Table of Contents

- 1. Summary

- 2. Background

- 3. Why focus on electricity?

- 4. Package 1 - moving legacy costs onto general taxation

- 5. Package 2 - More reform in future

- 6. Conclusion

- 7. Authors

Summary

The government should take action and move more policy costs into general taxation. But the quid pro quo is no more contractual abominations that bind our hands in future.

Events in Iran have led to another spike in energy prices, just four years after the Russian invasion of Ukraine. Our paper argues for a bill relief package that is more than a sticking plaster solution.

It has two major components. Firstly, a £4bn p.a. package to move levies and taxes on electricity into general taxation. This will cut the cost of electricity relative to fossil fuels, catalysing the government's electrification ambitions and building long term energy security.

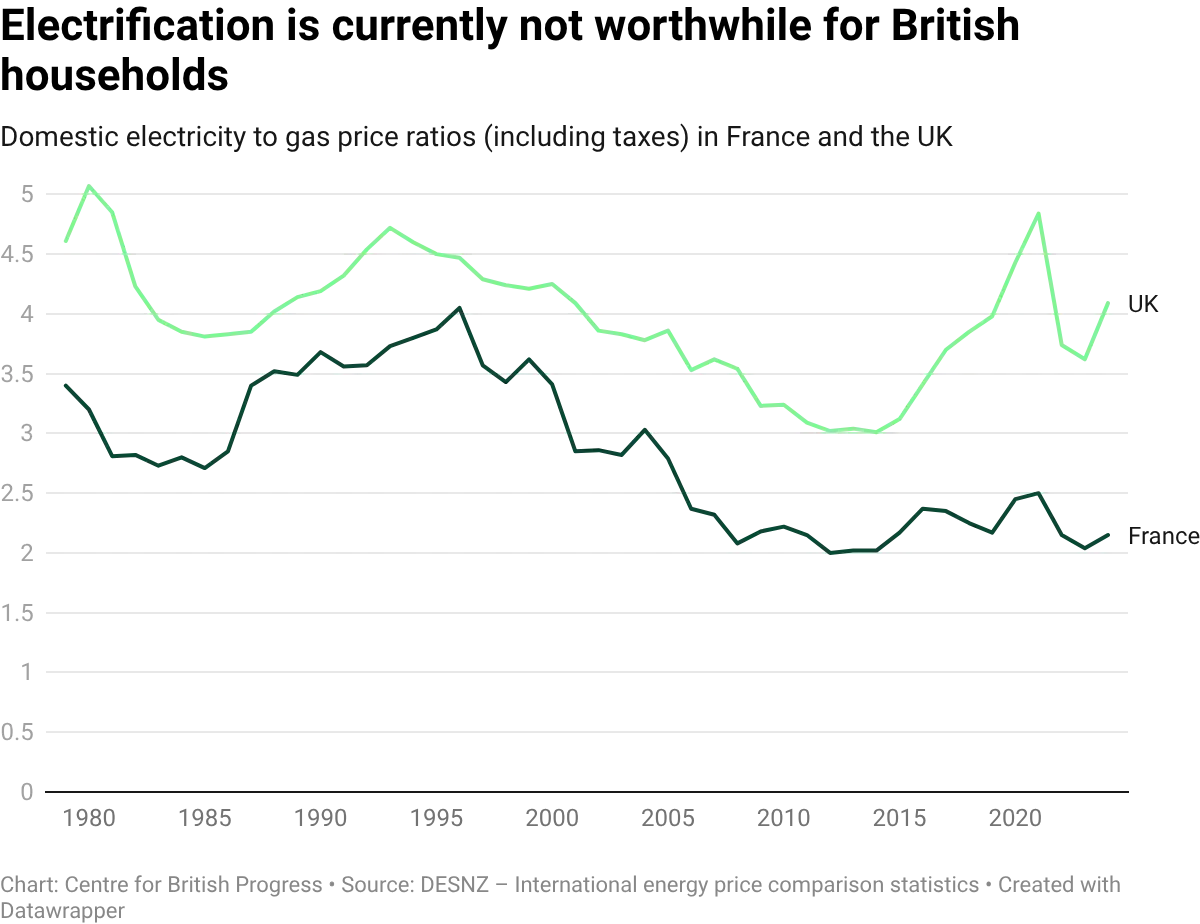

We estimate that these measures will cut average household electricity bills by c. £115 per year and reduce costs by 7% for everyday businesses. The household bill reduction would reduce the electricity to gas unit price ratio from 3.6 to around 3.1, materially improving the returns for domestic electrification.

The second part is the quid pro quo - in exchange for taxpayer support on levies now, we need much greater cost discipline and much more competition when procuring future generation and grid capacity. Our flabby electricity system, enriched by subsidy and rent-seeking, needs a much leaner diet.

Specifically, we propose:

- Moving three household electricity levies into general taxation: The remaining Renewable Obligation, the Feed-in-Tariff and the electricity costs of the Warm Home Discount.

- Cutting wider electricity costs by removing electricity generators from the UK Emissions Trading Scheme for five years and zero-rating the Climate Change Levy with respect to electricity on a permanent basis.

- Imposing cost discipline on new Contracts for Difference - via stricter price limits, technology neutral allocation rounds and subsidy clawbacks on exported electricity volumes.

- Further cost discipline by subjecting hydrogen to a carbon abatement cost limit, increasing consumer choice in the decarbonisation of heating and improving the efficiency of the grid via dynamic line rating.

Our package of reforms meets three important criteria:

- Immediate energy bill relief for both households and businesses

- Longer term energy security, by encouraging electrification

- Fiscally responsible by moving levies to the taxpayer that will fade over time - avoiding a permanent fiscal burden

The government has already made strides to reduce electricity costs for households and businesses, both in the November 2025 Budget and in setting up the British Industrial Competitiveness Scheme.

Now is the time to double down, and support electrification as the route to growth, decarbonisation and national energy security.

Background

There are three major areas of energy spending for households. Transportation, heating and electricity. Since the war in Iran, costs have risen for each.

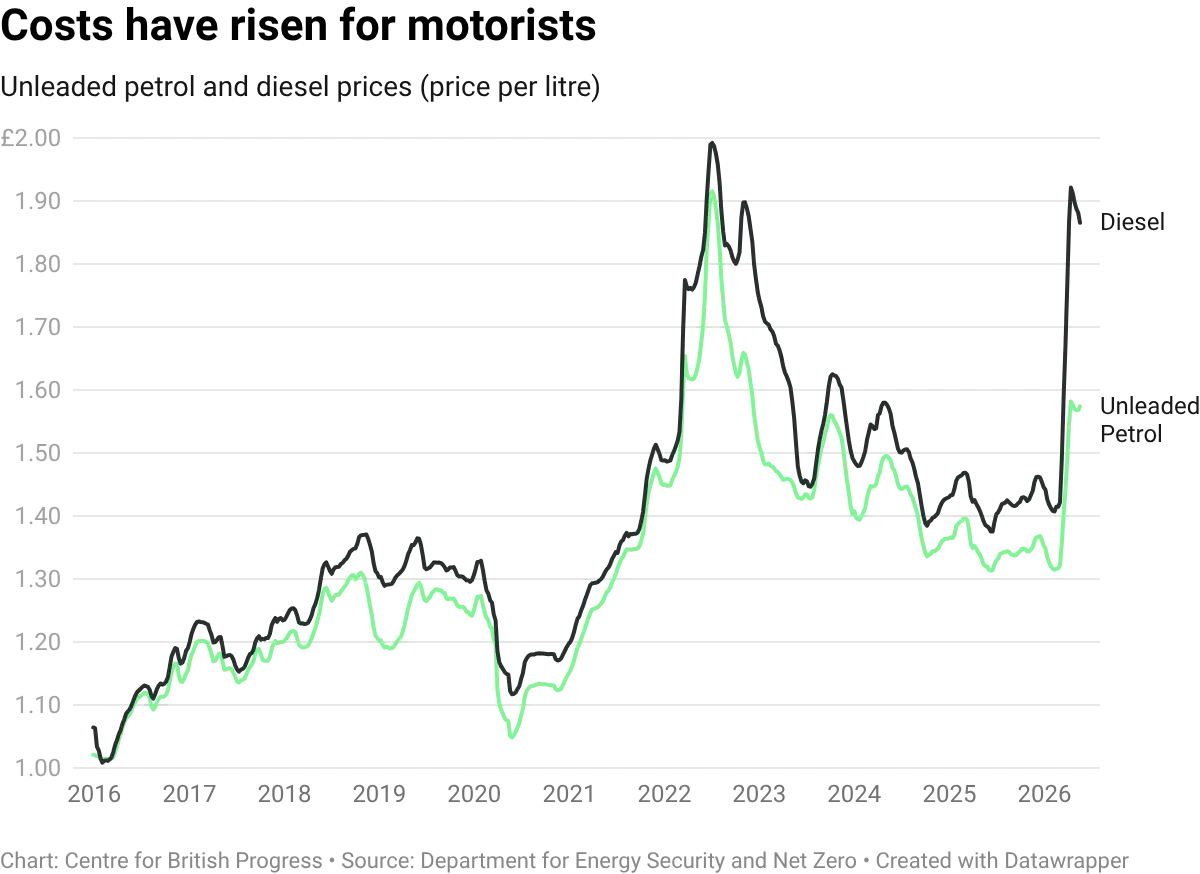

Road Transportation:

By the middle of May, petrol prices had risen by about 25 pence per litre versus the average for January and February 2026. The jump in diesel prices has been more extreme, around 45 pence per litre.

The rise can be attributed to higher crude oil prices, but also due to higher refinery margins. Global refining capacity has been squeezed, as refineries in Asia are suffering from reduced feedstock deliveries from the Middle East.

Assuming average private and commuting mileage of 6,700 miles per car, 1.2 cars per household, and 38 miles per gallon, each penny on the fuel price should increase household costs by about £9.60 p.a.

Petrol car households are thus facing costs increases of around £240 and diesel drivers around £430 p.a. Adjusting for the relative weights in the UK fleet, this averages out to around £305 p.a. for a non-EV household.

At the end of 2025, battery electric vehicles and plug-in hybrids made up about 7.5% of the UK car stock. Owners of these vehicles will be far less exposed to cost increases.

Domestic Heating:

Around 80% of homes in England and Wales use gas for central heating.

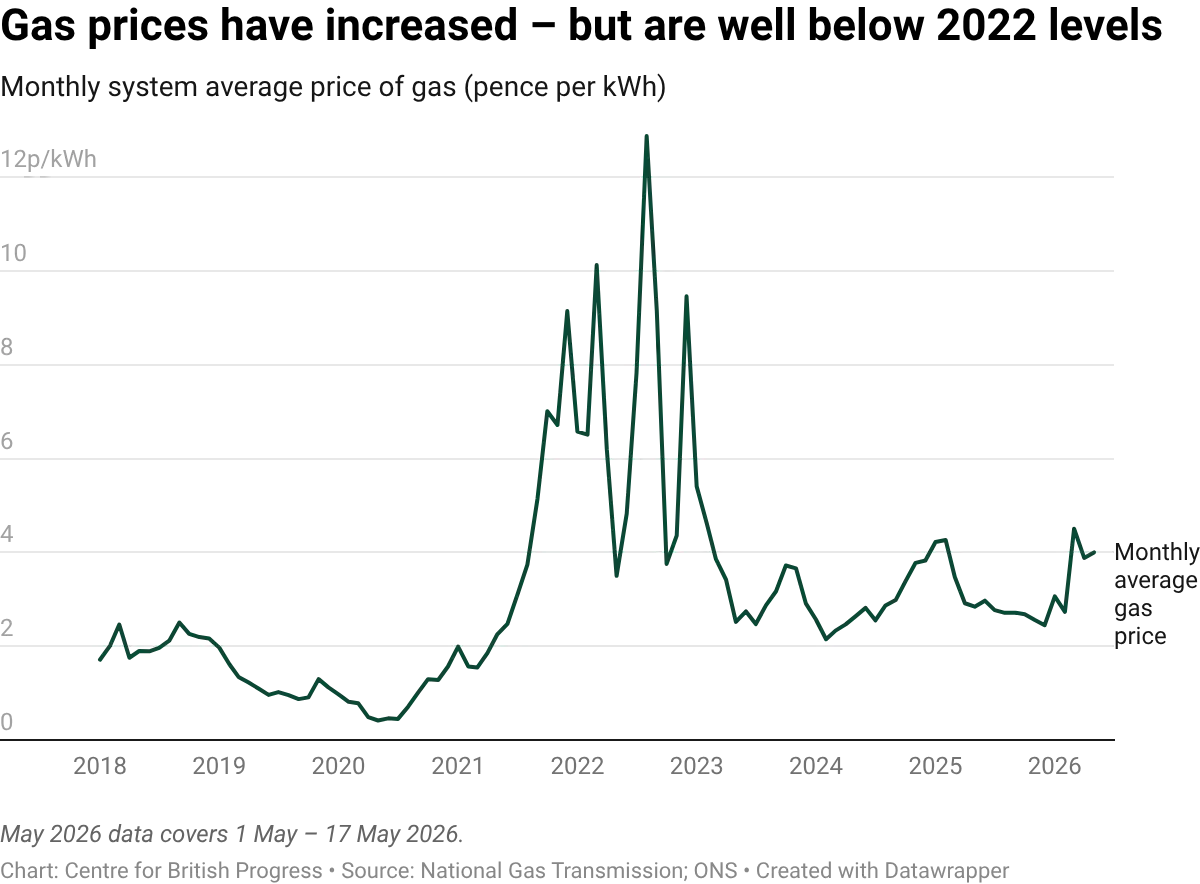

Wholesale gas prices since March have increased by about 45% vs the levels of January and February. Rising wholesale prices have increased gas heating costs in the latest price cap by about £180 on an annualised basis.

Around 5% of UK households use heating oil as their main fuel source. Exposure in Northern Ireland is higher, where almost two thirds of households are reliant on heating oil. Around 8% of UK households are reliant on electricity, which is skewed towards inefficient resistive heating, rather than much more efficient heat pumps.

Electricity:

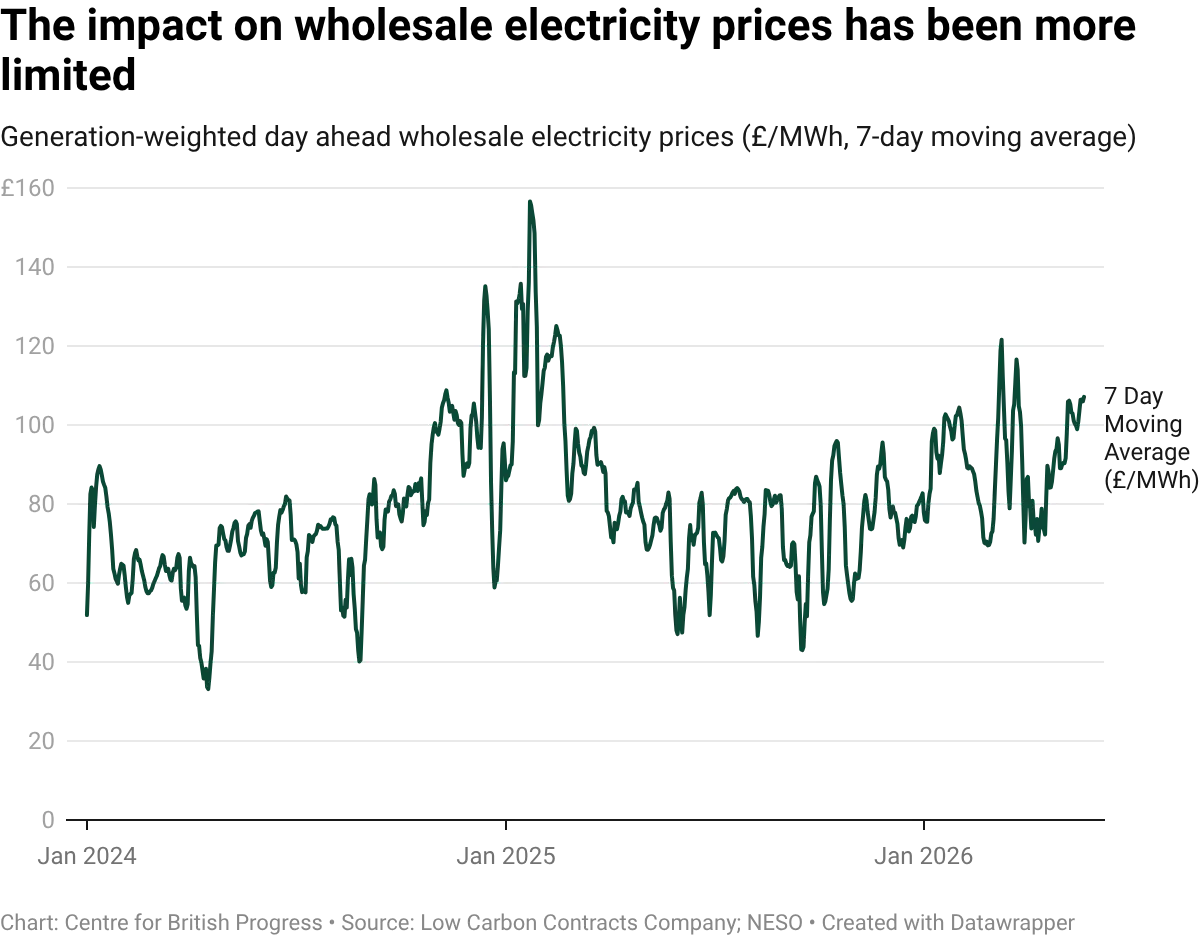

Day ahead wholesale electricity prices did not increase meaningfully in March 2026 vs. January to February - thanks to a month of strong wind and solar generation.

However, forward contracts for the next 12 months have increased by about £24/MWh since the end of February. Electricity prices have increased by about £40 on an annualised basis in the most recent price cap update (announced on the 27th May 2026)

In total:

Energy Service | Annual Cost Impact |

Motor Fuel (Non-EV driver) | £305 p.a. |

Gas Heating | £180 p.a. |

Electricity | £40 p.a. |

Cost increases were passed through to motorists almost immediately. Around 40% of gas and electricity customers are on some form of fixed price tariff.

£525 p.a. of total direct energy cost increases would represent around a 3.9% hit to discretionary household incomes, based on the Asda Income Tracker for February 2026.

Households have also experienced inflation in other goods and services - as the increased costs for businesses feed through to the wider economy.

Why focus on electricity?

Although electricity bills are likely to be least affected by the recent energy price shock, we argue that they should be the main focus for cost reduction measures.

1. Support across the board

Virtually all UK households are connected to the electricity network. Actions that reduce electricity costs will benefit a broad range of businesses and households.

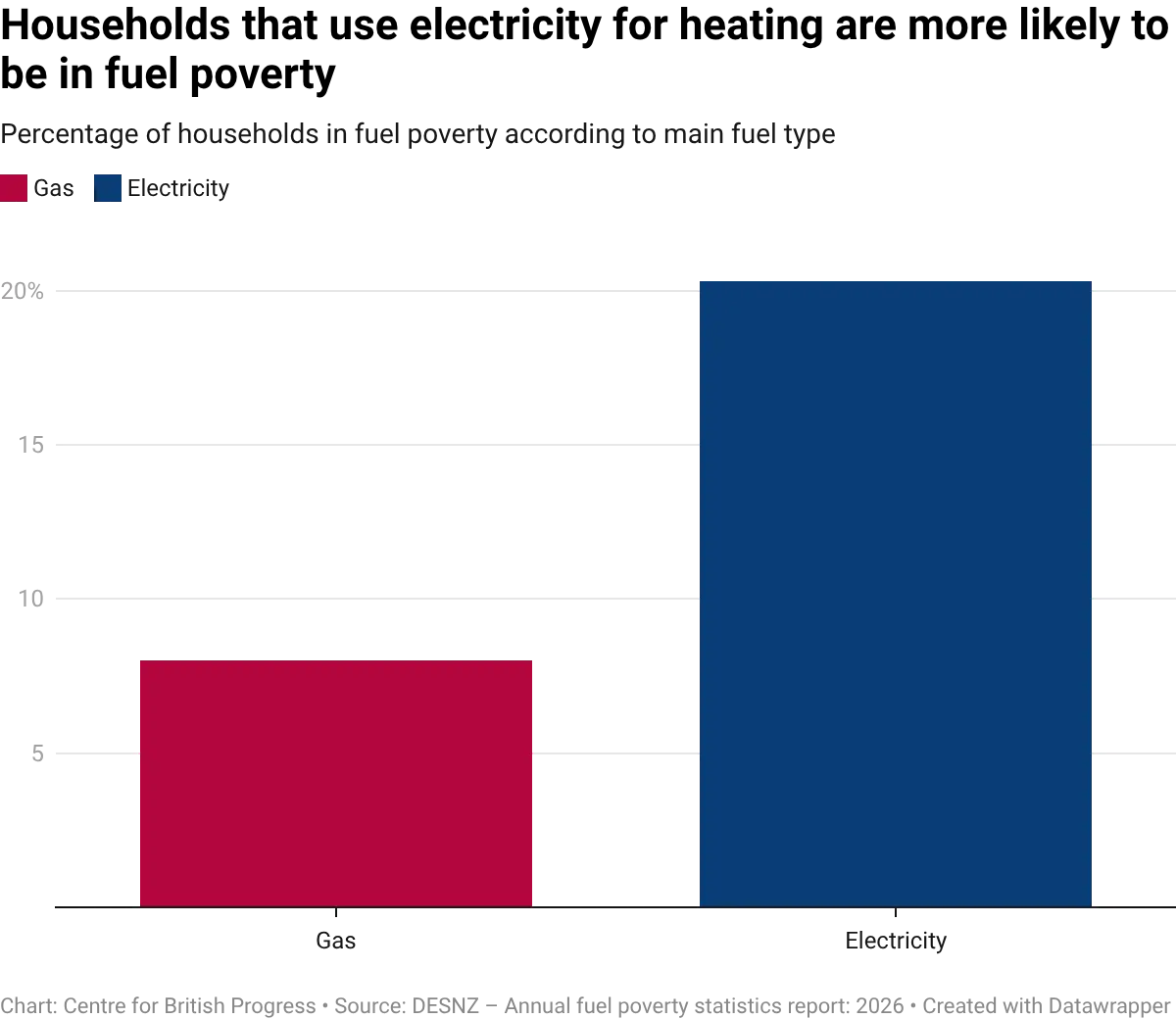

Reducing electricity costs would also help the c. 8% of households that rely on electricity as their sole source of heating. Households with inefficient resistive electric heating are c. 2.5x more likely to be in fuel poverty than gas heated households.

2. Encouraging decarbonisation

In 2024, the UK had the most expensive industrial electricity costs and second highest domestic electricity costs compared to a group of around 25 developed market countries.

As policy costs have been loaded on to electricity bills, we have stacked the deck against incredibly energy efficient technologies such as heat pumps and electric vehicles.

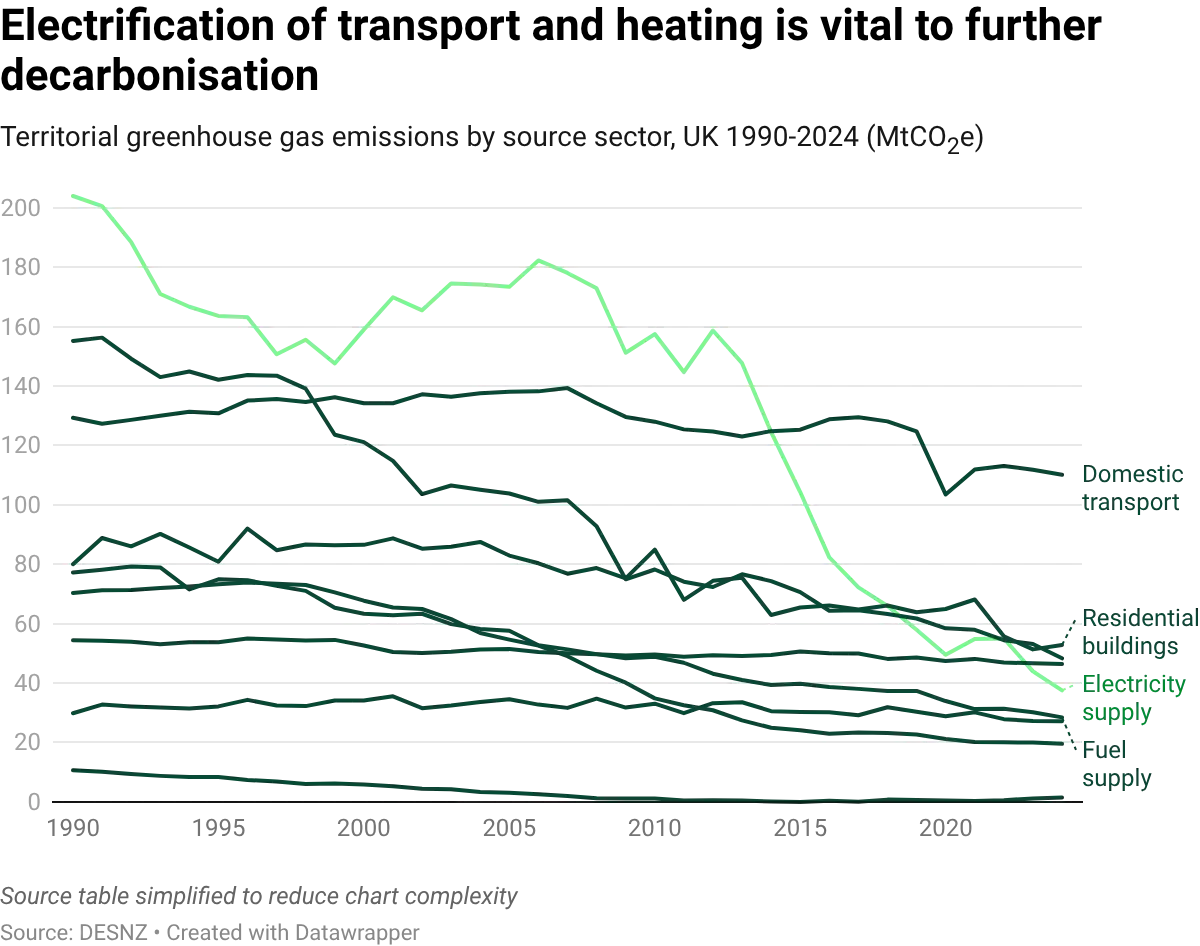

The UK has an increasingly clean grid, but is a laggard on electrification – i.e. the extent to which households and businesses are using electricity instead of fossil fuel options. Most notably, we are behind on using electricity for household heating. The key barrier is the relative price of electricity to gas. By cutting electricity costs we can make progress on our decarbonisation goals.

3. Long term energy security

The UK can generate electricity at home, through nuclear power and renewables, without relying on fossil fuel imports. Electrification is therefore essential for British energy security.

Whilst nuclear plants require uranium imports, fuel is a minor part of the cost base, and the UK already has a substantial presence in the capital-intensive enrichment process, thanks to the Urenco site in Capenhurst, Cheshire. Nuclear fuel is also incredibly energy dense, so it is feasible to hold years of fuel supply domestically. The same is not true for oil and gas.

Whilst renewables technologies such as wind and solar have high reliance on overseas supply chains in their construction, once they are built the UK has a domestic capital stock that can generate electricity without any requirement for imported fuel.

Importantly, both renewables and nuclear are highly capital intensive - meaning they can be built under contract structures that allow electricity to be secured at stable real prices - via Contracts for Difference and Regulated Asset Base models.

If we can reduce electricity costs, then consumers can benefit from lower prices and much greater bill predictability into the future.

4. Consumption must increase

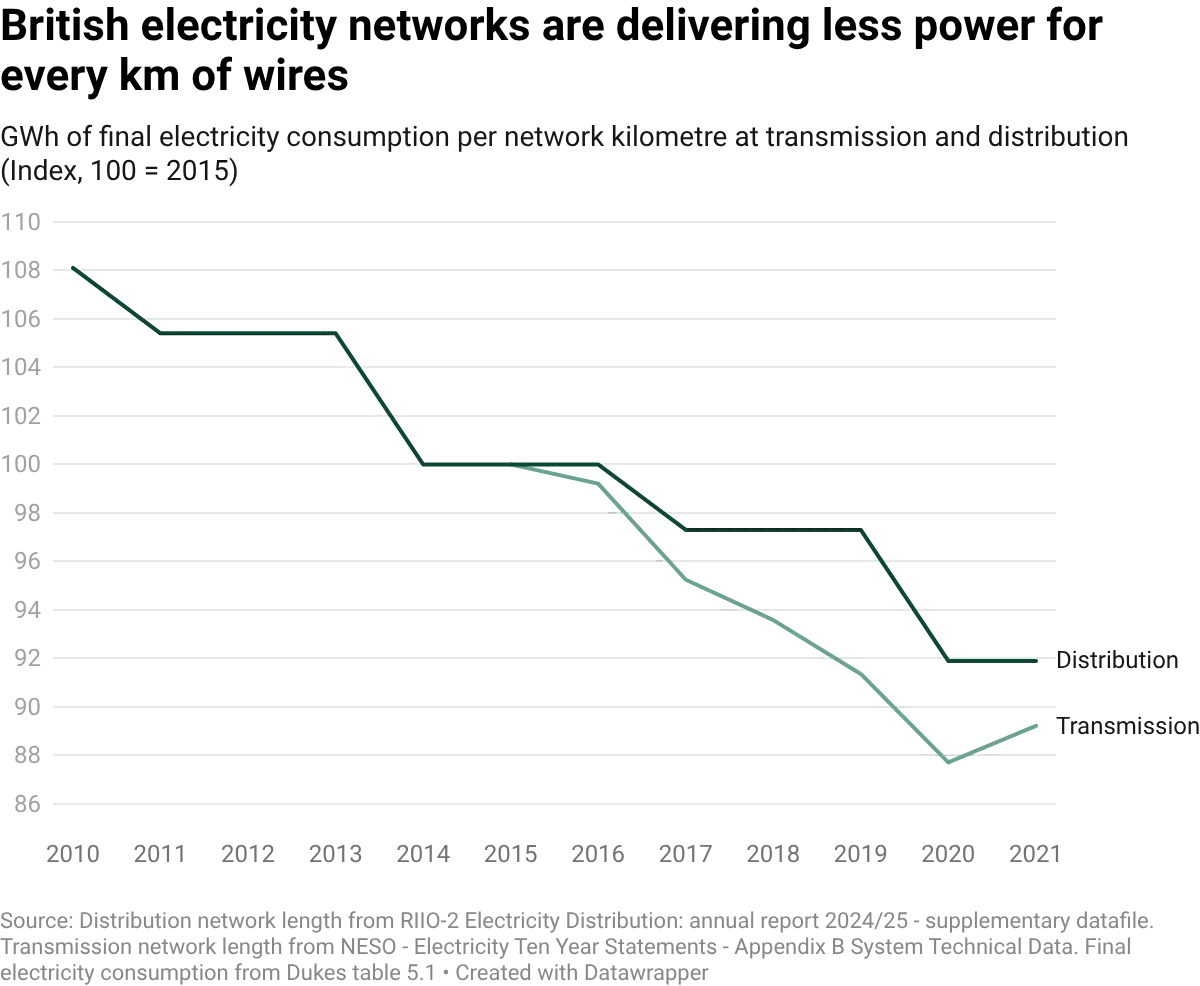

UK electricity consumption has fallen by 22% since the peak of 2005, and by 10% in the last decade. With rising fixed costs - via network investment, legacy contracts and the Sizewell C RAB, it is vital that consumption can grow to spread the cost burden.

Since 2010, the length of the distribution network has grown by 0.2% p.a. whilst electricity consumption has fallen by 1.3% p.a. - delivering a 1.6% annualised decline in electricity consumption per network kilometre.

Our data for the length of the transmission network (excluding offshore wind cables) only goes back to 2015, but tells a similar story. The network has grown by 0.7% p.a and consumption has fallen by 1.2% p.a. - driving a 1.9% p.a. decline in electricity consumption per network kilometre.

If electrification is to succeed, it is vital that consumption grows at least in line with the capital we are deploying into our infrastructure. The costs of our electricity networks are largely fixed - and are expected to make up around 25% of our bills by 2030. If consumption volumes fall short, network costs still have to be paid for, but are shared over fewer units. This means higher electricity prices, stalling our efforts to improve energy security and reduce emissions.

Package 1 - moving legacy costs onto general taxation

1. Addressing the generous contracts of the past - moving (remaining) RO and FIT costs from household bills to general taxation

Over the last twenty years, more and more of UK generation capacity has been constructed and financed via fixed price mechanisms, rather than relying on the wholesale market revenues. Some of these contracts have been negotiated at reasonable rates, but many earlier schemes were not.

Whilst early investment may have been necessary to help technologies scale, these legacy policy costs now act as a drag on household affordability and electrification. In last year's solar auction, new projects were awarded at just under £70/MWh at current prices. We highlight a number of instances where incumbent generators continue to receive over £200/MWh, thanks to legacy contracts and deals that have not expired.

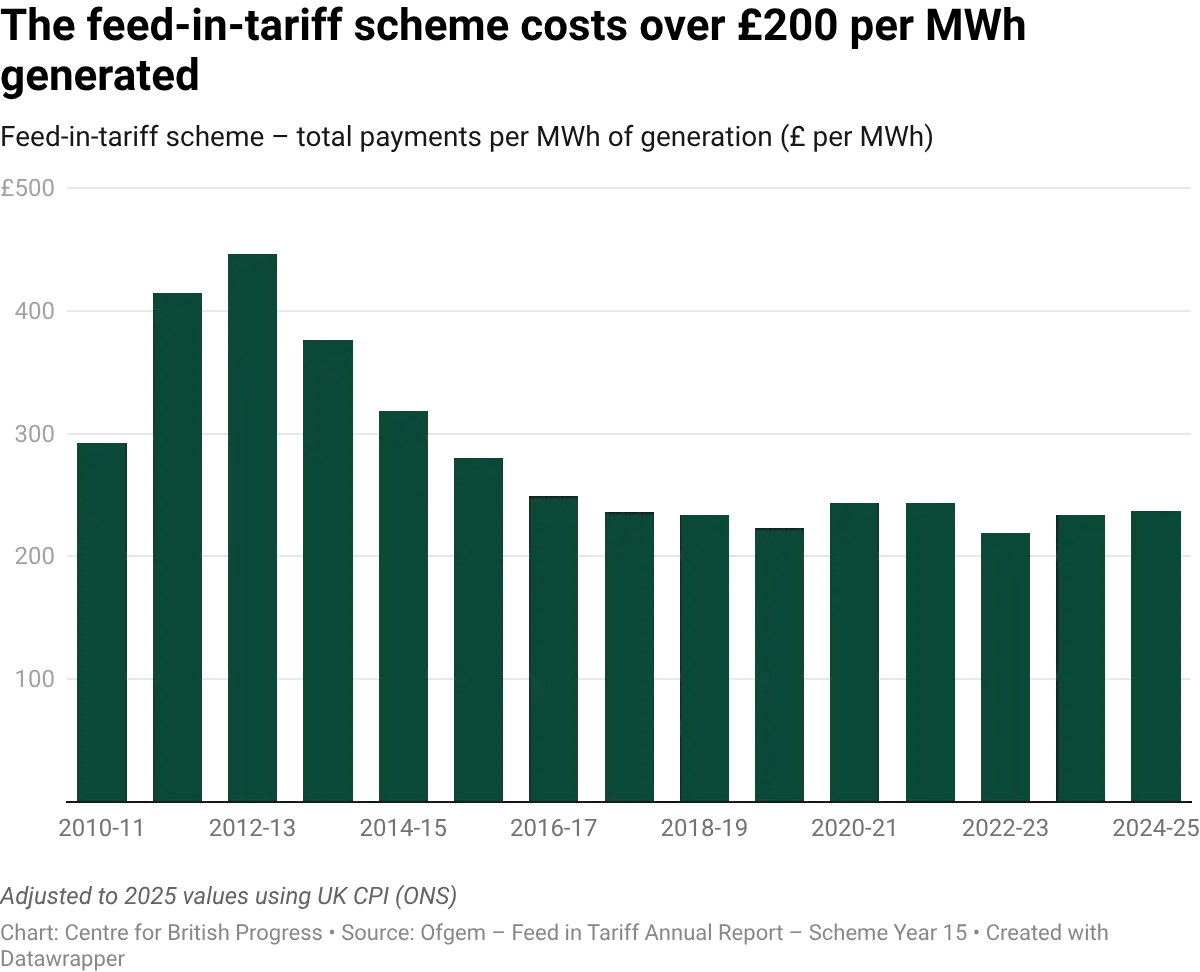

- Generous feed-in-tariffs led to a boom in rooftop solar from 2010 to 2019. In the year ending April 2025, generators in the scheme were paid c. £230/MWh on average, at an overall scheme cost of c. £1.8bn. Tariff rates were incredibly generous in the early years of the scheme, with reduced rates over time.

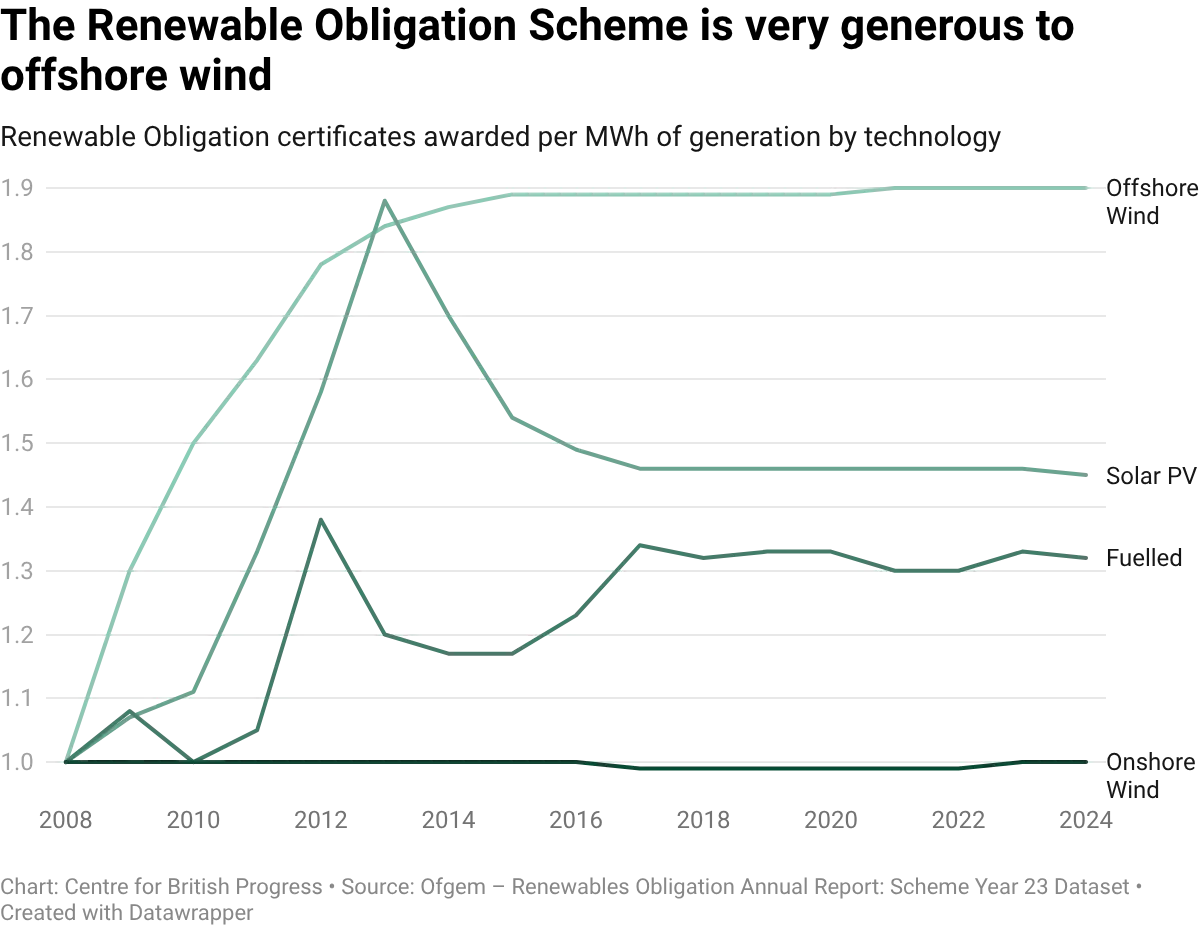

- The Renewable Obligation (RO) scheme started in 2002 and was originally designed to award generators a single RO certificate (Currently worth £69.34 each) per MWh generated, in addition to the wholesale value of their electricity. In 2009, banding was introduced to the scheme, varying the number of certificates awarded depending on the technology. Offshore wind has been particularly generously rewarded, receiving 1.9 RO certificates on average per MWh generated - this equates to over £130 per MWh, in addition to wholesale revenues.

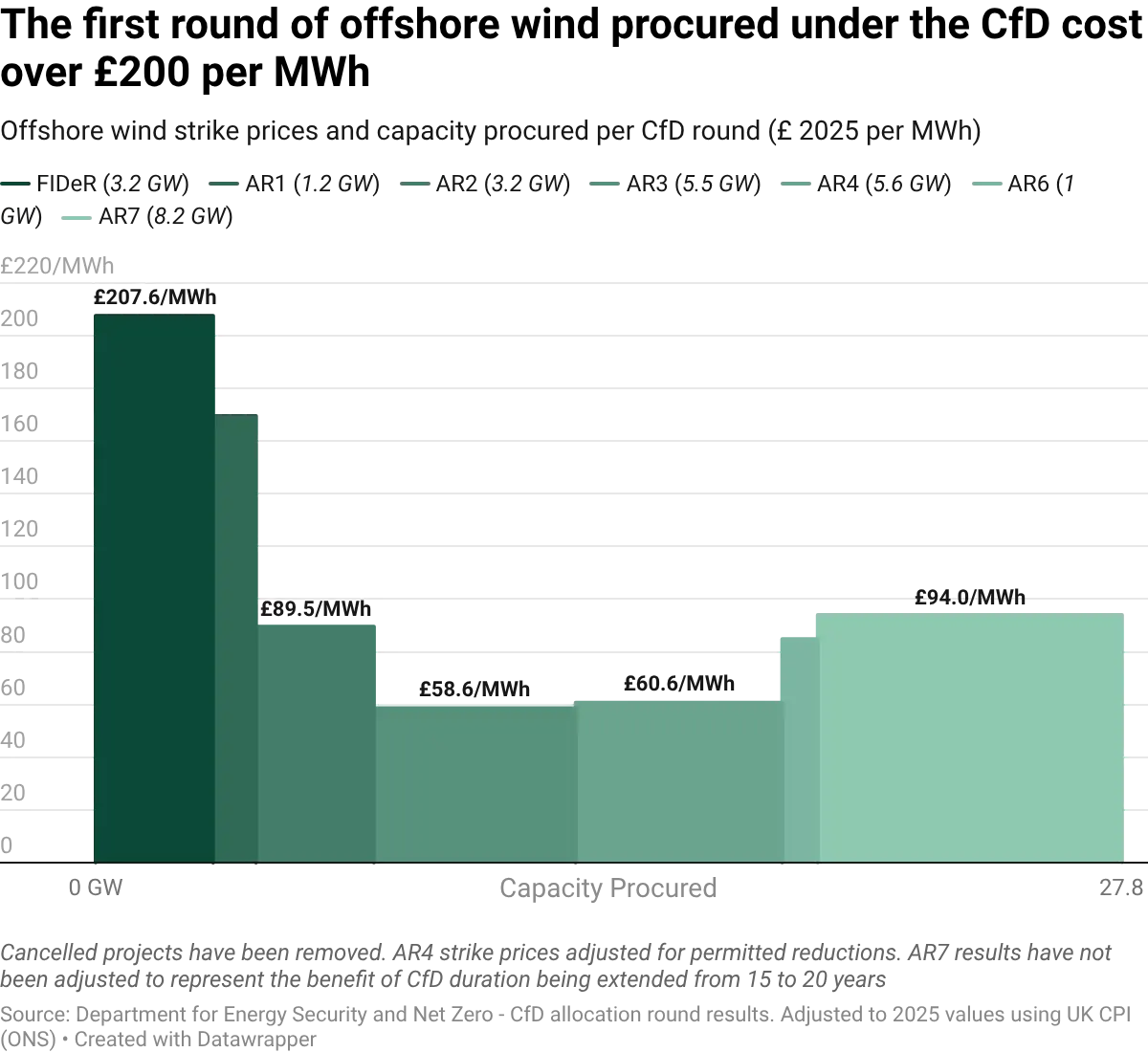

- The very first Contracts for Difference were procured without competitive tension - a decision criticised by the National Audit Office. In total, five offshore wind farms, two biomass conversions and one dedicated biomass plant were awarded contracts. On a capacity weighted basis, these projects are currently receiving in excess of £195/MWh, with the offshore wind generators receiving over £210/MWh at today's prices.

The feed-in-tariff scheme, alongside offshore wind farms supported by Renewable Obligations and the first Contract for Difference round amounted to c. 15% of British electricity generation in 2024.

If the government isn’t prepared to renegotiate these schemes (and risk damaging future investment) then it should move more of these legacy costs into general taxation. The government took action to this effect in the November 2025 budget, where 75% of the household costs of the Renewable Obligation scheme were moved into the tax system.

We estimate that removing the remaining 25% of the RO scheme and all of the feed-in tariff scheme costs from household bills would reduce domestic electricity bills by c. £53 p.a. at a cost of c. £1.5 bn p.a.

Policy | Fiscal Cost | Average Electricity Bill Saving |

Remove remaining 25% of the RO costs from household bills | c. £780m p.a. | £27 p.a. |

Remove FIT costs from household bills | c. £730m p.a. | £26 p.a. |

Total Impact | c. £1.5bn p.a. | £53 p.a. |

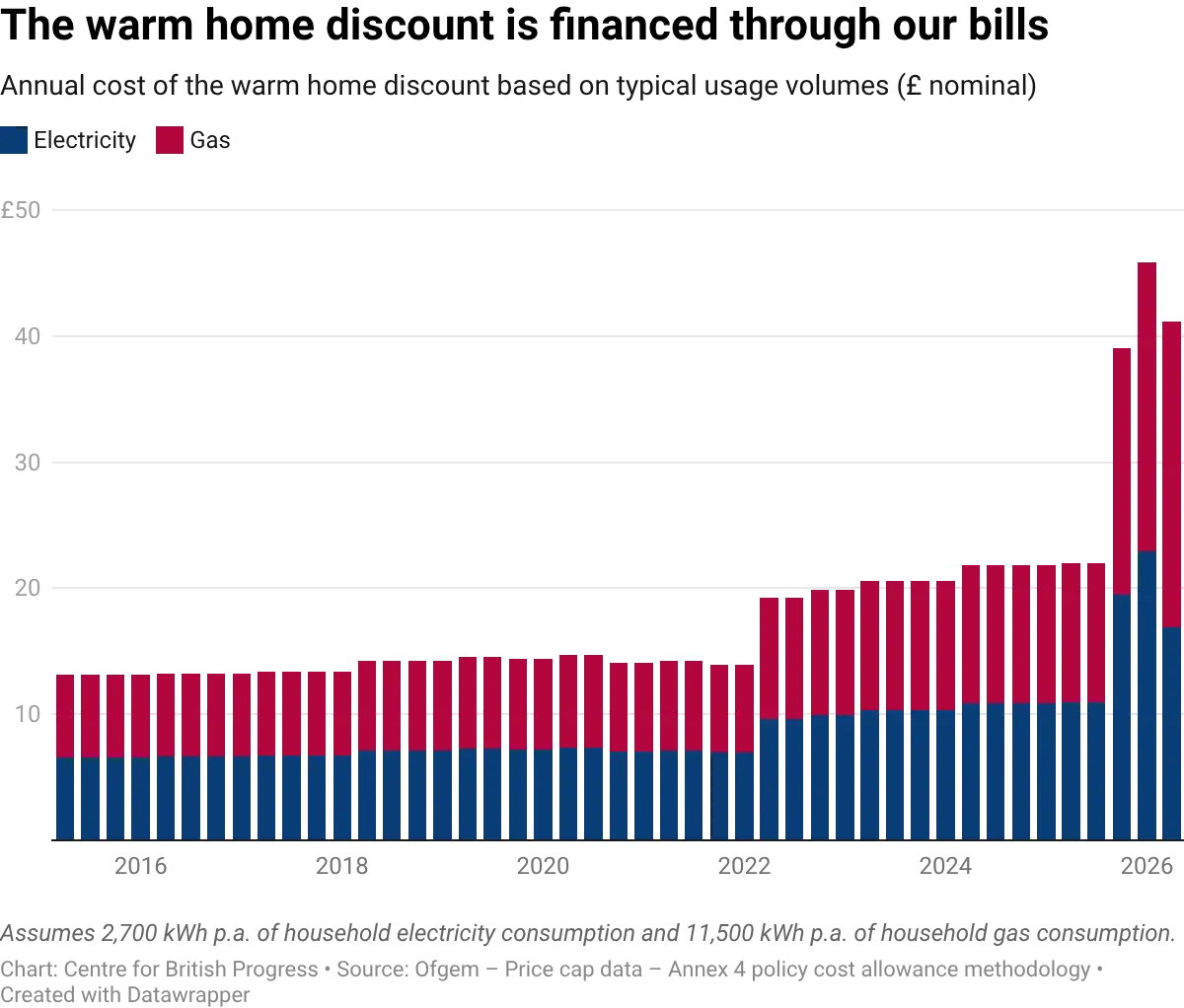

2. Move the electricity costs of the Warm Home Discount to general taxation

The Warm Home Discount helps tackle fuel poverty in Great Britain, by providing a £150 energy bill rebate to low-income and vulnerable households. The scheme is funded through a levy on all domestic gas and electricity customers, including those in receipt of the rebate.

In the year ending March 2013, around 1.65 million households received a £130 rebate. After two major expansions of the eligibility criteria in the last five years, the scheme is now estimated to provide around 5.9 million households with a £150 rebate.

The scheme is funded by applying a levy to every household's electricity and gas bills. Back in 2013, this might have added around £10 per household to an average dual fuel household’s bills. Now, however, Ofgem’s price cap data indicates that this costs a typical household over £40 p.a.

This £40 p.a. levy affects all households - reducing the net benefit for a typical rebate recipient from £150 to around £110.

Moving the entire cost to general taxation would incur a fiscal impact of around £1bn, but would reduce energy bills for all British households. If fiscal conditions don’t allow this much headroom, then just the electricity charge could be moved to general taxation, at a cost of c. £0.5bn p.a.

Moving the electricity component of the Warm Home Discount would reduce average household electricity costs by around £20 p.a. and would also improve the electricity to gas price ratio, further encouraging the electrification and decarbonisation of transport and heating.

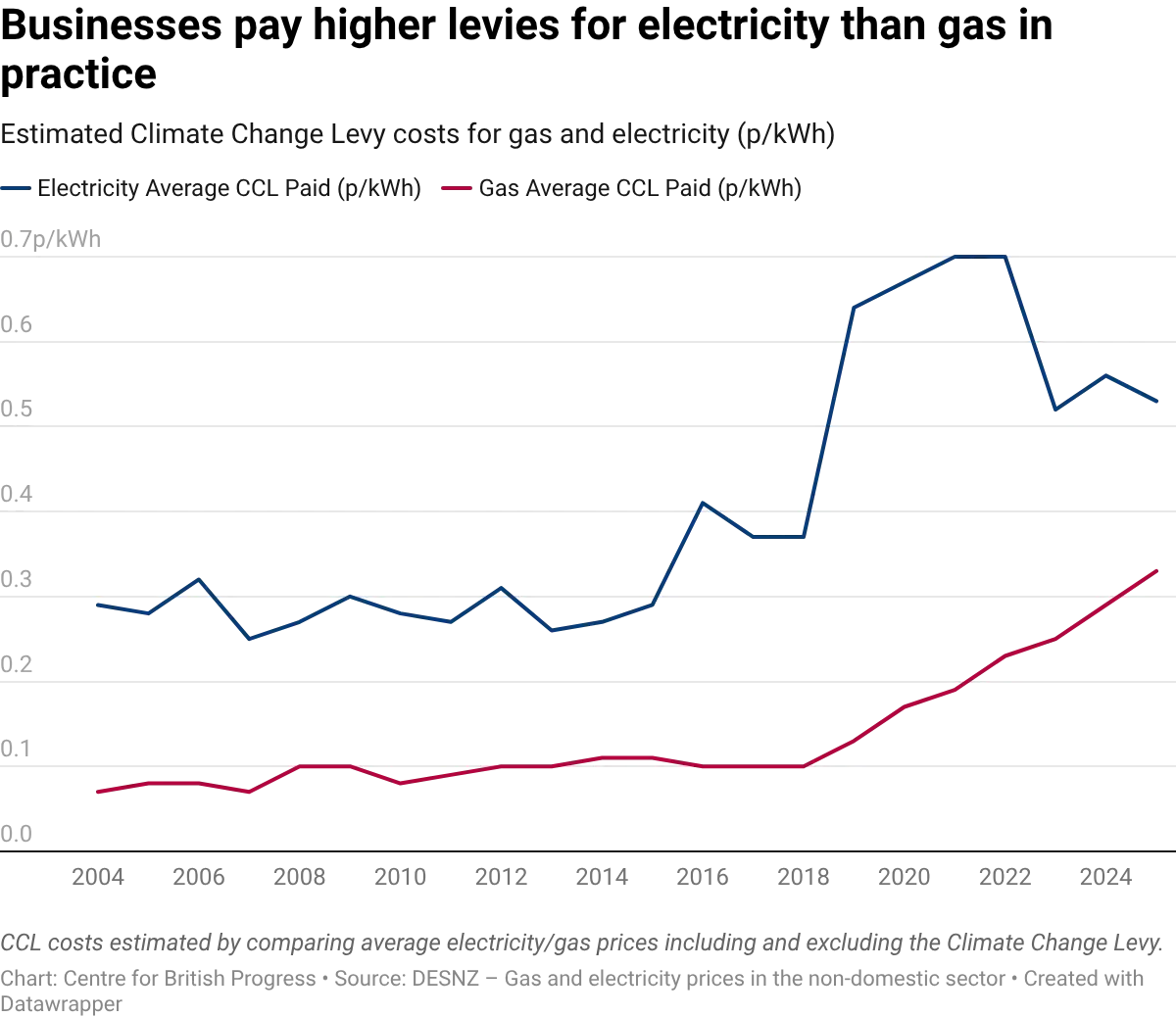

3. Zero rate electricity in the climate change levy

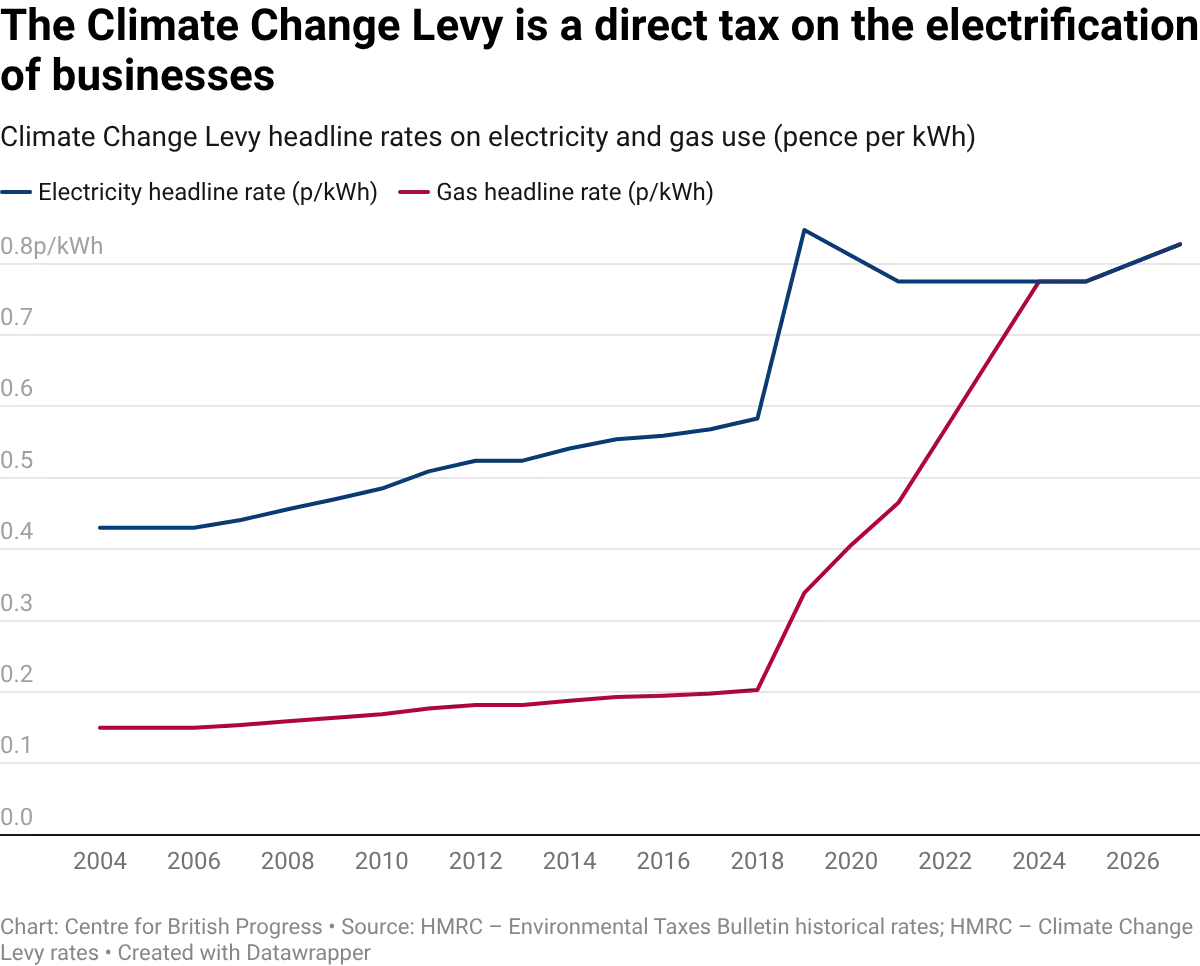

The Climate Change Levy is a charge on electricity, gas, liquid petroleum gas and solid fuels when supplied to businesses. When it first came into effect (April 2001), electricity was charged at nearly three times the rate of gas per kWh.

Rates have now been aligned for the two commodities, with both charged at c. 0.8p/kWh. This was a result of a commitment in the 2016 budget to equalise the main rates for electricity and gas by 2025 - and reduced a major electrification penalty.

The actual rate paid by a business will vary. Since 2005, various reduced rates have existed for sectors that have agreed targets with the government to reduce emissions.

This has descended into a complicated bureaucracy - holders of a “climate change agreement” can access discounts of up to 92% for electricity and 89% for gas. But it requires a sector association to manage the agreement between an industry and the Environment Agency.

According to the Reduced Rate Certificate database, there are 48 different sectors and over 8,000 individual facilities governed by these ingredients.

Taking into account all of these agreements, UK businesses paid around 0.53p per kWh in climate change levies. Removing this charge from electricity would have cut average business electricity costs by about 2.2% in 2025, and also reduce the bureaucratic drag associated with climate change agreements. For businesses without a climate change agreement, the cost saving would have been c. 3.2%.

We estimate the fiscal cost of removing electricity from the Climate Change Levy at c. £800m p.a.

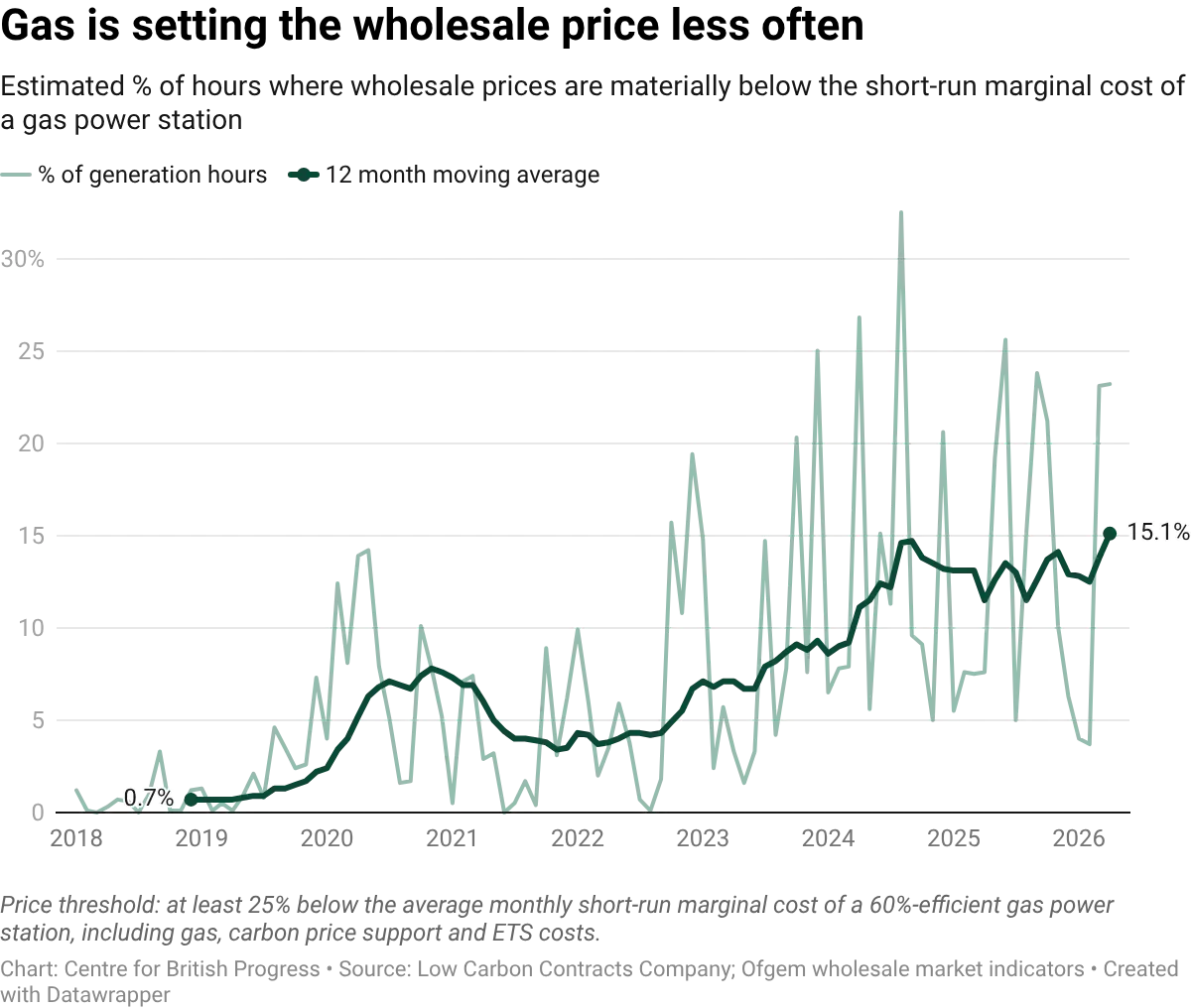

4. Remove electricity generators from the UK Emissions Trading Scheme for five years

The government has recently announced its intention to remove the Carbon Price Support from April 2028, an £18/tonne carbon tax paid by gas power stations. Removing this levy is a positive step for electrification, as it reduces the wholesale price of electricity whenever gas is setting the marginal price.

The UK Emissions Trading Scheme is a cap and trade system that prices carbon - current at around £52/tonne. It covers heavy industry, power generation, fuel supply and a proportion of aviation, encompassing around 25% of UK territorial emissions.

Removing £52/tonne of carbon costs from electricity generators would cut the marginal cost of generation from a combined cycle gas plant by c. £19/MWh.

Assuming gas sets the marginal price of electricity 80% of the time, and that CfDs cover 20% of generation next year, we estimate that this will cut retail prices by just over £12/MWh, or 4% in 2027. We estimate this would cut average household electricity costs by around £41 p.a.

Over time, gas and carbon costs will have a reduced role in price formation. More periods of low marginal cost generation will reduce the impact of gas in the wholesale market, and more generation linked to Contracts for Difference and Regulated Asset Base models will weaken the link between wholesale and retail prices. This is why we suggest a 5 year suspension only - giving bill relief to consumers whilst more generation capacity is built and expensive legacy contracts start to expire.

We estimate that this 4% bill reduction for households and businesses would come at a fiscal cost of c. £1.2bn p.a.

Although costly, this is the most fiscally efficient way of reducing electricity prices - as it reduces the inframarginal rent enjoyed by renewables and nuclear power stations that derive their revenues in part from the wholesale market.

Critics will argue that this will lead to a major rebound in using gas for electricity generation. We think this argument is dramatically overstated. Firstly, the fuel cost of gas will remain - solar, wind and nuclear all have much lower marginal costs and will dispatch first. Secondly, the risk of the UK gas plants running at higher utilisation in order to export to the EU should be reduced by the EU’s own Carbon Border Adjustment Mechanism, with the carbon price differential priced.

The desire to align with the EU ETS is understandable, but reducing carbon costs is one of the few fiscally efficient levers to reduce electricity prices in Great Britain. There are two reasons why we suggest a 5 year exemption for electricity generators:

- Although we are building renewables at a rapid pace, 80% of our existing nuclear capacity is currently scheduled to close by March 2030, with Hinkley C’s first unit now scheduled to be operational in 2030 at the earliest. Lower levels of clean baseload power could give gas a greater role on wholesale price formation in the short term.

- British electricity consumers are suffering from expensive electricity prices, in good part due to onerous contracts signed under the FiT, RO and early CfD schemes. In five years time, the costs of these legacy contracts will have eroded, and carbon pricing in the electricity sector can be reintroduced.

Removing electricity generators from the UK ETS for five years is a pragmatic step to cover these gaps. Aligning with the EU ETS immediately represents a major loss of optionality in electricity bill reduction.

Package 2 - More reform in future

It is fiscally painful to take further action on electricity costs, correcting for multiple schemes that continue to pay generators in excess of £200/MWh. It is vital that the UK government, both now and in the future, becomes much more serious in future negotiations, so that we don’t create a new generation of heinously expensive contracts that require taxpayer bailout further down the line.

The Department for Energy Security and Net Zero has effectively been given the power to procure electricity and hydrogen on behalf of the public, who bear the cost, either through bills or through taxation. It should exercise that power with much greater responsibility, and with greater oversight from the Treasury.

The November 2025 Budget proposed subjecting additional energy costs and levies “to enhanced scrutiny under a new framework”, ensuring that they represent value for money for households and businesses. The Treasury should lead this work, consulting energy consumers rather than generators, when designing the framework.

We share six proposals below to reduce costs in the electricity system.

Proposal 1: Set future administrative strike prices at a level consistent with lower bills

Administrative strike prices act as price limits at the start of a CfD allocation round. Historically they have been set by modelling a given proportion of the supply curve for each technology. In other words, households have been forced to subsidise the development of new technologies, playing the role of investor, but with no equity stake.

Instead, strike price limits should be set at a level that is consistent with lower bills. If no capacity is procured, then the generation industry should sharpen their pencils and try again next year. The aim is not to maximise procurement or subsidise some technologies over others, but to get cheaper electricity for consumers. Ultimately, that is a better deal for households, and also better for climate change, as the biggest barrier to electrification is the cost of electricity, not the amount of renewable generation capacity.

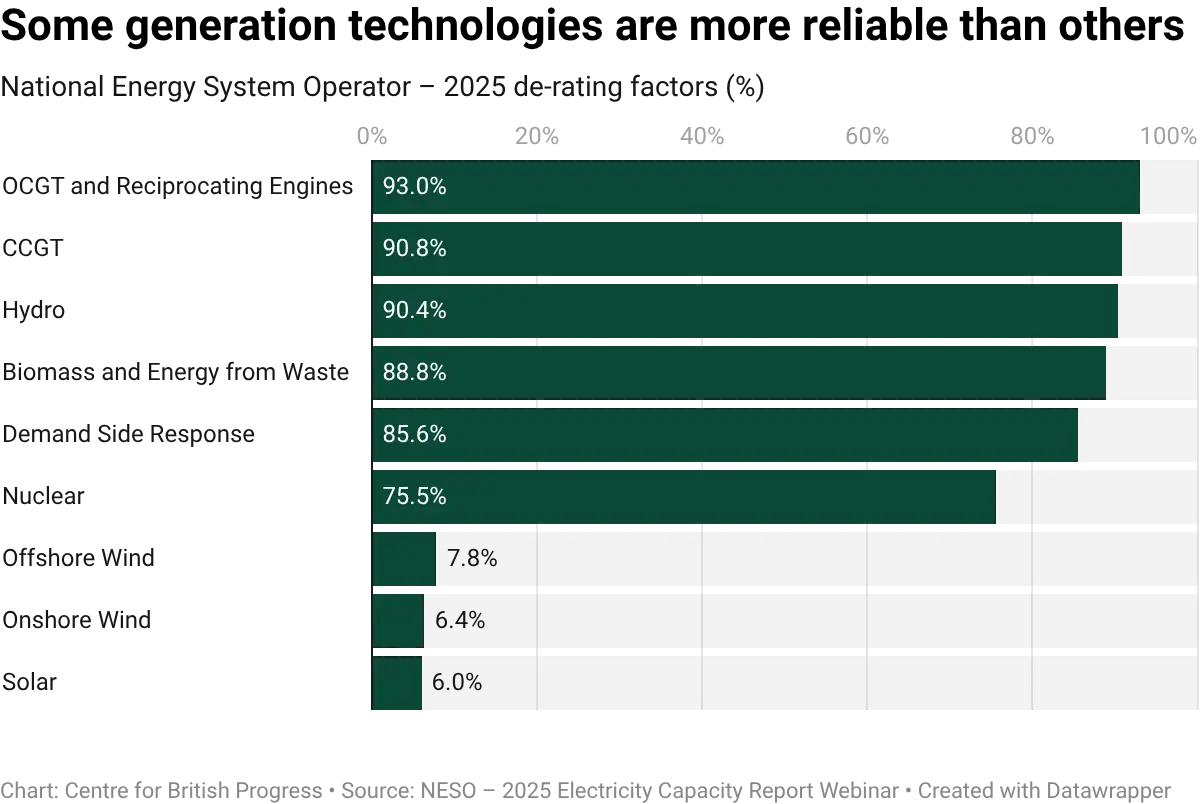

Solar and wind make minimal contributions to firm capacity on the electricity system - as they cannot reliably deliver power on the coldest and darkest days of the year. They are valuable to the extent that they save fuel costs and carbon emissions. Other CfD eligible technologies such as hydro, energy from waste and geothermal have greater ability to provide firm power in addition to saving fuel and carbon.

Each technology should have a strike price limit based on its ability to save fuel, reduce emissions and provide firm capacity. The following inputs can be used as a counterfactual:

- Gas costs - based on a 50/50 weighting of the trailing 10 year real gas price and the 5 year forward curve - using a 49% efficient CCGT

- Carbon costs - based on an agreed carbon price and a 49% efficient CCGT

- Firm capacity value - based on NESO de-rating factors and the most recent T-4 capacity market value (Currently £27.10/kw/year)

In the case of offshore wind, this would equate to a price limit of around £85/MWh at current prices - approximately £59/MWh for the gas, £26/MWh for the carbon (At £70/tonne CO2e) and £0.50/MWh for the firm value of offshore wind.

This mechanism would prevent us from wasting millions on supporting particular technologies beyond their productive use to energy security and cost. Since CfD allocation round 4 (2022), Great Britain has procured nearly 600 MW of floating offshore wind at a weighted average strike price of £210/MWh and 143 MW of tidal stream at average strike prices of £275/MWh.

If all of this capacity is built, these contracts will add c. £370m p.a. (or c. 0.5% to British electricity costs) versus a counterfactual generator at £90/MWh. If DESNZ wants to make venture capital style bets, it should use its own departmental budget, not consumer bills.

Proposal 2: Make future CfD rounds technology neutral - and adjust for firm capacity value

CfD Allocation Round 7 (2025) used four different technology pots that allow different groups of technologies to clear at different prices. We are now decades into renewable development and shouldn't be afraid to prioritise the most cost effective technologies.

This year’s auction, Allocation Round 8 (AR8), should put all technologies (including smaller nuclear projects) into a single pot to increase competition and reduce strike prices. We suggest an adjustment to the allocation round process, so that a technology-neutral allocation round will deliver better value for consumers.

Generators built under a CfD that provide dispatchable or firm power deliver a system benefit for which they go unrewarded. This is because generators in receipt of CfD support are not eligible to participate in the Capacity Market - a market that ensures that Britain has enough available electricity to cope with system stress events.

The largest part of the capacity market clears 4 years in advance (T-4) of its delivery year. Successful participants receive a payment in exchange for making their power available during system stress events - periods of high electricity demand relative to supply.

When determining the clearing price in a technology neutral CfD round, capacity value should be taken into account. We propose incorporating this information via a technology specific capacity adjustment to each technology.

We show a stylised example of our capacity credit calculation that covers solar, offshore wind, hydro and nuclear. We use the most recent T-4 Capacity Market clearing price (£27.10 per kw/year) for delivery year 2029/30 and NESO’s most recent de-rating factors for each technology.

Technology | Onshore Wind | Offshore Wind | Solar PV | Nuclear | Hydro |

De-rating Factor | 6.35% | 7.81% | 5.96% | 75.54% | 90.40% |

Capacity Market value / MW | £1,721 | £2,117 | £1,615 | £20,471 | £24,498 |

Capacity Factor | 37.0% | 49.0% | 12.0% | 80.0% | 35.0% |

1MW produces (MWh) | 3,241 | 4,292 | 1,051 | 7,008 | 3,066 |

Capacity Credit: £/MWh | £0.53 | £0.49 | £1.54 | £2.92 | £7.99 |

The ‘free’ capacity value associated with 1MW of hydro is worth around £8 per MWh per year, versus around 50 pence for offshore wind. This capacity credit should be used to determine which technology clears first - for example if an offshore wind bids at £80/MWh and a hydro project at £85/MWh, it makes sense from a societal perspective to secure the hydro project first.

This should create a much more adaptive framework going forwards - if the clearing price in the T-4 capacity market increases, then CfD rounds will bias towards procuring firmer power sources. If capacity market prices fall, then CfD rounds will tend towards the lowest cost technologies per MWh, regardless of firm value.

Generators should also be exposed to the grid upgrade and balancing costs that they create. The Reformed National Pricing (RNP) programme should ensure that generators fully internalise these costs. Given RNP is unlikely to be finalised imminently, adjustments for grid and balancing costs should also be incorporated into the clearing price for the forthcoming Allocation Round 8.

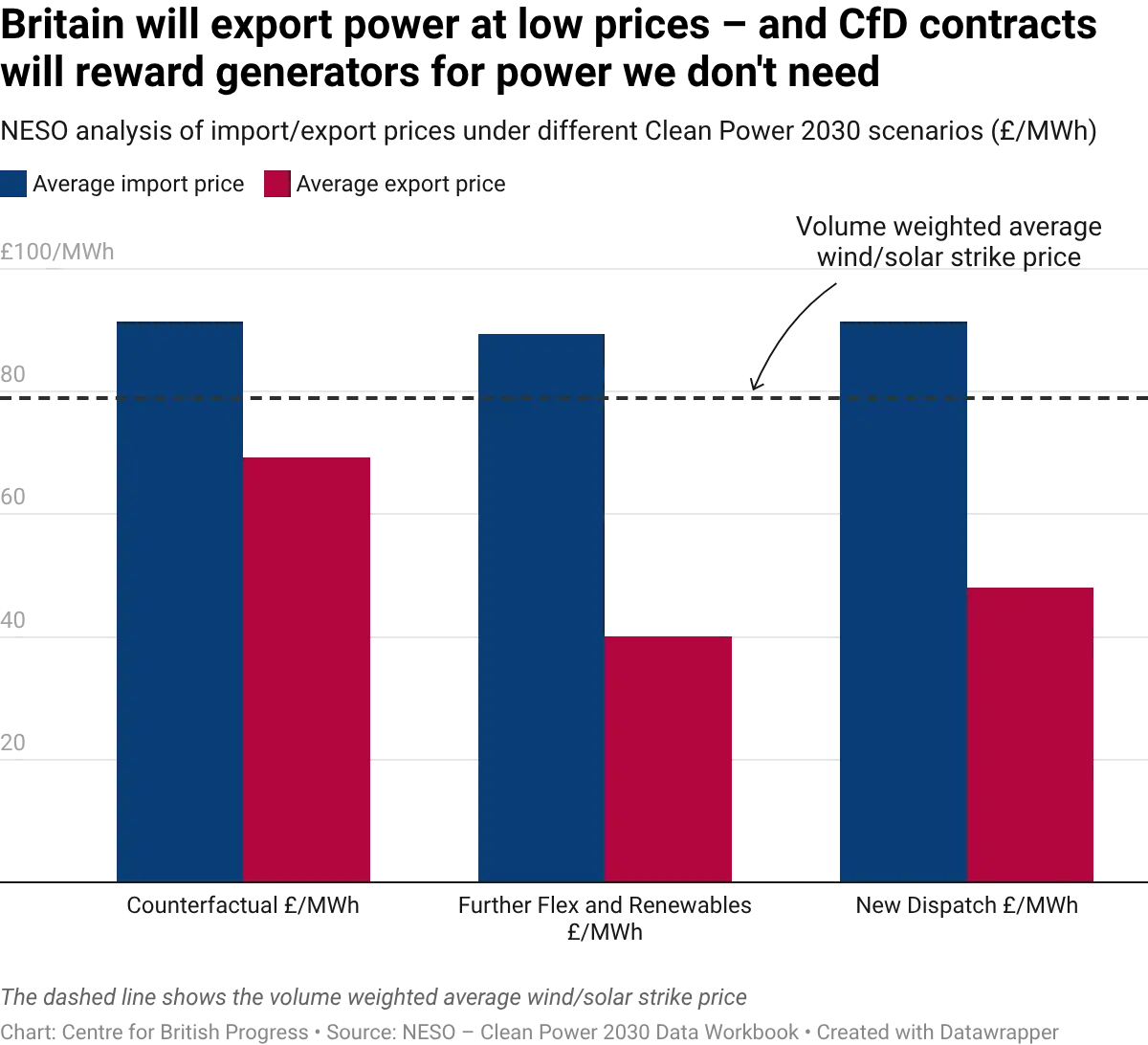

Proposal 3: Address the export problem in CfD contracts

A major flaw in CfDs is that they largely treat each MWh of generation as equally valuable - with little reference to the timing or locational value of that electricity.

Over time, contracts have been tightened up. For instance, generators no longer receive a top-up payment for an individual generation hour if the wholesale reference price is negative.

A further improvement could be made, to counter a problem created by exported electricity. As Great Britain builds out solar and wind generation, we can expect more periods when the country is net exporting power to Europe via interconnectors. This isn’t a problem in an unsubsidised market - as it represents incremental revenue for low marginal cost technologies. But it is a problem if generators are receiving a CfD top-up payment.

Consider a scenario on a windy day, when Britain is net exporting electricity. If the wholesale price of electricity is £10 per MWh and generators are on a £90/MWh CfD, they will receive an £80/MWh top up, paid for British consumers, to export power the country does not need. In short, we are subsidising French, Dutch, Belgian, Norwegian and Danish consumers thanks to poor contract design.

NESO has highlighted this risk - their costs and benefit analysis of Clean Power 2030 states that:

“One factor contributing to higher system costs in our pathways is the increased available energy within the system, not all of which is utilised by local consumers”

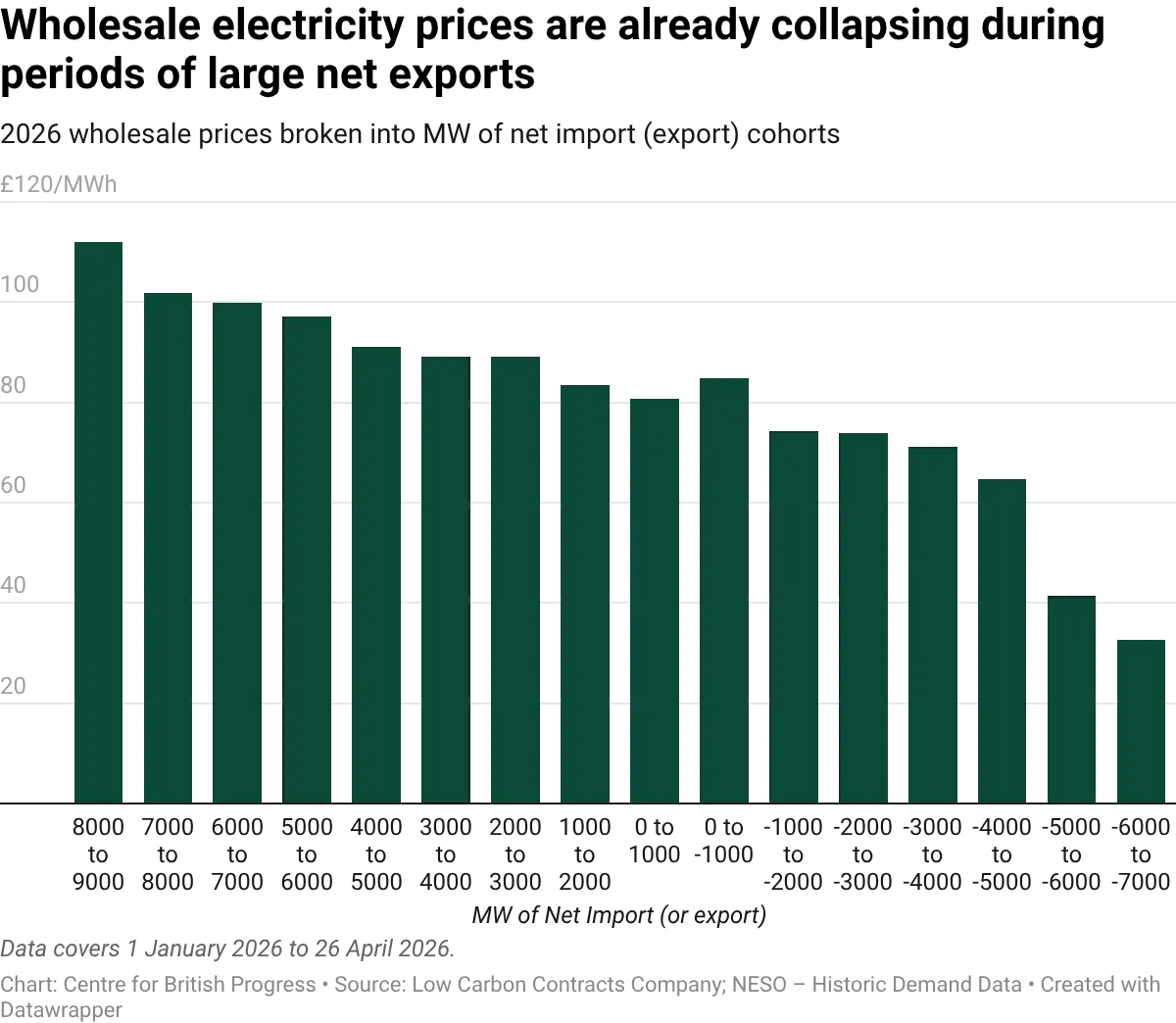

“As Great Britain transitions to a clean power system, it is anticipated to become a net exporter of electricity. However, exports will be highest during periods of high renewable energy output, which typically coincide with relatively lower prices under current arrangements. While exporting can help recover some costs compared to curtailing excess generation, significant net exports at low prices still incur some overall costs to the British system.”

We examined 2026 wholesale prices according to how much electricity is imported or exported. There is a near-monotonic relationship between the two variables - Britain imports at high prices, and exports at low prices, typically driven by high wind output. At this stage the problem is relatively modest - as Britain was net-exporting over 3GW for about 4% of operating hours in 2026, typically during windy, overnight and early morning hours. But this issue will grow in scale, as more wind projects procured under previous CfD rounds are completed and start generating in a correlated fashion.

A solution to this problem is to introduce a new variable to future CfD contracts - the net export clawback. The idea would be to scale back the CfD top up according to how much Great Britain is net exporting power.

CfD top up scaling factor = (GB electricity generation - GB electricity net exports) / GB electricity generation

For instance, if Great Britain was generating 40GW and net exporting 5GW, the CfD top-up would be scaled back to 87.5% of its previous value in those generating hours.

Whilst this clawback would marginally increase the headline clearing prices of CfD auctions, it wouldn’t increase system costs - the costs of this export driven effect are already being socialised across consumer bills.

The advantage of exposing generators to their own net export profile in the context of a technology-neutral CfD round is that you reveal information. Generation technologies that are correlated with the existing generation base and create export heavy power gluts will have to bid higher, giving relative advantage to less correlated generators in the CfD auction.

Over time, this will encourage wind projects in parts of the country with less correlated wind profiles, and improve the economics for firm or despatchable generators - such as hydro, nuclear and geothermal.

The Government should be sceptical of industry lobbyists that call for maximising interconnector capacity and removal of all export frictions. Exporting power at low wholesale prices and topping up CfD generators for power the country doesn't need is a rising burden on British billpayers.

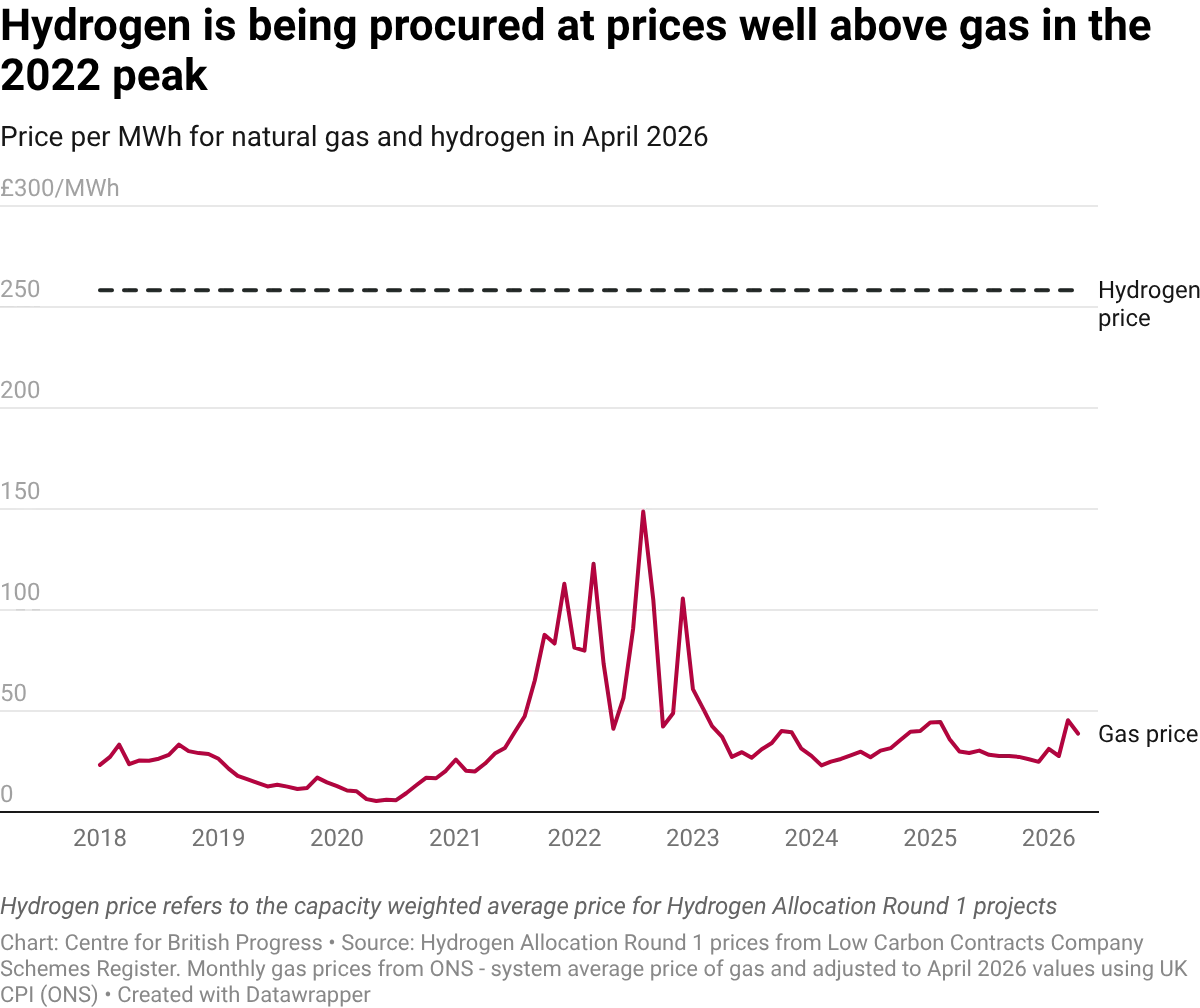

Proposal 4: Dramatically scale back hydrogen funding

The first hydrogen allocation round was monstrously expensive. 143 MW of hydrogen output capacity was procured at a current weighted average strike price of £258/MWh for thermal energy. We have plotted the procured hydrogen price next to monthly day ahead gas prices since 2018.

The UK offered 15 year inflation linked prices at prices above the highest month of gas prices during the Russian invasion of Ukraine. We estimate this equates to paying a carbon abatement cost of well over £1000 per tonne at current prices and the total subsidy is estimated to total over £2bn. This largesse will be recovered through consumer bills from 2027, via the Gas Shipper Obligation. This is expected to add around £3-£7 p.a. to household gas bills, depending on the method of cost recovery.

The current scheme is thankfully fairly small, but needs nipping in the bud. All future hydrogen funding should be subject to a strict carbon abatement cost threshold. As an absolute maximum, the £235/tonne value for 2050 from DESNZ’s net zero aligned carbon price model could be used as a threshold. If the industry cannot meet this threshold, then it should be ignored.

The same logic should be applied to all carbon capture and storage projects that are seeking subsidy support. The UK can deploy the same funding in electrification projects to decarbonise at much lower abatement costs.

Proposal 5: allow a broader range of decarbonisation options for domestic heating

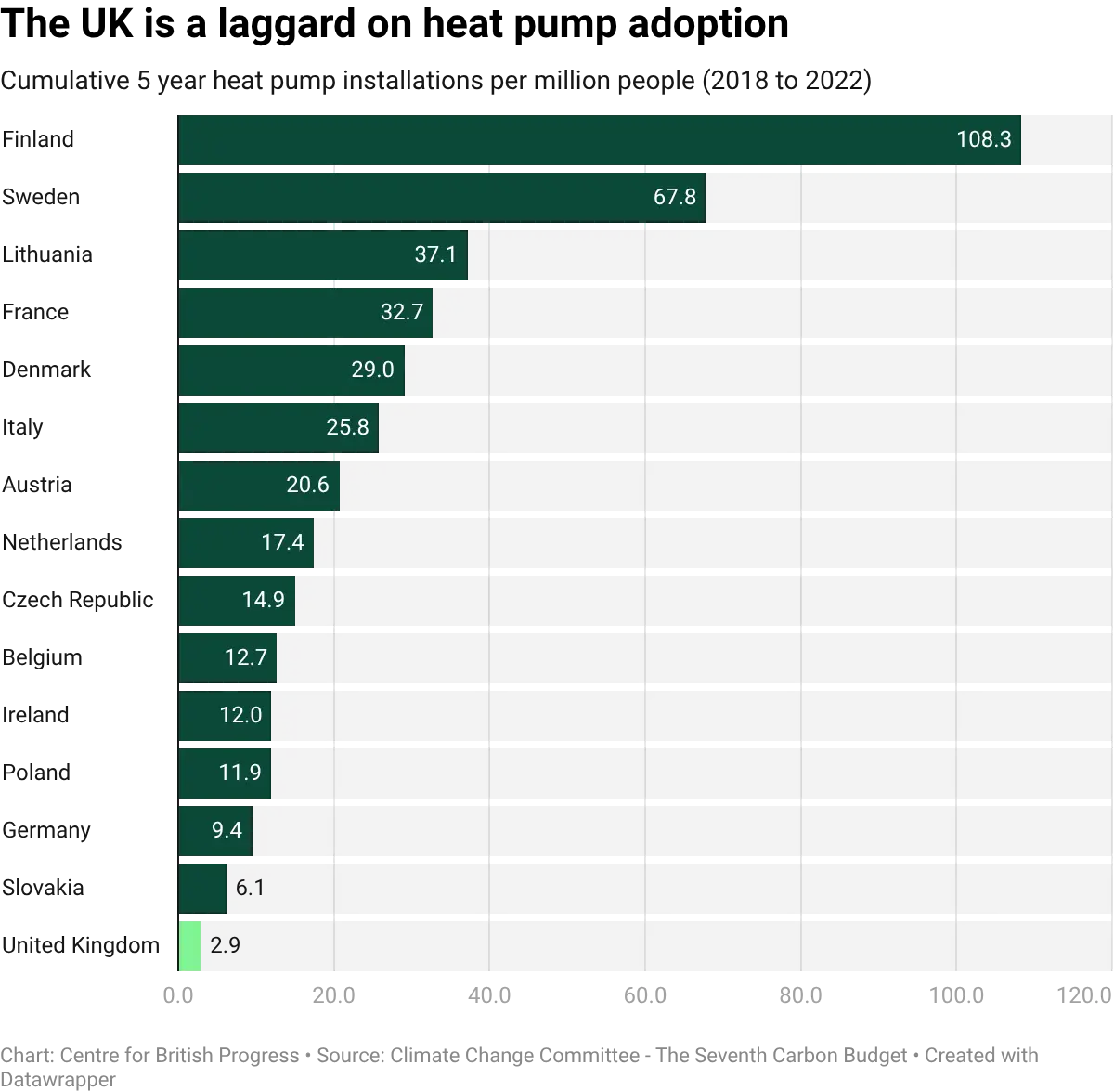

Heat pumps are an amazing technology, converting clean electricity into warmth for households. They are much more efficient than gas boilers, with real world studies suggesting they are around three or even four times as efficient.

However, uptake in the UK has been slow, with around 60,000 retrofit installations in the UK in 2025. This compares to a total domestic gas boiler market of around 1.5 million units p.a.

Much of this limited heat pump uptake can be attributed to a high electricity to gas price ratio, which this paper seeks to correct. But high capital costs are also part of the problem, with average air-source heat pump installation costs of c. £13,300 in 2025.

A further barrier to widespread heat pump adoption is correlated electricity demand on the coldest days of the year. This creates a major demand spike on very cold days, requiring substantial investment in firm generation and grid reinforcement. There are three major drivers behind this:

- Demand for heating is highest on the coldest days of the year

- Heat pumps lose efficiency when the temperature differential between the outside and indoors increases

- Diversity of demand between households drops - as heat pumps run at much higher utilisation - 20 or more hours per day on the coldest days

Gas distribution networks are stress tested at a 1 in 20 year winter, which isn’t currently applied to electricity distribution network planning.

On the 20th of November 2025, my (London based) flat used about 154 kwh of gas, or around 139 kWh of heat consumption assuming 90% boiler efficiency. Assuming a heat pump co-efficient of performance of 2.44, in line with the cold snap performance data from the Electrification of Heat Demonstration Project, that equates to 57 kWh of incremental electricity demand if I had a heat pump.

Even if that demand was evenly spread over 20 hours of stable use, 2.85kw of demand multiplied by 28 million households is nearly 80 GW of incremental electricity demand that must be met by distribution networks - which currently experience peak loads of around 50 GW.

Hybrid heat pump systems combine technology from gas boilers and electric heat pumps - allowing the heat pump to do the largest share of the space heating, with the gas boiler kicking in for very cold temperatures or for hot water. The system level advantage is that hybrid systems could switch to gas use on the coldest days of the year, reducing the requirement to build out electricity distribution networks and generation capacity to handle the coldest days of the year.

Consumers could also benefit from automatic switching based on electricity prices, helping UK electricity consumption respond during windy periods.

The Department for Energy Security and Net Zero (DESNZ) recently expanded the boiler upgrade scheme to include a £2,500 grant for air-to-air heat pumps that can also provide cooling in UK homes. A literature review on air-to-air heat pumps was undertaken in January 2025, with the new legislation taking effect from the 28th of April 2026.

As a first step, DESNZ and the Energy Systems Catapult should undertake a literature review of hybrid heat pump systems as a solution to help decarbonise heating systems in our existing housing stock.

The review should balance the system cost benefits of hybrid heat pumps with the risks of locking in a more carbon intensive solution - and examine the case for inclusion in the Boiler Upgrade Scheme at a much lower level of policy support.

Proposal 6 - Address grid costs

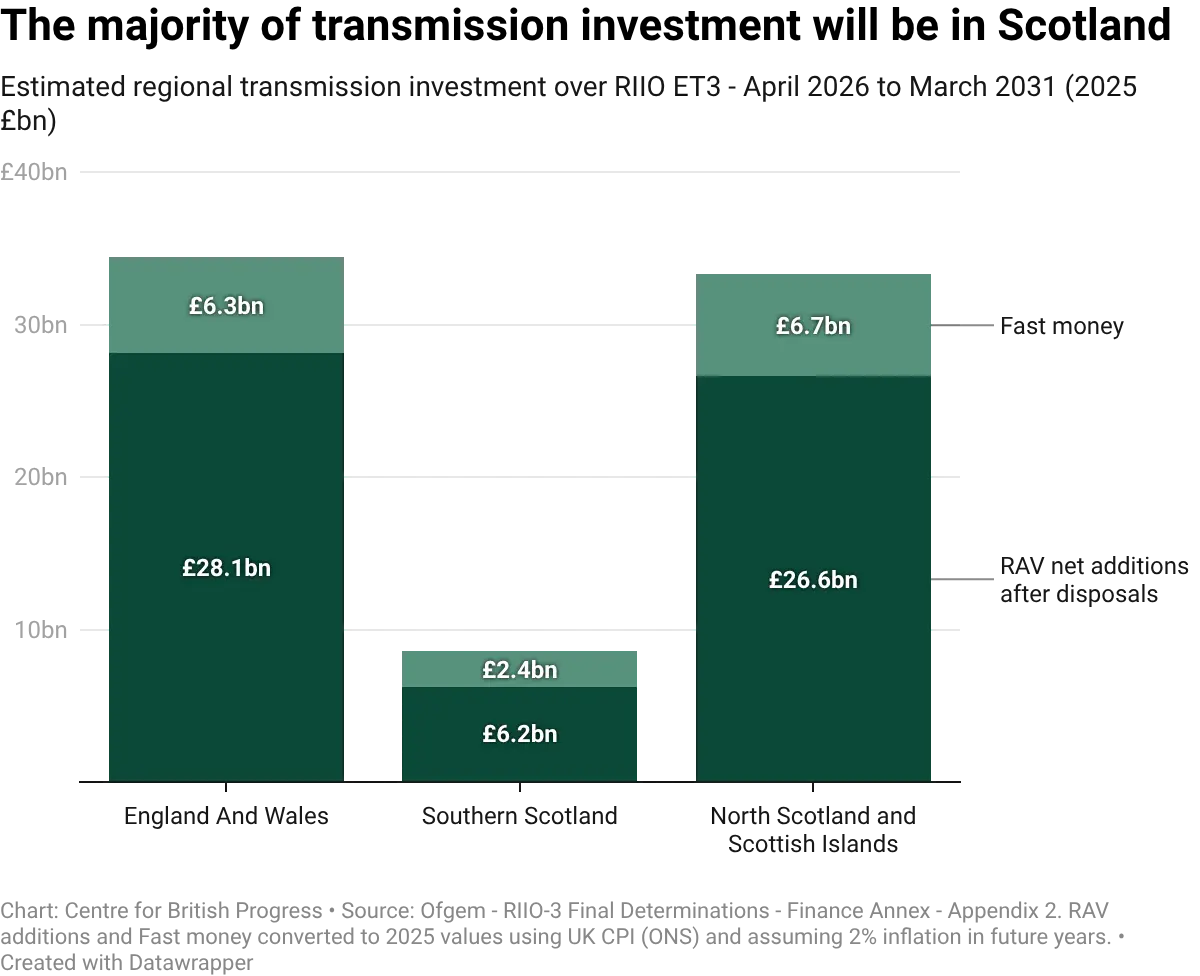

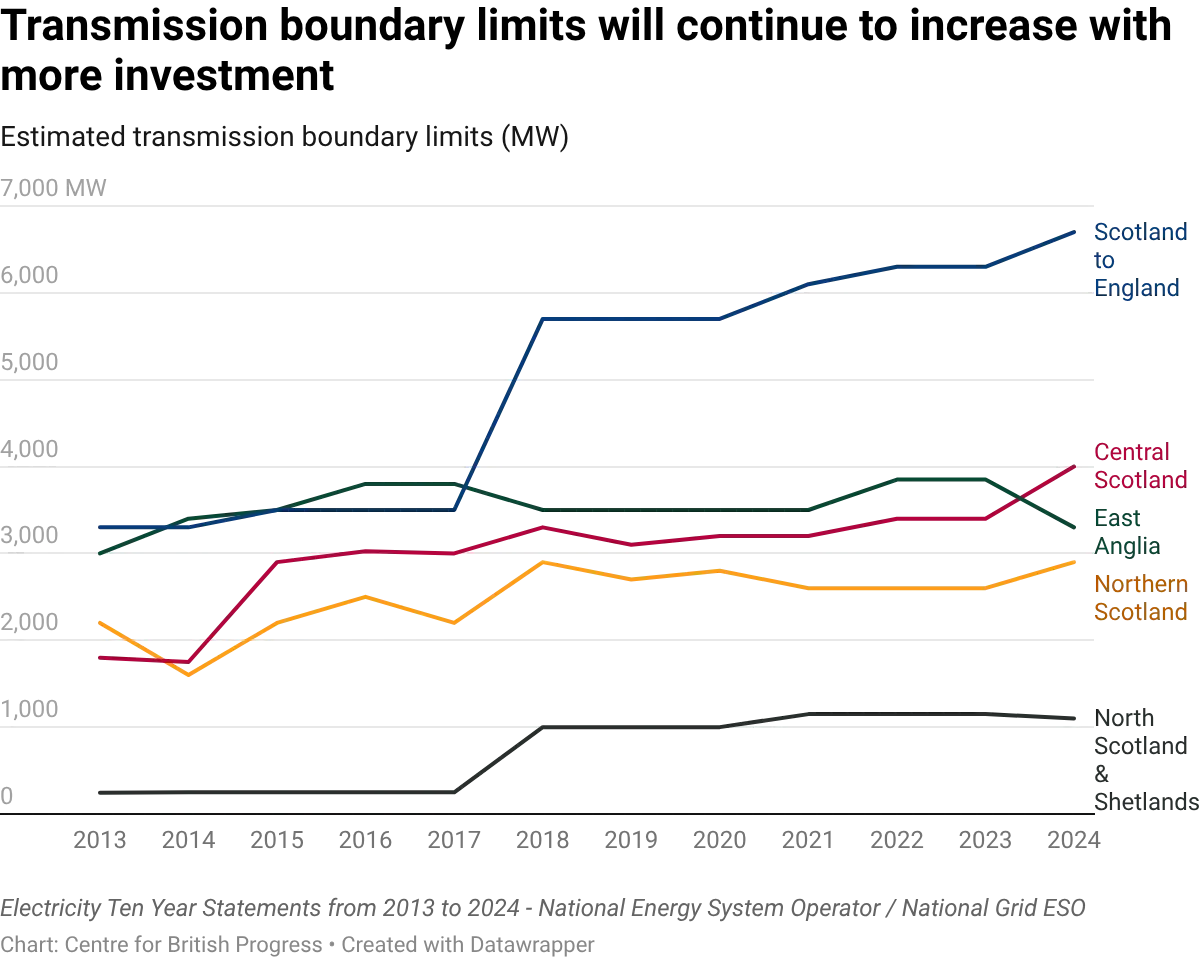

Great Britain is currently embarking on a massive expansion of its transmission network. The new control period runs from April 2026 to March 2031 - investment over the control period could exceed £70bn, almost four times the level of the previous five years. Much of this investment will be directed towards Northern Scotland, so that distant wind farms can deliver their power further South.

Most of this investment will be added to the regulated asset base of the networks, and will be charged through consumer bills over a 45 year depreciation period. Independent forecasts estimate that transmission charges will double between 2025 and 2030, adding around £50 to household bills.

Some grid spending undoubtedly needs to happen - we have already built a lot of wind capacity in Scotland, and it makes sense to continue alleviating boundary constraints to make better use of this clean electricity, and reduce the balancing costs that households have to pay.

But we should also subject spending to a greater degree of scrutiny. Britain is pursuing a version of grid decarbonisation that is particularly wind-heavy - forecast to generate around 60% of our power by 2035 according to the NESO’s 2025 Future Energy Scenarios.

Building new generation capacity in the furthest parts of Scotland risks creating the need for multiple transmission upgrades, as the power needs to work its way through multiple bottlenecks to get to demand centres further South. Our transmission spend should be dedicated to alleviating our current transmission constraints - not enabling a new set of constraint payments in future.

Ultimately, the cost of constraint needs to be put back on the generators that cause them, not onto the bill paying public. Locational pricing would have been a positive step in exposing generators to some of the system costs that they create, and is a missed opportunity for the time being.

But there are further cost-efficient ways to get the most out of our transmission capacity, which could work alongside new transmission construction.

Transmission lines and substation equipment have limits in terms of how much power they can handle. If too much power flows, equipment can overheat and reach its thermal limit. However, on colder and windier days, more power can be transmitted before thermal limits are reached. Dynamic Line Rating (DLR) technology allows the grid operator to monitor the temperature of the network in real-time - meaning more power can be allowed to flow when it is windiest and coldest, reducing constraint costs.

National Grid have recently announced that they are applying DLR to an additional 585km of their network, increasing the power carrying capacity of those circuits by an average of 8%. In 2025, SSE had over 300km of DLR coverage and the new transmission control period offers transmission owners the opportunity to own 10% of the avoided constraint costs.

One of the challenges of seeing the full benefits from DLR is Britain’s three different regional transmission owners. Power flows from north to south will be limited by a particular bottleneck on the network, so DLR needs to be added widely across the system to achieve its full benefit. The control room for the National Energy System Operator also needs a consistent and reliable set of data if they are able to run the transmission system closer to its limits.

NESO should set out the standardised data format and redundancy level they require for DLR to be used to its maximum effect. Ofgem should then instruct the three transmission network owners to use that data format, and coordinate their DLR deployment onto the most cost effective power flow corridors to reduce constraint costs. In turn, NESO should disclose their use of DLR (and estimated savings) in their annual balancing costs report.

Conclusion

Cutting the cost of electricity is a rare unifying force in British politics - appealing to those concerned about economic growth, energy security and decarbonisation.

Moving historic levies into general taxation can give a much needed kick-start to British electricity consumption. But we must learn the lessons of the past - and stop creating contractual horror shows for future generations to deal with. That’s why fundamental reforms to our electricity market must come alongside near term bill relief.

For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]For more information about our initiative, partnerships, or support, get in touch with us at:

[email protected]