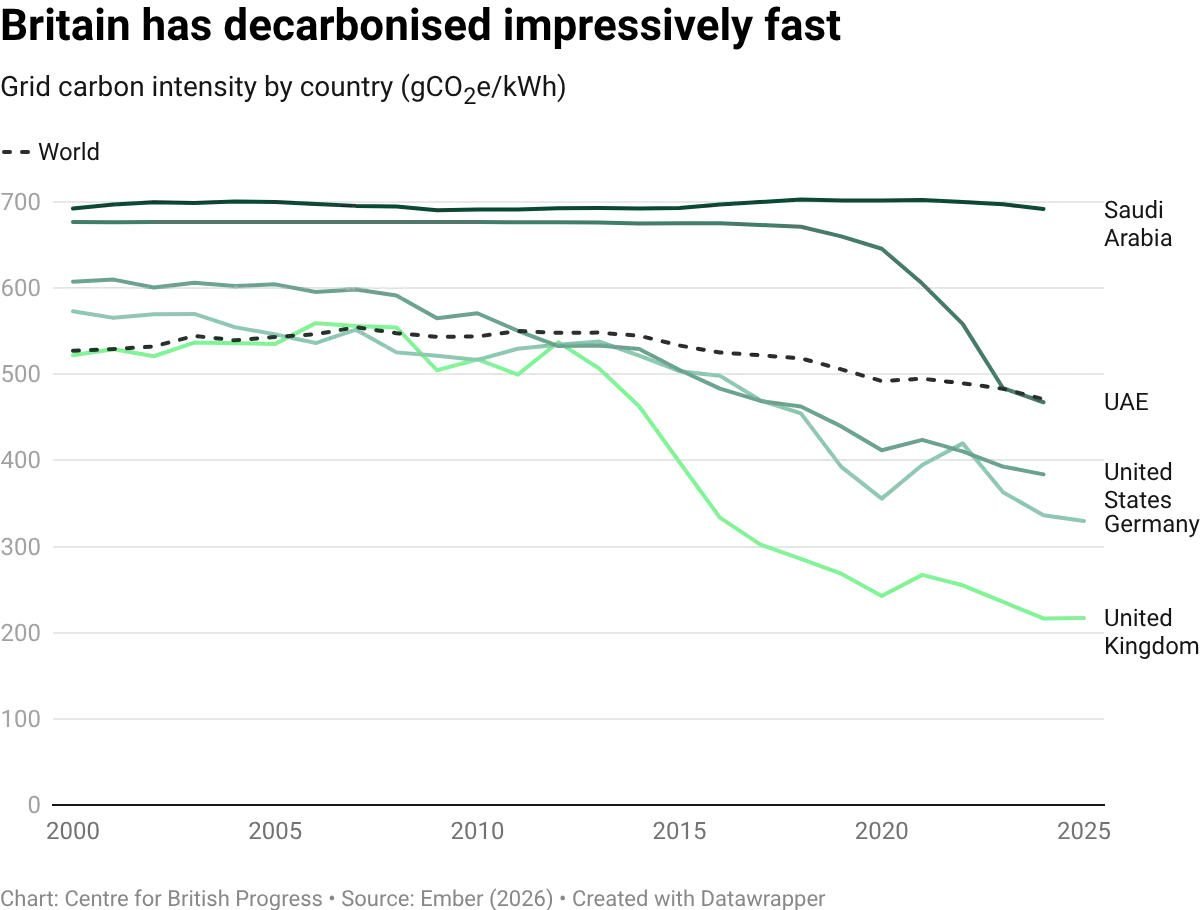

Britain is unusual in having a lot of data centres and a green grid. The UK hosts the third most data centres in the world, by both count and by energy use. Over the last two decades, Britain has outperformed its peers in decarbonising its grid, removing coal and switching away from natural gas, towards wind and solar, with baseload nuclear. This means that a unit of electricity generated in Britain produces a third of the CO2 as would be produced in Saudi Arabia, and just over half that produced in the US.

Energy demand is, in itself, neither good nor bad for the planet. Its impact depends entirely on how that demand is supplied. For fossil-fuel intensive grids, like Saudi Arabia or the US’s, more demand creates more emissions. But for renewable-intensive grids, like Britain’s, more demand has the opposite effect: enabling and encouraging even more renewable projects to come online, and paying for much-needed transmission infrastructure.

As the global economy becomes more and more dependent on, and driven by, AI, those who care about climate change should prioritise building AI infrastructure in countries with the cleanest grids: countries like Britain.

The challenge: AI’s growing climate impact

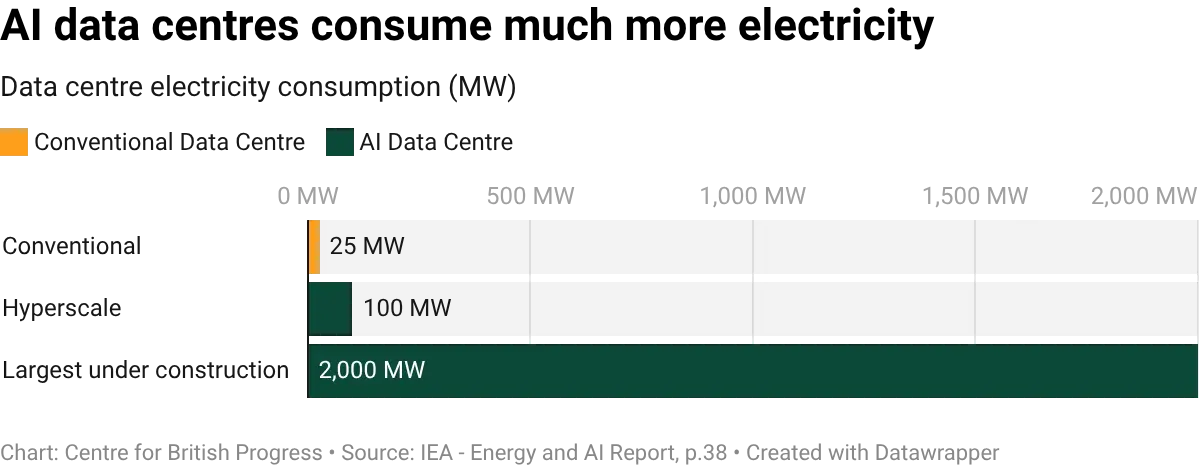

AI data centres consume vast quantities of energy to train new AI models and run existing ones. Since the release of ChatGPT in 2022, data centre construction has increased by 400%, and data centres have become more energy intensive. Globally, data centres use almost twice the amount of electricity as the UK does each year.

AI data centres are far more energy-hungry than traditional data centres, such as those used for web hosting, online communications, and video-streaming. Traditional data centres act like a library, storing and retrieving data. Data centres used for AI training, inference and deployment act like a brain working to solve a puzzle. This means that responding to a chatbot prompt can use 10 times more energy than a standard Google search.

The rise of AI accounts for the increase in both the number and energy intensity of data centres:

- Data centres now consume roughly 1.5% to 2% of all global electricity. In hubs like Ireland, or Virginia, they account for 20% to 30% of total national/state power consumption.

- A traditional server rack typically uses 5–15 kW of power. Modern AI-ready racks can require 60–100+ kW, generating more heat, which in turn requires more energy for cooling.

Both the International Energy Agency (IEA) and financial analysts have recently revised their forecasts of data centre demand upwards. Total demand is projected to reach 1,350 TWh by 2030 – a 220% increase from 2023 levels. The main bottleneck in most countries is grid connections. Across the world there is a substantial backlog of data centre plans waiting to be built, with huge potential economic benefits for the countries that can move fastest.

In the US and China, the countries with the most large-scale data centres, much of new AI demand is being met by fossil fuels. More energy demand on carbon-intensive grids is likely to be bad for climate change, especially if those countries do not have plans for rapidly decarbonising their grids by switching to nuclear and renewables.

In Saudi Arabia, a 100MW data centre (used, for example, for training a large language model) produces the equivalent of 552 thousand tonnes of carbon emissions every year, equivalent to adding 275,000 new petrol cars to British roads, or the carbon impact of 2000 people each making a transatlantic flight, every day, for a whole year.

For the UAE, another oil-rich country, but one that has rapidly built out nuclear and solar capacity, the situation is better, but a 100MW data centre there still produces 373 thousand tonnes of carbon emissions (equivalent to 186,000 new petrol cars in the UK).

In the US things are slightly better (306,000 tCO2/yr), as its gas-heavy grids are mixed with new solar capacity, and Germany is better still, despite still having coal on its grid (268k tCO2/yr).

Britain, however, beats them all.

Britain’s advantage: a greener grid

When it comes to providing green electricity to data centres, the UK performs better than almost all its comparable peers. Since the UK has one of the greenest grids in the world, a new data centre here produces a third of the carbon emissions produced by an equivalent data centre in Saudi Arabia, about half that produced in the US, and about 30% less than Germany.

Furthermore, if the Government achieves its ambition of clean power by 2030, British data centres will be close to carbon-neutral. Britain not only has a greener grid, but has decarbonised more rapidly. The Government’s Clean Power 2030 plans mean that we are on a greener trajectory than other comparable countries.

The UK has the third most data centres in the world, by both count and by energy use. Most of these are traditional data centres, rather than AI ones, though the number of AI data centres is projected to rise substantially. Data centers now account for approximately 8–10% of the UK’s industrial electricity demand.

Britain has a lot of data centres for several reasons. The UK is geographically well placed for transatlantic subsea cables connecting the US and Europe, and a temperate climate reduces cooling costs. Our high concentration of financial and tech firms, who often require low-latency infrastructure, mean that data centres need to be physically close to business activity. Data centres are critical for national security. Indeed, in 2024 the UK Government designated data centres as Critical National Infrastructure, providing a more stable regulatory environment for investment. These factors, combined with established data privacy laws, maintain the UK's position as a primary European hub despite high domestic energy prices and grid capacity limitations.

Of the top four countries for the number of data centres, Britain has the greenest grid. Britain is unusual in having a lot of data centres and a green grid.

This green advantage wasn’t always the case. In 2000, a unit of electricity generated in Britain came with a similar carbon footprint to one produced in the US or Germany. Since then Britain has rapidly decarbonised: replacing coal completely and reducing our reliance on natural gas.

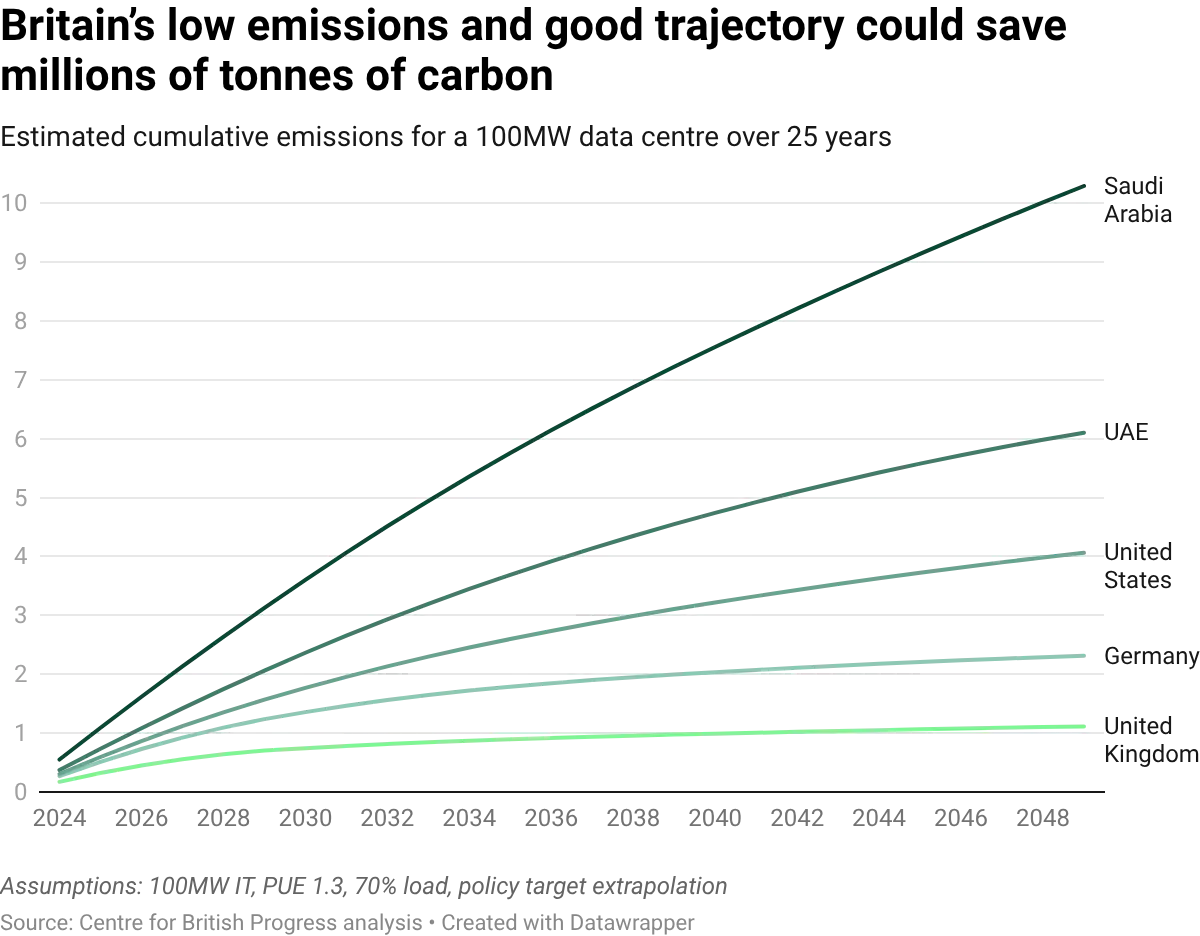

Over the lifetime of a data centre, the difference in carbon emissions quickly stacks up. Adjusting for each country’s policy targets, we estimate that a data centre in Saudi Arabia would produce 8x as much carbon emissions over 25 years than if it were built in the UK. In the US, the figure would be 4x as much, and in Germany, twice as much. Of course, the true figure depends on the rate of decarbonisation the UK and other countries achieve.

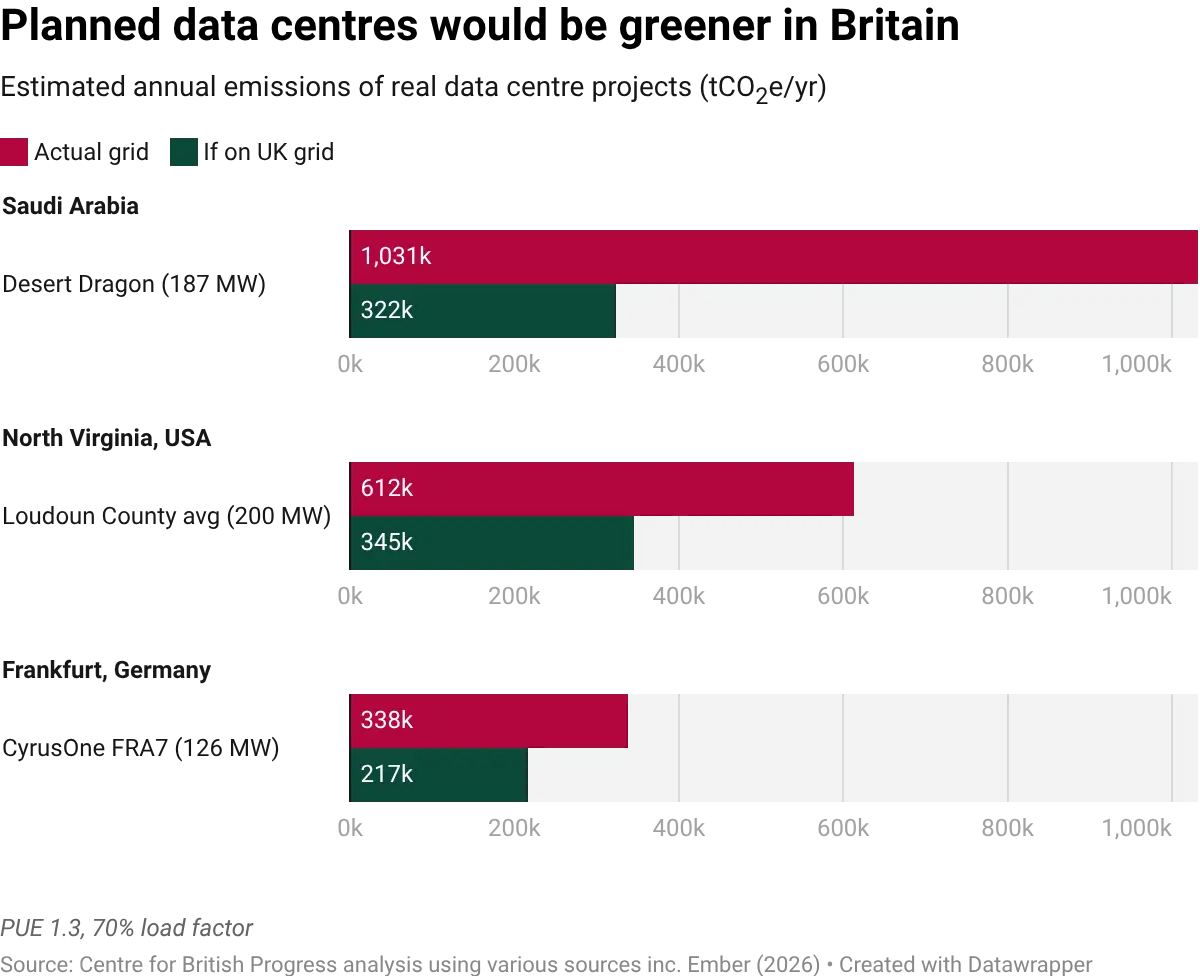

To make this more concrete, we look at individual data centres, and their carbon footprint in their respective countries.

- The Desert Dragon Data Centre is a flagship 187MW project in Saudi Arabia, designed to be one of the region's most advanced hubs for AI and high-performance computing, as part of Saudi Arabia’s Vision 2030 digital transformation. Since Saudi Arabia’s grid is almost entirely dependent on fossil fuels (oil and natural gas), the project is estimated to produce the equivalent of a million tonnes of carbon emissions every year.

- Loudoun County in North Virginia is known as “Data Center Alley”, a primary global hub for cloud services and digital infrastructure. Because the local grid still relies significantly on a mix of natural gas and coal, an average data centre of this scale in Loudoun County is estimated to produce roughly 612,000 tonnes of carbon emissions every year. This is nearly double the emissions the same facility would produce if it were operating on the UK’s increasingly decarbonised grid.

- CyrusOne FRA7 is a major facility in Frankfurt. While Germany has made significant strides in renewable energy integration, the current grid mix results in the project being estimated to produce 338,000 tonnes of carbon emissions annually. By comparison, if this specific facility were located in the UK, its annual footprint would drop to approximately 218,000 tonnes of CO2 equivalent.

A virtuous cycle: How data centres can support cleaner, cheaper power

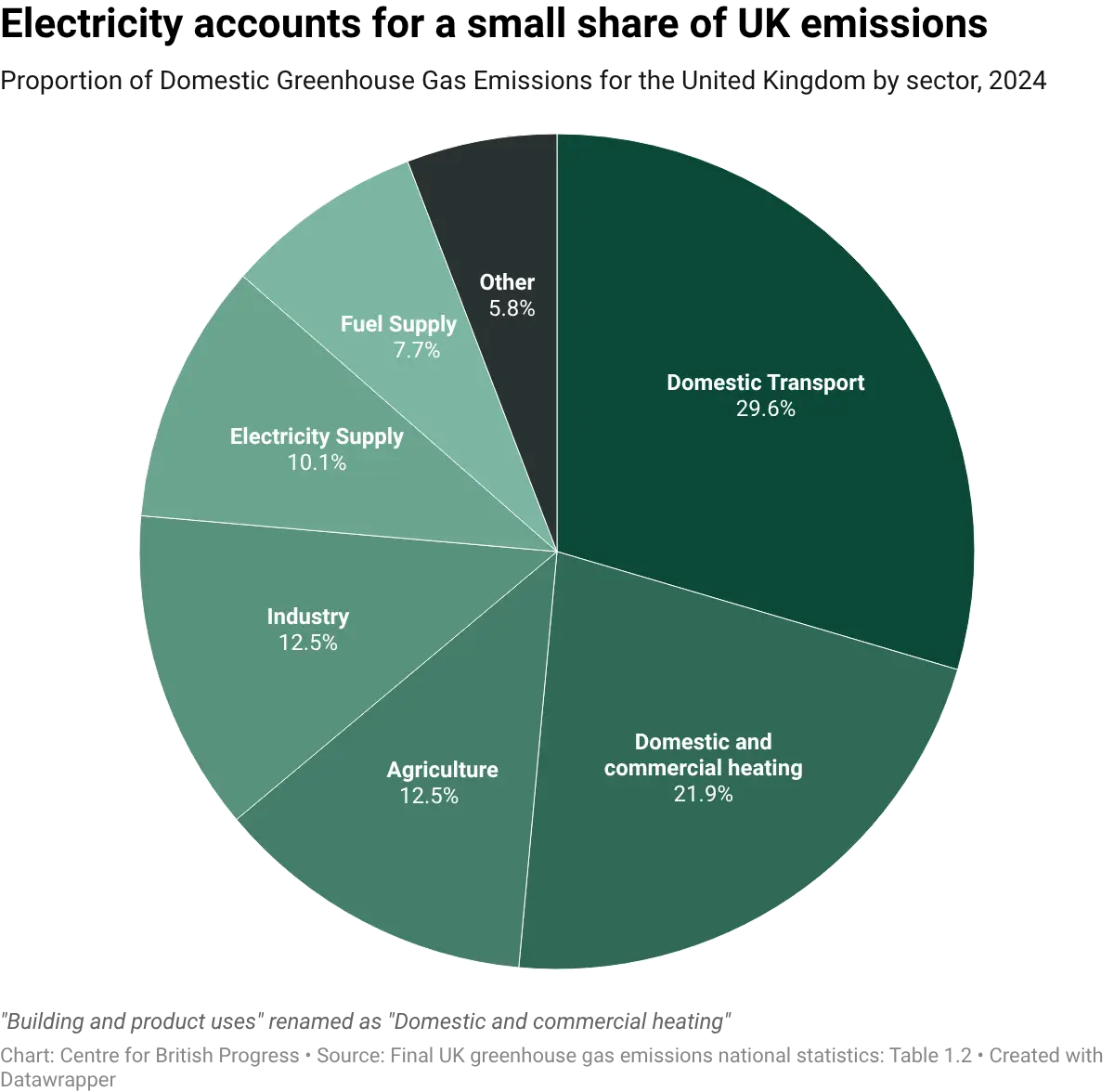

For countries like the UK, which have largely decarbonised their grids, tackling climate change means electrification – switching other energy uses from fossil fuels to electricity. Only 10% of UK emissions are from electricity supply, and this continues to fall as more wind farms and solar projects come online. The big challenge is getting domestic transport, domestic heating and industrial uses of fossil fuels to decarbonise. For these purposes, the most important factor is the relative price of electricity compared to petrol (in the case of cars) and electricity versus gas (in the case of domestic heating).

Even without a fully decarbonised grid, the climate benefits from households switching to electric vehicles, away from petrol, and to heat pumps, instead of using gas. In the context of one of the greenest grids in the world, this change is imperative.

Britain’s electrification, however, is held back by our high electricity prices. Electricity is much more expensive than gas, making heat pumps uneconomical for many households. And whilst most electric cars cost less in electricity than a petrol car would in fuel., the saving needs to be large enough to offset the higher repair and insurance costs.

Why is electricity so expensive? One key reason is that renewables, while facing a very low marginal cost of generating electricity, come with significant transmission and infrastructure costs. Indeed, these costs are much higher for renewables (particularly offshore wind) than for nuclear or gas.

- National Investment: Ofgem’s framework allocates £70 billion for grid upgrades, primarily to support the Government’s goal of 50GW offshore wind by 2030. This is mainly paid for through consumer electricity bills.

- Connection Charges: Offshore wind costs up to £1.5M per MW for subsea cabling, while onshore wind and solar range from £100k–£400k per MW depending on substation proximity. Although the immediate cabling (at point of construction) is paid for by wind farms, future upgrade work to the wider system adds significant cost, and is borne by consumers.

- Transmission Network Use of System charges are fees paid by electricity generators and suppliers to National Energy System Operator (NESO) to cover the costs of building, operating, and maintaining the UK’s high-voltage transmission network. These increased to £8.9 billion in 2026. These charges are ultimately passed on to consumers.

- Constraint costs: Managing grid bottlenecks costs over £1.7 billion each year.

These costs are substantial, and they are also fixed; i.e., they do not vary depending on usage. In a sense this means the costs, once baked in, are unavoidable. But it also means that more electricity demand reduces the average unit cost of supplying the electricity, and increases the viability of new renewable projects. Even without new projects, more demand pays for maintenance and upgrades of existing infrastructure, making electricity more affordable for ordinary consumers and thereby supporting transitions away from fossil fuels.

To continue decarbonising our economy we will need to connect further clean generation and do so at a competitive price. There are three main mechanisms through which increased electricity demand helps make renewable energy viable:

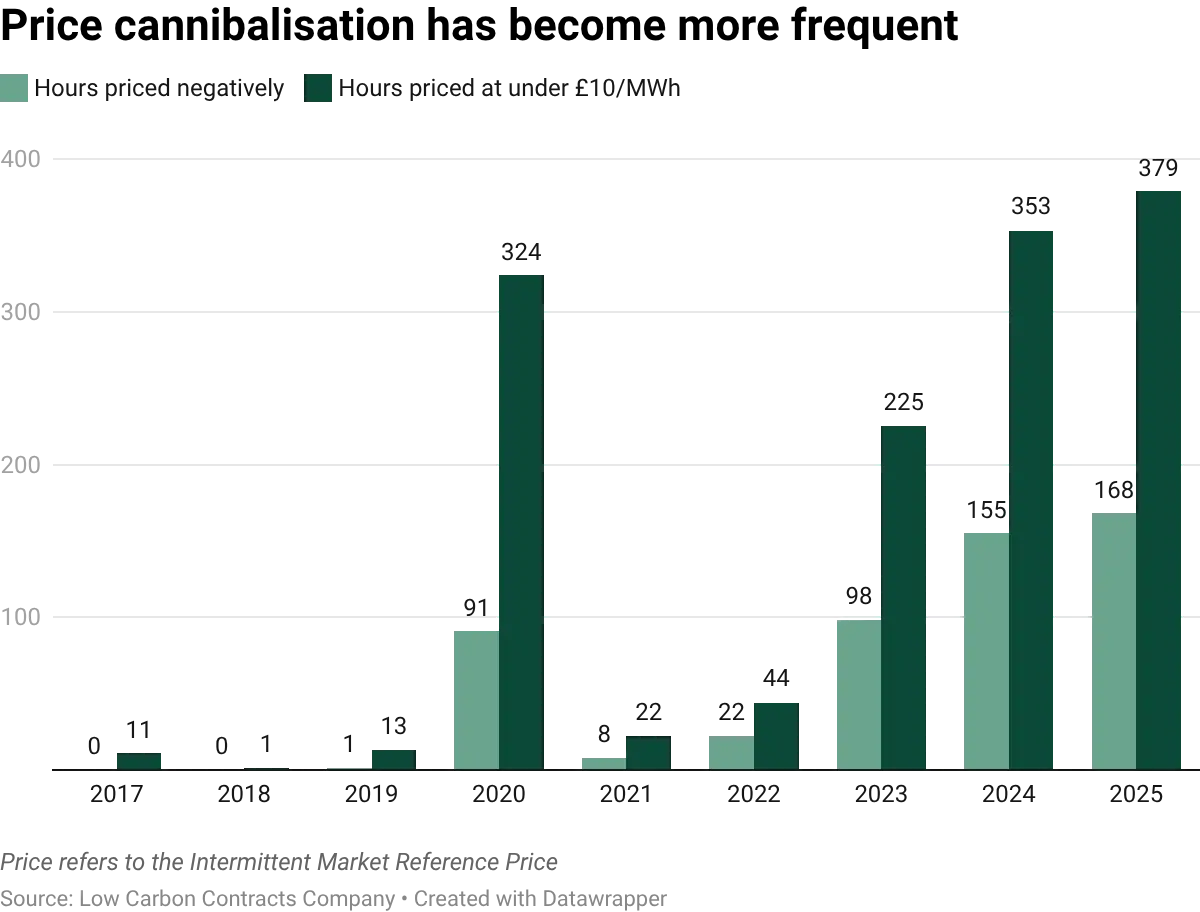

1. Stopping price cannibalisation

When solar and wind generation is high but demand is low, wholesale prices crash (sometimes into negative territory).

This is known as price cannibalisation: an excess of supply means that prices collapse. For new renewable projects to be viable, this needs to happen less frequently, for a smaller proportion of the year.

Analysis of the UK's Day-Ahead market shows a rising frequency of negative price hours, with over 200 hours in 2023. As more renewable projects come online, this could increase, if it is not met by a corresponding increase in demand.

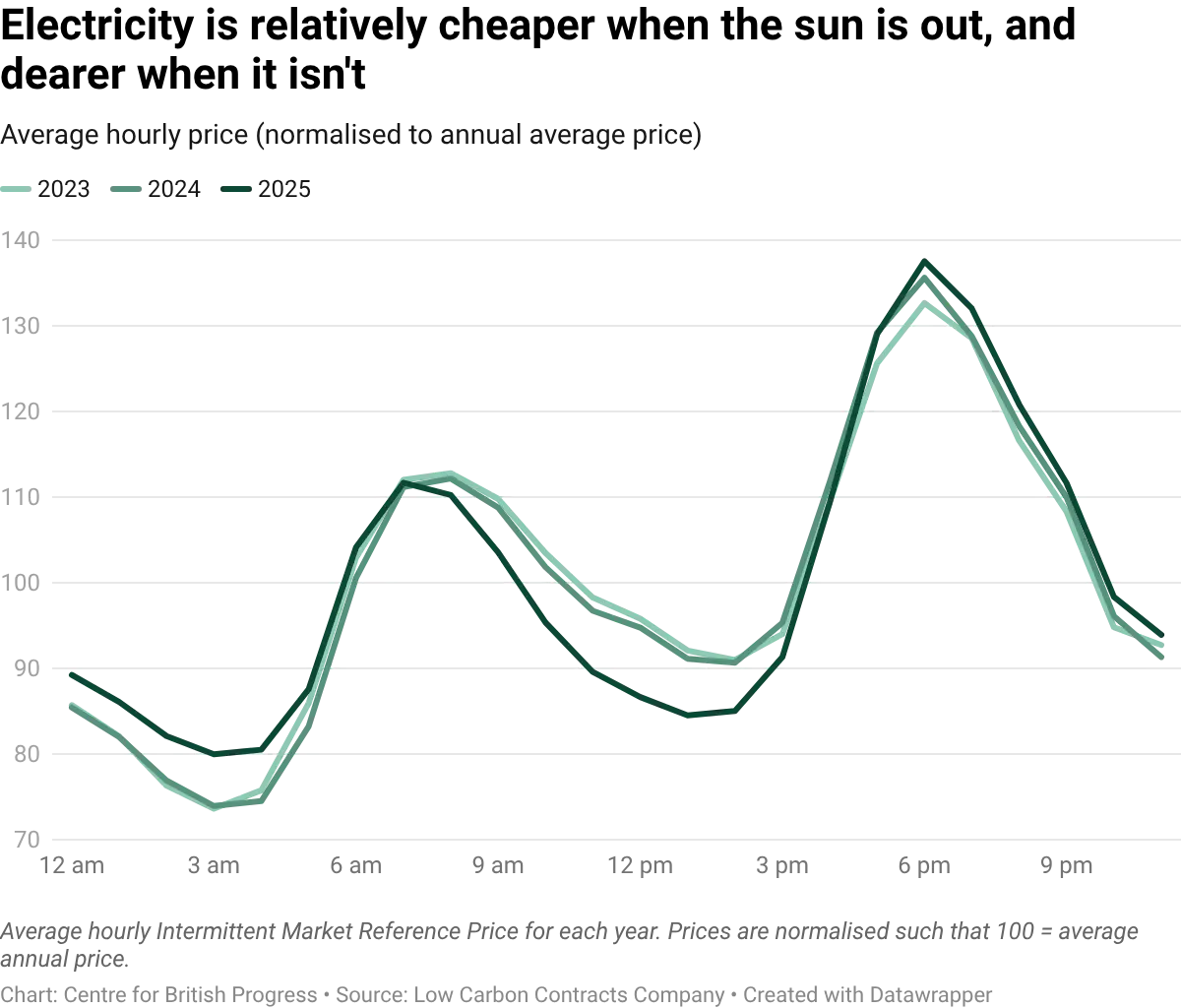

High demand, particularly demand that correlates with, or is consistent through, periods of oversupply (when it is very windy or sunny) can prevent prices from falling to zero. By absorbing energy during peak production, these loads keep wholesale prices stable, ensuring renewable generators receive a "capture price" high enough to service their debt.

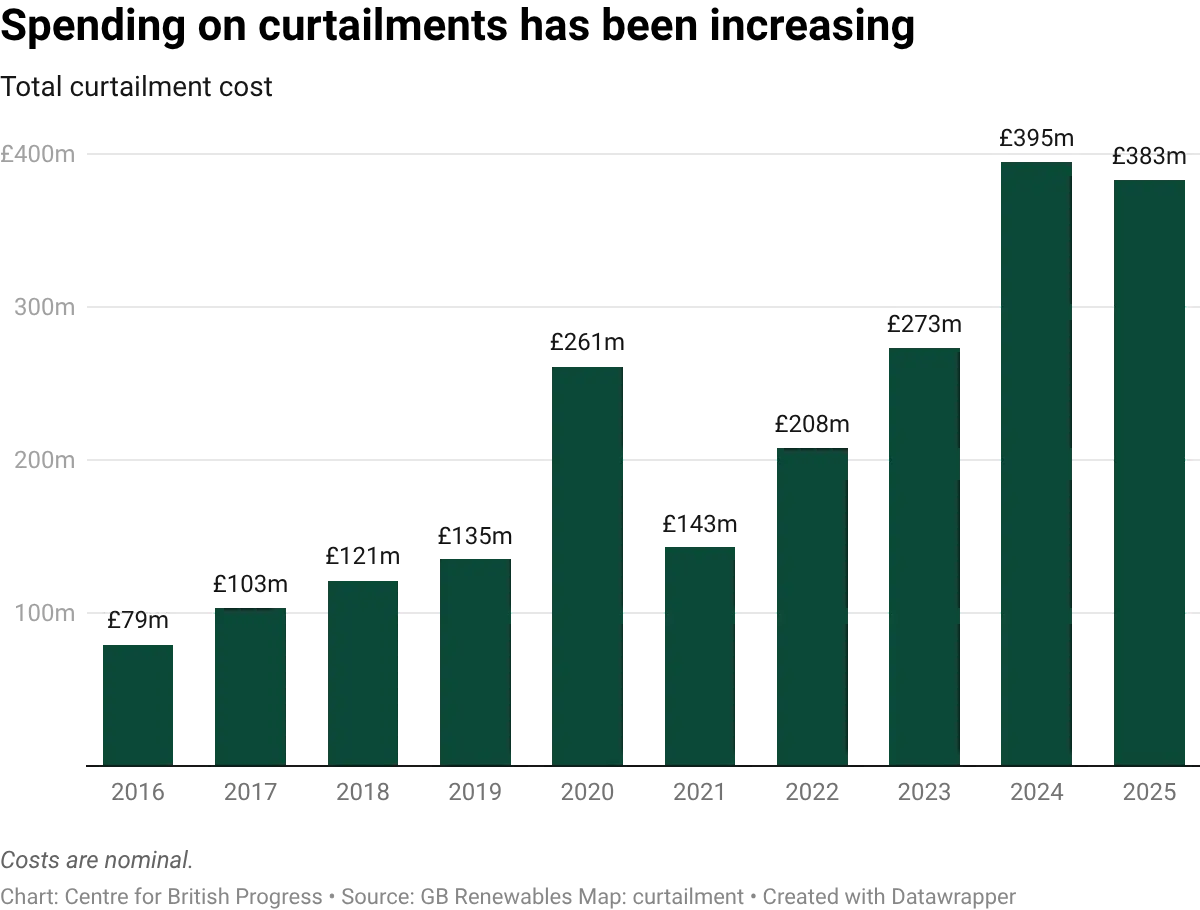

2. Reducing curtailment wastage

Curtailment occurs when the National Grid pays generators to turn off solar or wind farms because there isn't enough demand or cable capacity to use the amount of electricity

In 2025, the UK spent over £380m on curtailment, much of it on wind farms.

Curtailments can be reduced either by locating demand alongside places with high supply (i.e. placing data centres near wind farms), or by increasing the level of transmission to other parts of the grid, or by allowing prices to fall in different locations depending on local supply (locational or nodal pricing). For a generator, high local demand means they can sell 100% of their potential yield rather than having 5–10% of their annual energy "thrown away" by the system operator.

3. Improving the “merchant tail”

New UK renewable generation projects rely on a Contract for Difference (CfD) system, which guarantees generators a price per MWh for 15-20 years. However, the project's total value depends on the “merchant tail”, in other words, the full net present value of the project which includes revenue earned after the subsidy ends.

This projected long-term demand growth gives investors confidence that there will be a robust market for their power in the 2040s and 2050s, making it easier to secure low-interest financing today. Projects are more likely to go ahead if there is expectation of demand after CfDs expire.

If we do not boost demand, we could end up in a doom loop: falling demand raises the unit costs borne by households for grid infrastructure. This reduces consumption even further, and makes new renewable infrastructure less viable, reducing longer run energy supply. It also encourages grid defection, where individuals and companies pursue off-grid options, and therefore spend less on maintaining the national grid. In this context, data centre demand is enormously helpful: they could play a similar role to historic “industrial loads” in making the transmission and infrastructure costs more affordable for households.

The role of demand flexibility

In periods of low renewable production, where the UK is more reliant on gas, data centres can add pressure on the grid and can increase prices. This is also the point at which data centre demand is most likely to be carbon-intensive, as marginal electricity demand increases gas consumption.

The Government is already offering discounts to data centres to locate themselves in places that are favourable for balancing the grid; i.e., near to renewable generation. This reduces the proportion of the year that data centres are increasing demand for gas, and also means that there is less wastage during periods of high renewable supply (when it is windy or sunny), and less curtailment.

It is unrealistic to expect data centres to flex their energy use based on time of day: they are often supporting critical online systems that need to run at all hours, or at least at regular times. However, there are additional ways data centres could introduce flexibility:

- Onsite generation can plug periods of low renewable generation on the grid, reducing reliance on gas. Aside from local renewable options (such as solar), data centres could use green fuels such as Hydrotreated Vegetable Oil (HVO), which uses waste oils. AWS has used these fuels in data centres in Ireland and Sweden, and has plans to roll out to all data centres.

- Battery storage: data centres could build or finance batteries to store electricity during periods of renewable over-supply (when it is cheaper), and use it when gas is setting the price. This is likely to become a more attractive option as battery storage becomes cheaper.

- Workload optimisation and time-shifting: data centres can shift demand to perform more energy-intensive tasks at cheaper times. Google, for instance, claims to already be doing this. The company recently said that it had “integrated a total of 1 gigawatt (GW) of demand response capacity into our long-term energy contracts with multiple utilities across the U.S.” In practice this means that they can shift non-urgent tasks (like processing YouTube videos, updating Google Photos, or training large AI models) to hours when the sun is shining or the wind is blowing.

These options can make non-firm grid connections viable. Since data centres are often most bottlenecked by speed of grid connection, some hyperscalers are willing to take non-firm connections, even if as a temporary measure. These connections do not guarantee firm power at all times, so involve some risk for data centre operators, unless they have decent backup options. The UK, Ireland and other countries have already begun offering these options.

The impact of global, and mobile, investment in data centres

Finally, it is worth emphasising the strong potential for investment displacement. Because of strong global demand for compute and data centre investment is highly mobile across borders, turning away projects in the UK does not eliminate them. It merely shifts the development to other countries, risking 'carbon leakage' as they connect to dirtier grids.

Global demand for data centres is strong, persistent and mobile for two main reasons:

1. Data centres have become critical infrastructure

As the economy becomes more digitised, data centres are being treated increasingly as critical infrastructure by firms and governments. Ever more sensitive and personal data is held in data centres and much of this has to be on domestic soil, for legal and security reasons. Furthermore, many more key services – from running hospitals to managing traffic – depend on the continuous functioning of fleets of data centres. Disruption to the country’s digital backbone threatens essential services.

In the UK, this has led to the Government designating data centres as Critical National Infrastructure, placing them on the same level of strategic importance as water and power. This centrality means that demand for data centres is less elastic, i.e. less responsive to the price and availability of land and energy. Because modern commerce, healthcare, and government services are now hosted in the cloud, not having data centres is not an option. This means that, to a certain extent, data centres will be built regardless of the UK’s high energy costs.

2. AI has generated unprecedented demand

The second key driver of inelastic demand comes from the race dynamics of AI development. AI companies are fiercely competing to create ever more powerful frontier models. The possibility of a “winner takes all” scenario, where a model could become recursively self-improving and guarantee one company’s position at the frontier makes this race existential for AI firms. Because of the vast potential profits on the table from being at the frontier, AI companies have raised huge amounts of capital, which is largely being spent on building new data centres and the chips to go in them. Furthermore, AI companies are highly mobile, and can build data centres anywhere with reliable energy and decent legal infrastructure.

“Winner takes all” dynamics mean that companies are primarily optimising for securing more powerful chips quicker, rather than minimising the financial cost of building or running data centres. Even as grid connection costs rise and lead times for power extend towards the 2030s, firms continue to queue for capacity.

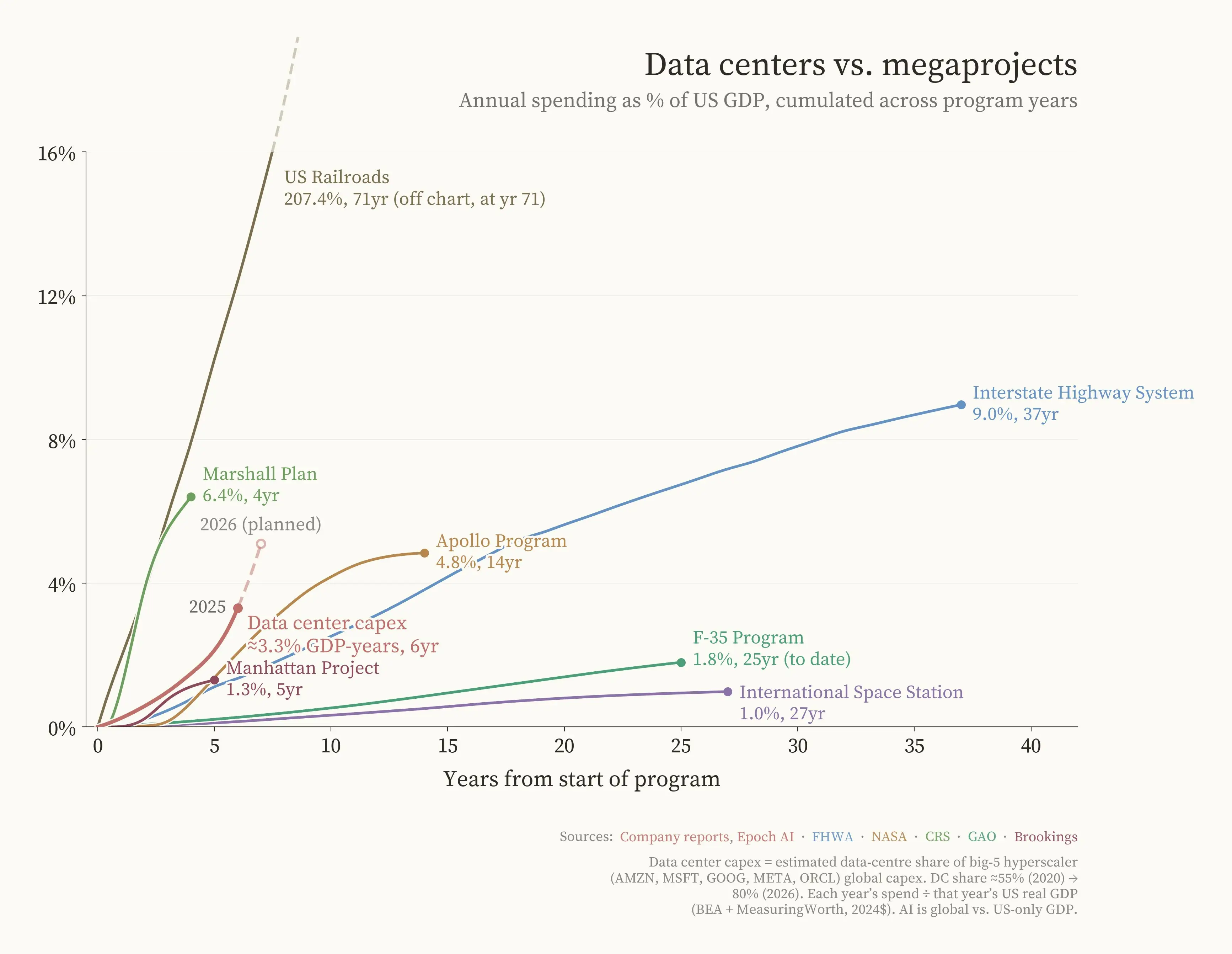

The graph below shows how US spending on data centres has taken off at a steeper gradient, as a percentage of GDP, than historic megaprojects, with the exception of US railroads.

Source: Fin Moorhouse

These race dynamics mean AI companies are less sensitive to energy prices or other costs, and more sensitive to speed and security.

Evidence suggests that data centre operators are increasingly willing to pay a premium for shovel-ready sites with secured grid allocations, often funding their own energy infrastructure or entering into long-term Power Purchase Agreements to bypass price spikes. This behaviour confirms that the utility of the data centre – providing the 24/7 always-on backbone for the digital economy – far outweighs its marginal cost. Consequently, the UK market continues to see record investment despite inflationary pressures, as the necessity of digital sovereignty and AI readiness makes data capacity a non-negotiable asset for national progress.

This extremely strong demand, combined with the mobility of AI companies, matters because it implies that if data centres are not built in the UK, they will be built elsewhere. Outside of highly sensitive uses, for AI data centres what matters is not so much location as the ability to build them at all. The number (or power) of data centres, globally, is insensitive to Britain’s ability or willingness to build data centres. If they are not built here, they will be built elsewhere.

This matters for climate change, because it changes the counterfactual. When assessing the carbon impact of a data centre, the relevant comparator is not if the data centre were not built at all, but if it were built elsewhere. If building the data centre in the UK is less carbon intensive than building it in the next best country (such as Ireland or Germany), then building a data centre in the UK can lead to a net reduction in global emissions.

Case study: Ynys Môn, Britain’s energy island.

Anglesey (Ynys Môn) is home to some of Britain’s most exciting energy projects. Most prominently, Wylfa, a former nuclear power station which operated from 1971-2015, was revived by this Labour Government as the home of Britain’s first Small Modular Reactors (SMRs), to be built by Rolls Royce. The site is slated for three 470MW SMRs initially, with the potential for eight in total. The aim is for them to supply power by the mid-2030s.

In addition to Wylfa, Anglesey and the surrounding area are home to:

- Alaw Môn solar farm, A 160 MW solar farm with integrated Battery Energy Storage Systems (BESS). It will connect via an underground cable directly to Wylfa’s substation (grid connection).

- Morlais tidal power, a tidal project west of Anglesey, which intends to deploy turbines before the end of the decade.

- Gwynt y Môr offshore wind, a 160-turbine farm (~576MW), east of Anglesey, that has been active since 2015.

- Awel y Môr offshore wind, a consented project adding up to 50 turbines (adding ~500MW), connecting to the Bodelwyddan substation, also east of Anglesey, in the Irish Sea.

- Mona offshore wind, consented in 2025, to be constructed east of Anglesey in the Irish Sea.

Anglesey’s green energy projects are made viable by a major, co-located set of data centre projects, namely the North Wales AI Growth Zone. The growth zone includes:

- Prosperity Parc, in Holyhead, is developed by Stena Line and Anglesey Land Holdings to host a massive AI data centre campus on the former Anglesey Aluminium site, using its grid connection and existing infrastructure. In March 2026, the Anglesey Freeport unlocked £25 million in seed capital to prepare the site’s infrastructure. The site has an AI focus, and is specifically designed for NVIDIA GPU clusters with liquid-cooled racks.

- Trawsfynydd, on the mainland in North Wales, is being developed as a secondary AI hub, focusing on sovereign UK government data, leveraging its own SMR development plans.

With 1.4GW+ of SMR nuclear power coming to Wylfa, and 500MW+ of offshore wind (Awel y Môr), the grid would actually struggle to transport all that energy to other parts of the UK. By having multiple data centres right next to the source, the energy is consumed locally. This local loop makes the business case for Wylfa Newydd much stronger because consumers don’t have to spend billions on new pylons across the Welsh mountains.

The sheer number of GPUs planned for Prosperity Parc alone requires a baseload that nuclear power is well placed to provide. This symbiotic relationship, where the data centre pays for the nuclear plant's fixed costs, offers a potential model for future green energy generation.

Conclusion

Data centres pose an unprecedented challenge, adding huge, inelastic demand to electricity grids around the world, at a time when we are also trying to decarbonise electricity production and achieve Net Zero. For most countries, an extra data centre is bad news for climate. However, for the UK, it is far less clear. Indeed, if a British data centre replaces one that would otherwise have been built in Germany or the US (let alone the UAE or Saudi Arabia), the effect is likely to be net positive for fighting climate change.

Over the next few years, the UK will continue to decarbonise its grid, but new green technology depends on having a reliable source of demand. This is essential for covering the lion’s share of the cost of green energy – its impact on the grid and transmission. While demand from elsewhere is falling, data centres can make these projects more viable.

Humanity must adapt to and harness AI, while mitigating climate change. In Britain, at least, we can do both.

For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]