Table of Contents

- 1. Top lines

- 2. Introduction

- 3. Fixing Four Flaws

- 4. Conclusion

- 5. Authors

- 6. Appendices

Top lines

- Tax cliffs are lose-lose: individuals forgo additional income, the Exchequer forgoes tax revenue, and wider society suffers as a result. Conversely, fixing tax cliffs would be a win-win.

- Tax cliffs do not only affect the rich: while the £100,000 childcare cliff gets the most attention, carers also face a cliff edge around the £10,000 mark.

- Fixing tax cliffs pays for itself: even with conservative assumptions about behavioural responses, our modelling implies that replacing the £100,000 childcare cliff with a taper would raise £300m, enough to pay for removing the £10,000 carers’ cliff edge.

- Fixing tax-cliffs would be good politics, good economics and good for the Exchequer. The Government should:

- 1. Replace the childcare cliff edge with a 3% taper

- 2. Spread the Personal Allowance withdrawal over a wider range of income

- 3. Smooth the High Income Child Benefit Charge over £60,000-100,000

- 4. Replace the Carer’s Allowance cliff edge with a taper

Introduction

One of the first rules of taxation, so elementary it could even go unstated, is that a taxpayer should not be worse off from earning more. Yet for several years, the UK’s tax system has violated that principle, most notably for carers earning above around £10,000 and parents earning in excess of £100,000.

In between these cliff edges, poorly constructed tapers have created marginal tax rates well above 50% even for those far from the top of the salary scale. These anomalies violate all three of the fundamental principles in the Mirrlees Review, by failing to cohere with the benefits system, producing significant distortions in behaviour, and creating substantial inefficiencies.

There is a very broad consensus that this has to change. The question is how to remove these distortions, and particularly how to do so in a way that is revenue neutral for the Exchequer.

This paper focuses on four specific issues in personal taxation and takes each in turn:

- The £100,000 tax cliff edge for receipt of childcare subsidies

- The 62% marginal tax rate created by the clawback of the Personal Allowance

- The high marginal tax rates produced by the High Income Child Benefit Charge

- The tax cliff edge affecting recipients of Carer’s Allowance.

We recommend that the Government should:

- Replace the childcare cliff edge with a 3% surtax above £100,000 for each child in receipt of childcare subsidies

- Spread the Personal Allowance withdrawal over a wider income range

- Smooth the High Income Child Benefit Charge over £60,000-100,000

- Replace the Carer’s Allowance cliff edge with a taper

We built this tool to help policymakers and the public understand these four tax areas and how our proposed solutions address their underlying issues.

Fixing Four Flaws

1. Replace the Childcare Cliff Edge with a 3% Taper

The most distortive issues in personal taxation arise from the state’s attempts to claw back childcare subsidies from higher earners.

There are two subsidies of particular relevance here: Free Childcare for Working Parents (FCWP) and Tax-Free Childcare (TFC):

Free Childcare for Working Parents is the more generous of the two, ensuring that eligible working parents can receive 30 hours of paid childcare for children from 9 months until they start school at the age of 5.

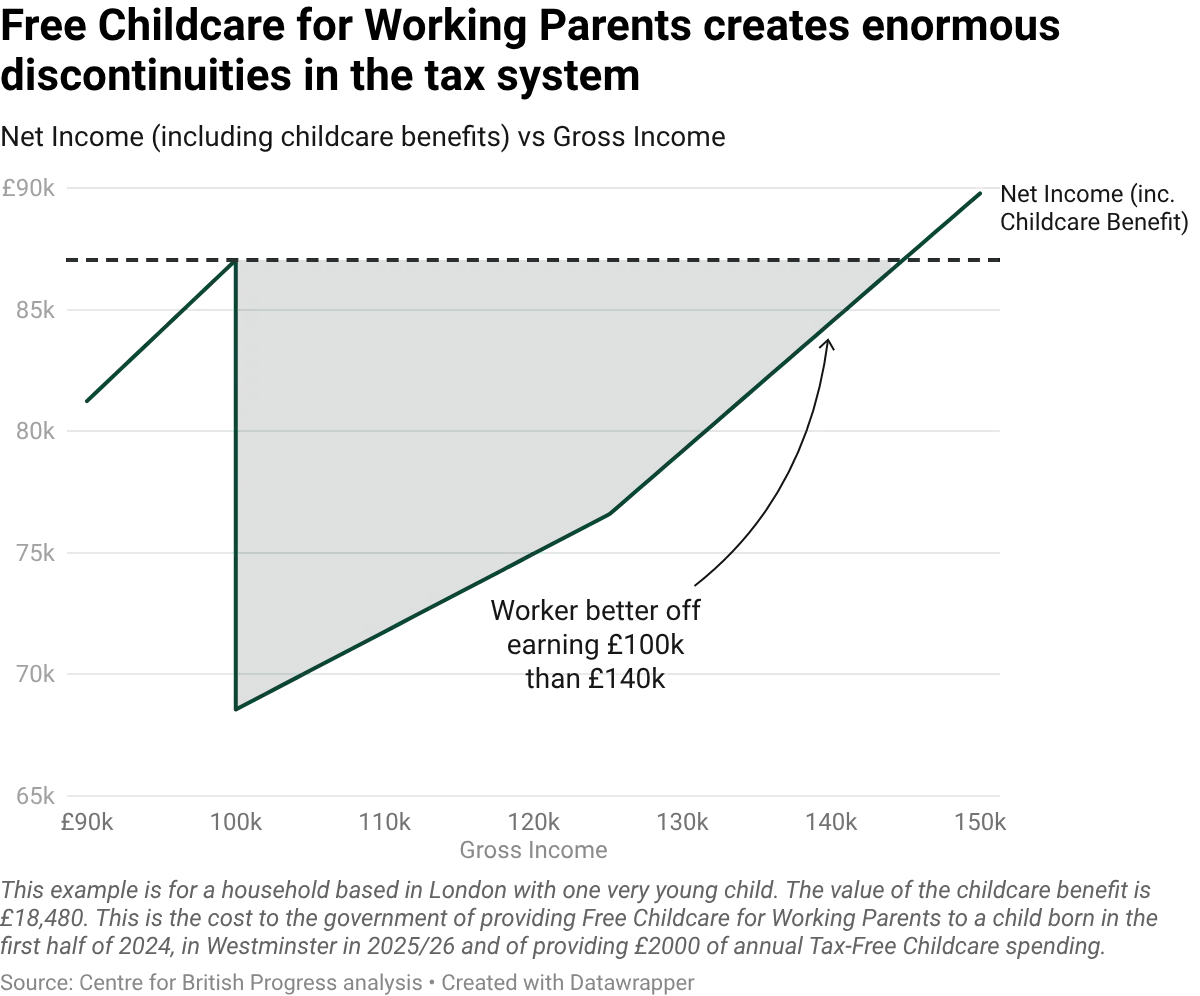

The value of the subsidy varies greatly with Local Authority, the age of the child and even their date of birth within the year. Theoretically, the largest possible cost of childcare hours this financial year would be for a child born in the first half of 2024 who is attending an early years provider in Westminster - this would amount to £16,480.

Tax-Free Childcare provides that the state will pay 20% towards childcare costs, up to a maximum of £2000 for £10,000 in expenses. The most significant usage is on nursery fees, where parents will often pay fees of several thousand pounds to supplement the FCWP entitlement and can use TFC to reduce this cost. However, unlike FCWP, TFC can be used for children up to the age of 11 on other expenses like after school clubs.

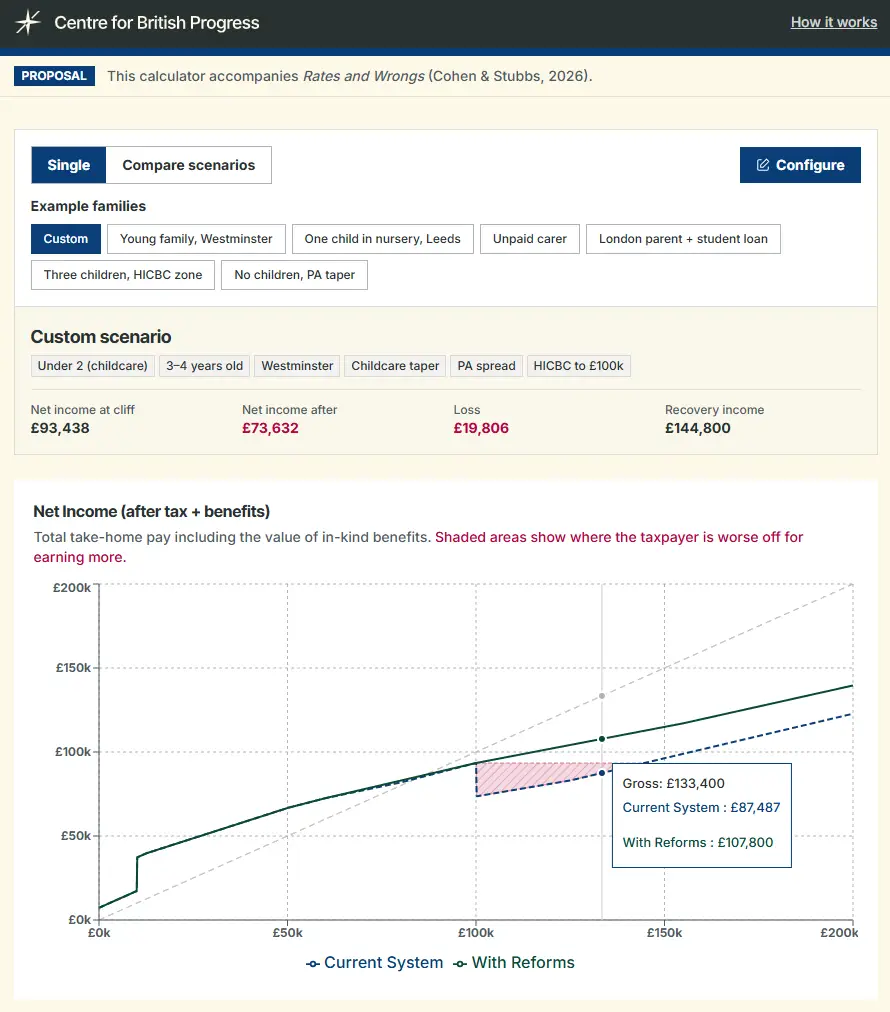

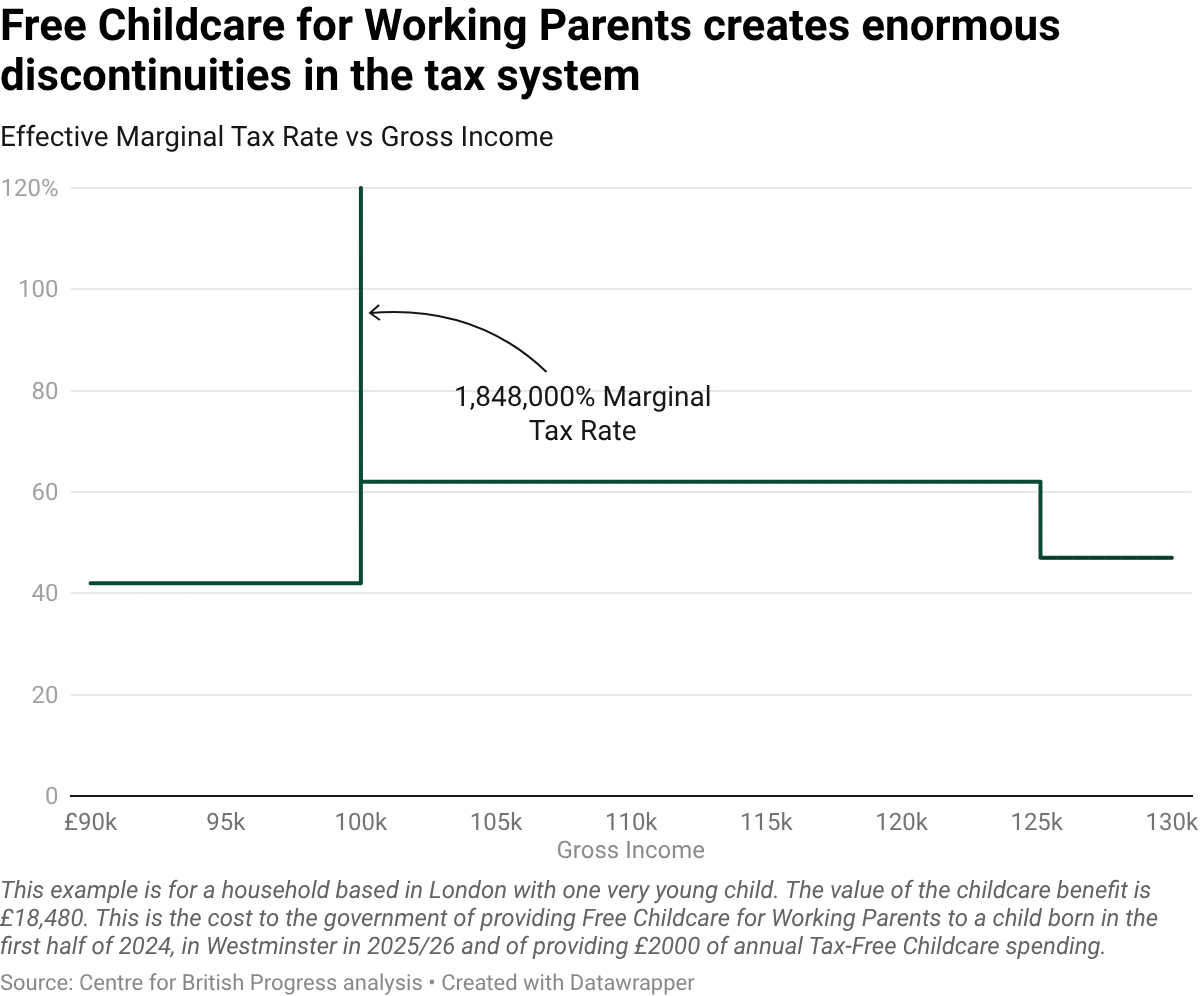

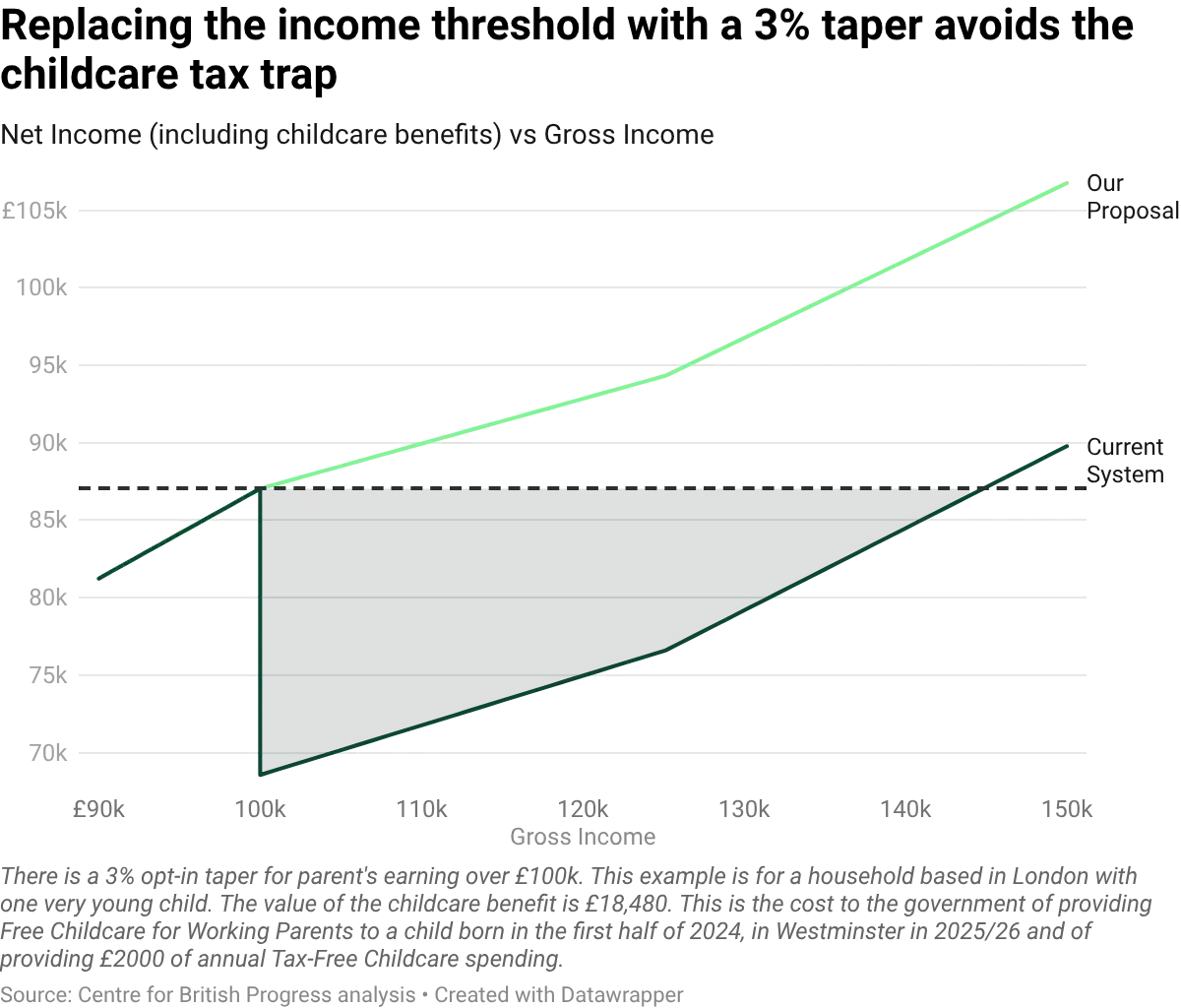

Both FCWP and TFC are withdrawn once one parent has an adjusted net income over £100,000. As the IFS noted, “The distortions that this can create are among the most severe you will ever see within a tax and benefit system.”

Returning to the theoretical example of a child in Westminster, if they were using their full TFC allowance and childcare hours, that highest earning parent would not be better off in cash terms until they earned £145k, if they were an employee.

The problems with the tax cliff edge only get worse if that parent has more than one child in nursery in a particular year.

Predictably, this has led to a large number of parents choosing to earn less than they could (for example by working part time) or channelling part of their salary towards their pension.

Punishing parents for working more is plainly a public policy failure, particularly for a government concerned about economic growth. There is as absolute a consensus on this subject as any in fiscal policy. The IFS described the £100,000 cliff edge as “Absolutely insane”. Major media outlets have reported extensively on the anomaly and its effects.

The fiscal cost of providing free childcare hours for children with a parent who earns over £100,000 is higher than for children with parents on lower incomes for two reasons.

- Higher earning parents have a greater monetary incentive to restart work earlier, thus necessitating higher utilisation of the childcare hours when their children are particularly young. This is especially costly as the hourly funding rates for under 2s and 2-year-olds are much higher than for older children.

- Higher earning parents tend to be concentrated in London and the South East, where funding rates are again higher - this time due to cost of living adjustments in the funding for early years providers.

This means that the government is disproportionately disincentivising high earning individuals from work in the most productive urban centres.

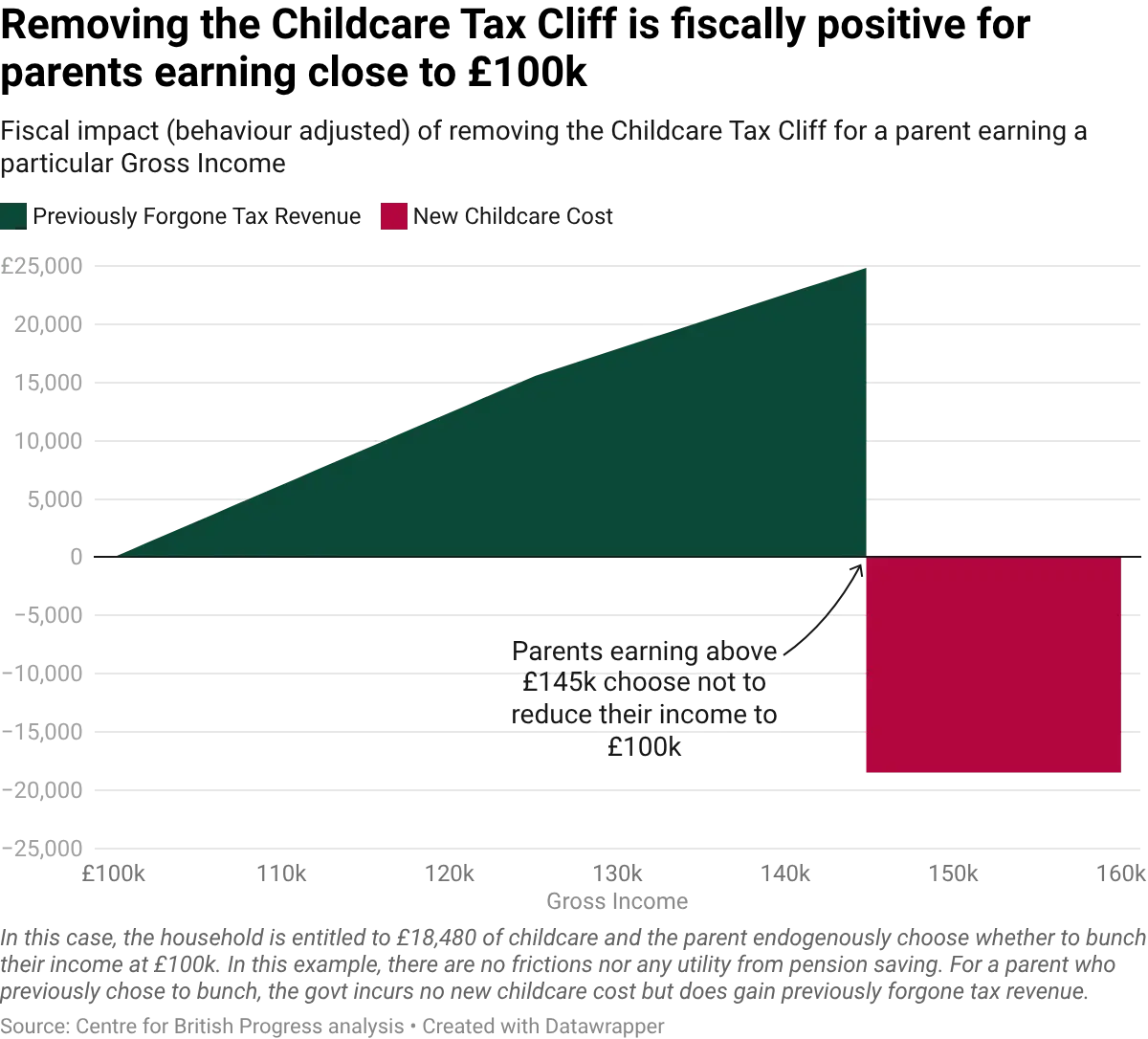

However, both of these factors only strengthen the magnitude of the behavioural response by workers. Modelling conducted for this paper implies that just removing this cliff edge at £100,000 in the tax system would raise far more in new tax revenue (lost through workers reducing their adjustable net income) than the cost of providing the free childcare hours. In a model where households change their labour hours, just removing the notch raises £425m in 2029/30.

Under a much more conservative model, where labour income is fixed and workers choose whether to divert money earned over £100,000 to salary sacrifice pensions, removing the cliff raises £130m in 2029/30. This fiscal effect remains positive throughout an extensive sensitivity analysis, which includes adding frictions for workers using salary sacrifice, different preferences over pension saving and using the very highest funding rates for childcare hours.

A Short Explanation of the Childcare Cliff Edge ModellingAn FOI response from November 2025 shows that HM Treasury does not hold any estimates on the tax revenue impact of parents reducing their adjustable net income below £100,000 in order to gain access to childcare subsidies. This is a crucial piece of evidence when evaluating the fiscal impact of the childcare tax cliff edge. On the basis of publicly available information, we have attempted to model this policy with behavioural effects. In our model, the primary response of households to the removal of the tax cliff edge is to reduce the amount of salary sacrifice they currently engage in to reduce their taxable income. This shifts taxation from the indefinite future, when these households receive their pension, into the present. That is likely to result in a net increase in average effective tax rates for these households because they will increase the amount of their income that is taxed at higher rates. We also model a positive labour supply effect from the removal of this disincentive, but the primary impact of the policy change is to reduce the amount of salary sacrifice households currently engage in for salaries above £100,000. How does it work? When a parent decides to drop their income from, for example, £120,000 to £100,000, the government loses £12,000 of Income Tax revenue whilst still having to pay for their childcare. Reversing the cliff would, for this household, not incur any additional government spending and would lead to a substantial increase in Income Tax revenue. In the long term, the government may gain Income Tax revenue when this additional pension saving is taxed, though probably at lower marginal rates. However, most parents of nursery-age children will be many decades away from retirement (the fiscal NPV here is ambiguous). Removing the cliff edge leads to more taxable income, increasing fiscal headroom against the Government’s fiscal targets. In our model, households endogenously choose whether to reduce their income to just under £100,000. They make this decision by maximising their net income (including the value of the childcare benefit) whilst having a current period utility for pension saving and a labour disutility. Frictions are also used to ensure that households are made at least £1,000 better off in terms of net income before they decide to bunch. |

The Taper

Although this modelling indicates that simply removing the childcare tax cliff edge would be fiscally positive, the Exchequer could raise more revenue by replacing the cliff edge with a taper, similar to the one that exists for Child Benefit (as detailed below).

However, the contrast with Child Benefit is illustrative. For those with incomes low enough to avoid the taper, Child Benefit is a uniform benefit (conditional on the number of children). This means that a family with, say, two children will receive precisely the same amount regardless of their circumstances. By contrast, the value of the childcare subsidies varies dramatically depending on the age of the child and the location of the early years provider. Calculating the exact cost of the entitlements to each parent of the FCWP scheme would be an extremely complex exercise.

We instead propose that anyone benefitting from childcare subsidies would pay a 3% income surtax on earnings above £100,000 for each child benefitting from childcare subsidies. We find that implementing this 3% taper raises £330m in 2029/30 using the more conservative, exogenous labour model. Under the less conservative model, it would raise £700m in 2029/30.

Fundamentally, this proposed system operates more like a self-administered taper. As illustrated in these examples, it would fall to individual taxpayers to opt in to paying the 3% surtax by benefitting from childcare subsidies. Although this calculation would introduce some complexity into the system, this problem is relatively small for two reasons. First, the threshold at which it would no longer be worthwhile to utilise childcare subsidies would be significantly higher than the current cut-off of £100,000. For example, if the annual childcare benefit was worth £5,000, parents earning up to £266,666 would still be better off from opting into free childcare hours. As a result, relatively few taxpayers would be in any doubt over whether it would make financial sense for them to apply for childcare subsidies.

Second, the decision of whether to apply for childcare subsidies would have far less significant implications for those in the immediate vicinity of the threshold. Currently, if an individual’s salary inadvertently exceeds £100,000 by a single pound, they immediately lose childcare subsidies worth thousands of pounds. This feature is removed under the new system. Take the case of the person with the £5,000 childcare subsidy. If that individual’s salary exceeded £266,666 by £1, although at that point they would be better off if they opted out of receiving childcare subsidies, the cost to them of remaining in the system would be negligible.

Fiscal Impact Forecast (2029/30):

Exogenous Labour Model | Endogenous Labour Model | |

|---|---|---|

Option 1: Remove Cliff Edge | +£130m | +£425m |

Option 2: Replace Cliff Edge With 3% Per-Child Surtax | +£330m | +£700m |

2. Spread the Personal Allowance Withdrawal Between £100k and £155k (Cost)

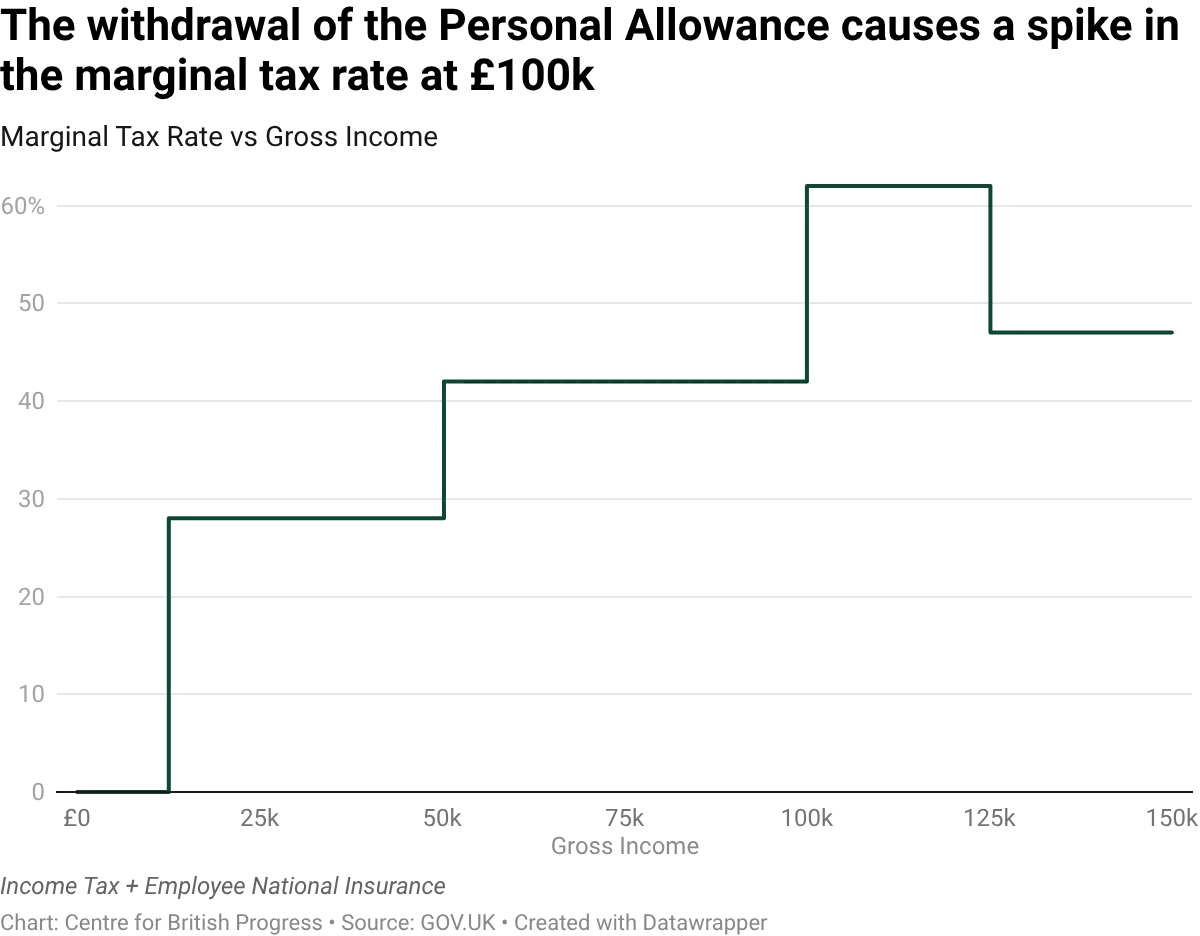

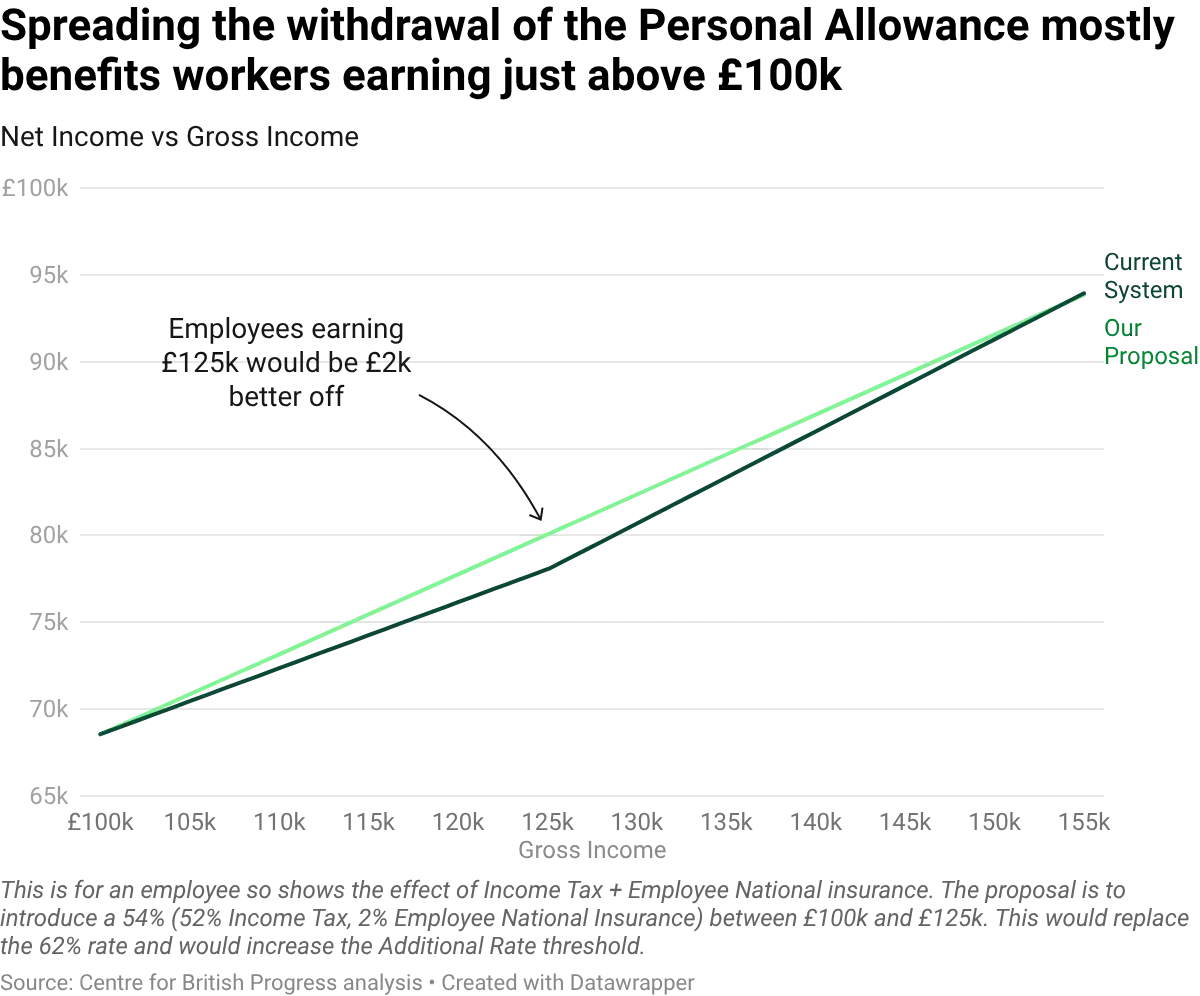

Once the £100,00 childcare cliff edge is removed, the situation is significantly improved for those earning above this threshold. However, it would remain the case that, separate from any interaction with the childcare system, employees earning between £100,000 and £125,140 pay an effective marginal tax rate of 62%. As the chart shows, this is far higher than the tax rate paid by those earning salaries above £125,140, a very irrational outcome of the current tax system.

This inconsistency is the result of a policy designed to reclaim the Personal Allowance from higher earners. To achieve this, taxpayers earning more than £100,000 lose £1 from their Personal Allowance for every additional £2 they earn. This adds an extra 20 percentage points to the 40% Higher Rate of Income Tax, leading to an effective marginal tax rate of 60% (62% with employee National Insurance) between £100,000 and £125,140.

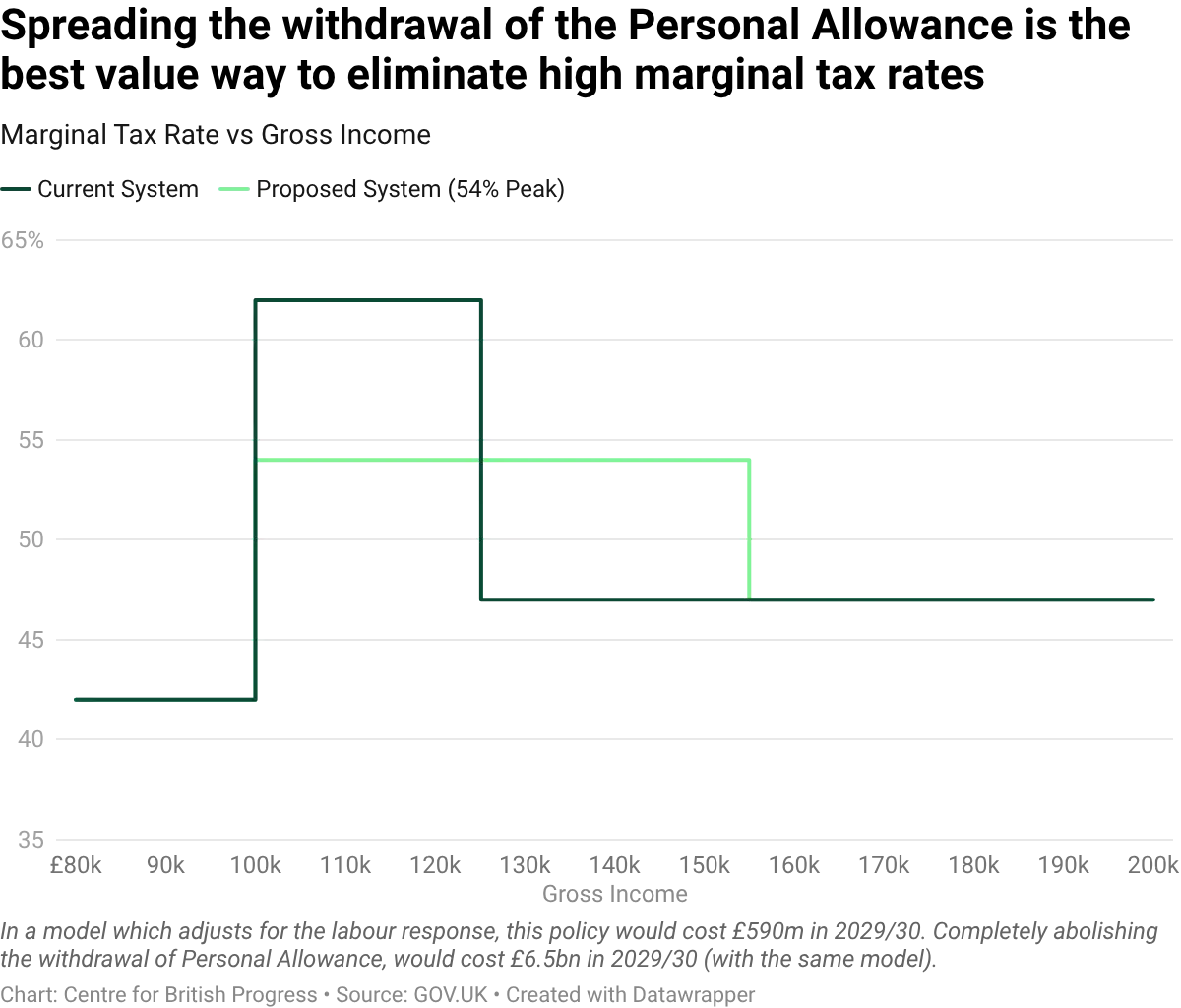

While the most straightforward solution would be to remove the clawback of the Personal Allowance, this would come at a cost of around £6.5bn in 2029/30. Simultaneously bringing down the threshold for the Additional Rate of Income Tax from £125,140 to £100,000 would offset this cost by only around £1.8bn. The main reason why both of these policies are so expensive is that they lead to transfers of either £5,028 or £3,771 to individuals earning above £125,140 without changing their marginal rate of tax. As a result, those very high earners have very little incentive to increase their labour hours nor to change their pension allocation. A more fiscally realistic alternative would be to spread the removal over a larger income range, thereby lowering the marginal tax rate.

There are many ways to do this, but the best way to think about it is to choose a maximum effective marginal tax rate and then raise the additional rate threshold so that people earning more than the threshold see no change in both their marginal rate of tax and their net income. We have outlined three variations of this policy with the estimated fiscal effects.

Fiscal Impact Forecast (2029/30):

Highest Effective Marginal Tax Rate (Income Tax + Employee National Insurance) | Endogenous Labour Model | |

|---|---|---|

Option 1: Spread to £155,000 | 54% | -£590m |

Option 2: Spread to £180,000 | 52% | -£940m |

Option 3: Spread to £230,000 | 50% | -£1.78bn |

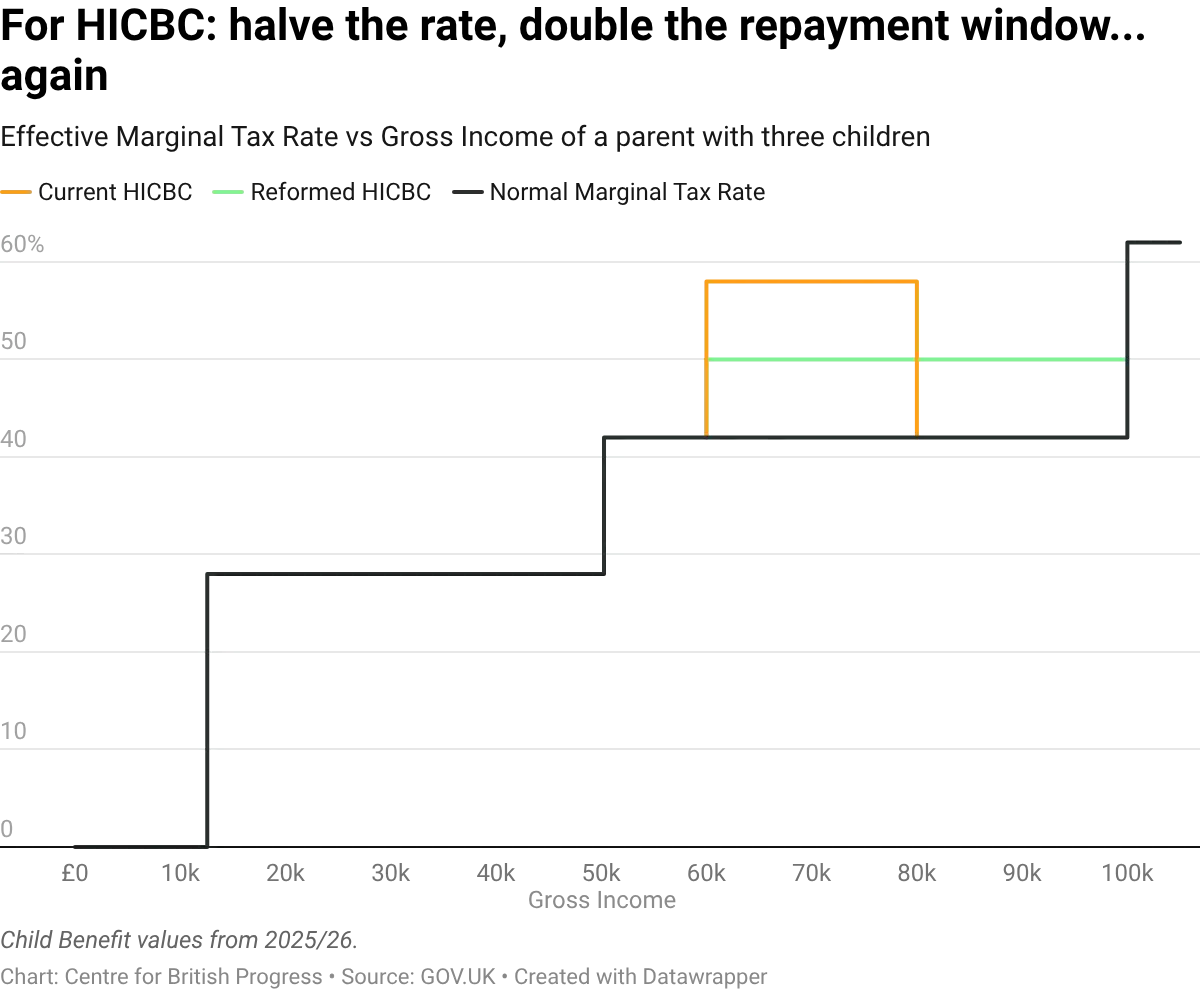

3. Smooth the High Income Child Benefit Charge Over £60k-£100k (Cost)

As one works their way down the income distribution, the next problem that arises affects a much larger group of taxpayers.

Here too, the issue stems from payments made by the state to parents. In this case, it is Child Benefit paid in the amounts of £26.05 per week for the eldest child and £17.25 per week for each additional child (equal to £2,251.60 and £3,148.60 per annum for a family with two and three children respectively).

In 2013, the Coalition government opted to means-test this benefit by introducing the High Income Child Benefit Charge (HICBC). This charge was established as a taper, with the full value of Child Benefit payments paid back between £50,000 and £60,000 on the salary scale. For taxpayers in this range, the result was an effective marginal tax rate of around 54%, 63% or 71% for a parent with one, two or three children respectively.

In the final budget of the Conservative government, then-Chancellor Jeremy Hunt moved the taper range to begin at £60,000 and end at £80,000. This reduced the effective marginal tax rates for a parent with one, two or three children to 49%, 53% and 58%. While this represented a significant improvement in the situation, these rates are still very high for taxpayers who are far from the top end of the salary scale. For those with four children or more, the marginal tax rate rises above 60%.

Number of Children | Annual Child Benefit | Current HICBC Effective Marginal Tax Rate | Reformed HICBC Effective Marginal Tax Rate |

|---|---|---|---|

1 | £1,354.60 | 48.8% | 45.4% |

2 | £2,251.60 | 53.3% | 47.6% |

3 | £3,148.60 | 57.7% | 49.9% |

The rates are unnecessarily high when one considers how easily the situation could be ameliorated. Just as the taper was extended to cover a range up to £80,000, the government could easily reduce these marginal rates further with minimal impact on revenue by extending the range to £100,000. This would halve the HICBC taper rate and lower the effective marginal tax rates for a parent of one, two or three children in this income range to approximately 45%, 47% and 49%, a pronounced improvement for this group and for the overall growth orientation of the UK tax system. This dramatic fall in marginal tax rates would only incur a cost of £124m in 2029/30.

Fiscal Impact Forecast (2029/30):

Spread HICBC repayment from £60k to £100k | -£124m |

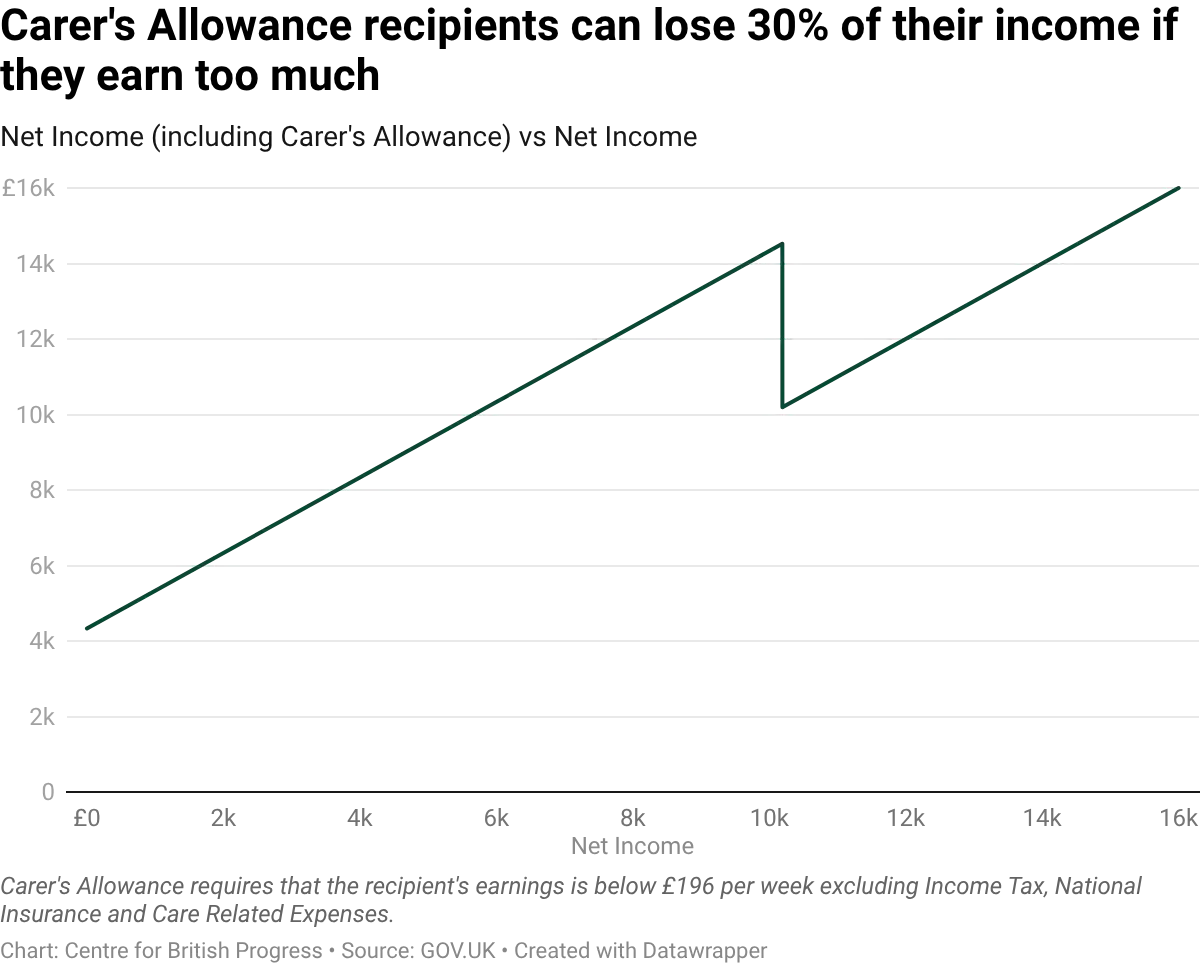

4. Replace the Carer’s Allowance Cliff Edge with a Taper

Although it receives far less attention than the other tax cliff edges discussed in this paper, arguably the most egregious of all the distortions in the UK tax system targets unpaid carers.

Those who provide at least 35 hours of care a week for a severely disabled person are entitled to a Carer’s Allowance of £83.30 per week (equivalent to £4,331.60 per annum). One of the conditions for receipt of this benefit is that the recipient is not “gainfully employed”, defined as having earnings of more than £196 a week (equivalent to around £10,192 per annum). The Carer’s Allowance is withdrawn in its entirety once one exceeds this level, creating a painful tax cliff edge.

We have already demonstrated the stark disincentive this kind of cliff edge presents to people considering taking on additional employment. However, this predicament is much less defensible when those affected are people on very low incomes taking care of severely disabled people.

The Sayce Review into Carer’s Allowance overpayment identified horrific stories of people trying to navigate this cliff edge. For example, one claimant had her weekly pay rise due to increases in the National Living Wage. As a result, her weekly earnings were 15p above the Carer’s Allowance earnings limit. DWP did not identify the overpayment for many months after the change and overpaid the benefit by £2,000, an amount they then sought to reclaim. The claimant earned a total of £5 more than the threshold in that time.

The most intuitive solution to this problem is to replace the Carer’s Allowance cliff edge with a taper. For example, a taper rate of 55% above the Carer’s Allowance threshold would have a static cost of just £101m in 2029/30, while a taper rate of 25% would incur a static cost of £277m.

Replacing the Carer’s Allowance cliff edge with a taper has been suggested many times previously. Back in 2008, the Work and Pensions Committee (WPC) called on the Department for Work and Pensions (DWP) to consider introducing a taper. The government dismissed that suggestion on the grounds that it would make the benefit more complex for the government to administer and for carers to understand. This back and forth was repeated in 2018 when the WPC again recommended introducing a taper, only for the government to object once more that this would complicate the system.

Frank Field, then head of the WPC, called the DWP’s bluff by asking whether the department had costed the changes that would be required, forcing the DWP to admit that it had not done so. This made a mockery of the notion that the government had undertaken any serious assessment of how complicated it would really be to make this change. It was also audacious to argue against a taper by citing carers’ interests, as if the additional complexity would not be a price well worth paying from their perspective for an end to the punitive cliff edge.

Fiscal Impact Forecast (2029/30):

Highest Effective Marginal Tax Rate (Income Tax + Employee National Insurance) | Static Cost | |

|---|---|---|

Option 1: Replace Cliff Edge with 55% Taper Rate | 83% | -£101m |

Option 2: Replace Cliff Edge with 25% Taper Rate | 53% | -£277m |

Conclusion

There is broad political agreement on the need for tax reform. That consensus, however, needs to be translated into specific proposals which are both practicable and politically palatable. This paper provides exactly those types of policy proposals. Even on the intentionally conservative sums provided here, the replacement of the £100,000 cliff edge (with a 3% per child surtax) could be paired with replacement of the care’s allowance cliff edge (with a taper) without imposing any additional cost on the Exchequer. This would make the tax system significantly more rational and efficient, potentially encouraging tens of thousands of workers to take on more employment.

Once one makes a fuller account of behavioural responses, replacing the £100,000 cliff edge with a 3% per child surtax would raise an estimated £700m. This almost covers the cost of replacing the Carer’s Allowance cliff edge with a taper, spreading the HICBC taper up to £100,000, and reducing the marginal rate above £100,000 from 62% to 54%.

Appendices

For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]